Breakfast Bites: Escalation on All Fronts

Iran attacks US military facilities in Kuwait and Bahrain, a new tariff front opens, and AVGO reports tonight.

Rise and shine everyone.

Markets ended yesterday near all-time highs, fading Iran and riding a historic momentum reversal. I’m not sure that holds today.

Overnight, Iran struck US and Kuwaiti military facilities with missiles and drones. The IRGC claimed an attack on the US Fifth Fleet headquarters in Bahrain. Kuwait’s airport took damage and casualties. The US hit back at Qeshm Island. This is not a ceasefire.

The USTR also proposed 10-12.5% tariffs on 60 economies over forced labor concerns, with China, the UK, Australia, and Switzerland among those named. It landed quietly. It shouldn’t have.

The market cannot fade Iran escalation and a new tariff front at the same time. At some point, one of them sticks. AVGO tonight will tell us whether the AI capex story is still the ballast.

Three things driving the tape today:

Iran attacked US military facilities in Kuwait and Bahrain overnight, pushing oil 2.5% higher. Watch how equities open.

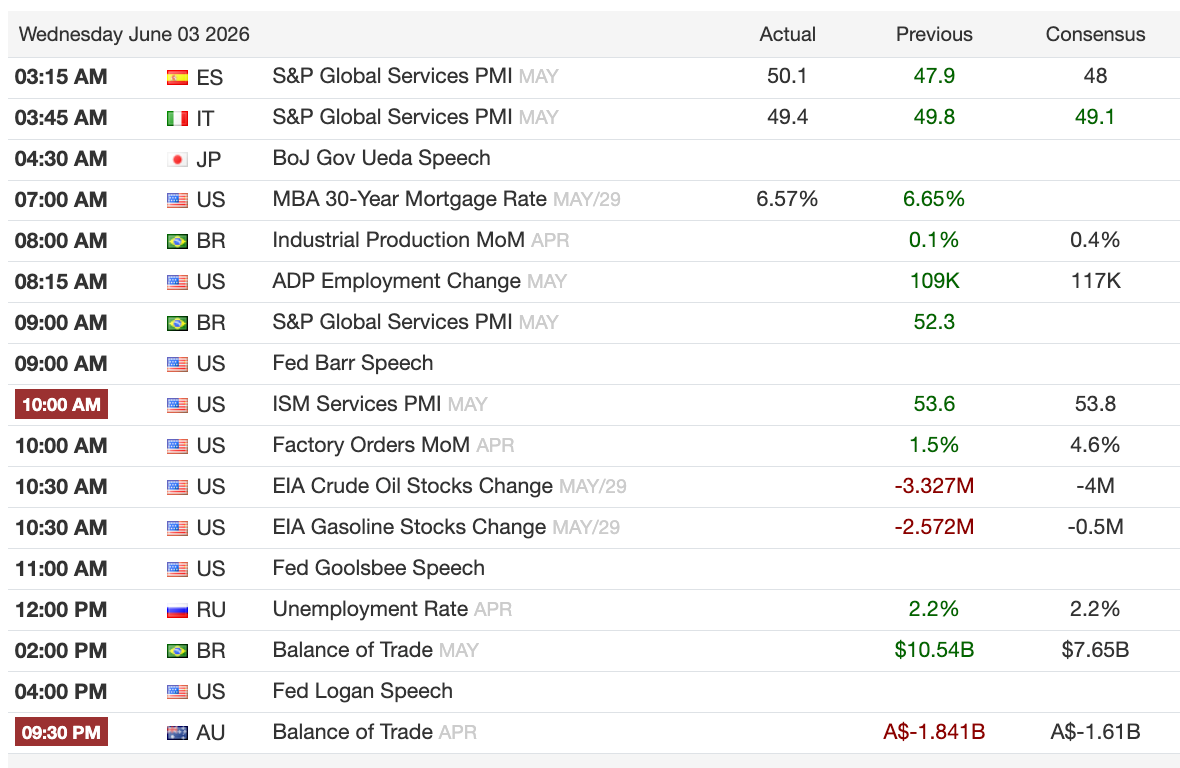

ADP at 8:15am and ISM Services at 10am are the data anchors ahead of Friday’s NFP.

AVGO reports after the close. The whole AI trade gets a verdict tonight.

Morning Macro Briefing

Iran struck US and Kuwaiti military facilities overnight with missiles and drones. US and coalition defenses intercepted most of them. Kuwait’s airport still took damage and casualties were reported. The US struck back at Qeshm Island and disabled a non-compliant tanker in the Gulf.

Trump says talks with Iran are ongoing. Iranian media says no talks have taken place. The fighting is real either way.

Brent +2.5%, WTI +2.6% overnight. Maersk says Hormuz rerouting is now costing above $500M a month in extra expenses and rising. Oil hasn’t fully priced this.

The USTR proposed new tariffs of 10-12.5% on 60 economies over forced labor imports. China rejected them outright. Australia said the tariffs violate its free trade agreement with the US. Taiwan expects favoured status. Canada flagged a constructive meeting with USTR Greer. A US court separately ordered broad IEEPA tariff refunds in the same 24-hour window. It’s noisy, but the tariff baseline is still moving higher. USMCA mandatory review is July 1.

BOJ Governor Ueda was hawkish overnight. He said the BOJ will keep raising rates, and flagged that oil-driven inflation is spreading faster and wider than in prior cycles. The yen hit 160/USD, the level that triggered Japanese intervention in late April. Japan’s Economy Minister Takaichi flagged close FX coordination with the US. Watch that level.

EU Services PMIs beat expectations in May across the board. Most remain below 50, but the beats were broad. Eurozone services composite at 47.7 vs 46.4 expected. Italy and Spain held in expansion. Germany and France below 50 but better than feared. The ECB is hiking 25bps on June 10, now priced at 97% probability.

In Asia, the Nikkei surged 3% to fresh records above 68,000. Hang Seng gave back most of yesterday’s gains. China’s services PMI rose to 54, expanding for the 39th consecutive month. Australia’s Q1 GDP came in at just 0.3%, per capita -0.1%. Not great.

Chart of the Day

Software ran 15% in three days last week. IGV took in over $400M in a single session, the sixth consecutive day of net inflows. Call options on the ETF hit an all-time volume record on Friday.

The chart shows shares outstanding still climbing even as price has reversed. This is a flow trade, not a fundamental one. AVGO tonight will tell us whether the underlying AI capex thesis holds, or whether this entire software move was a crowded momentum mistake waiting to unwind.

Calendars

Market Prep

Yesterday: SPX +0.1%, NDX +0.5%, RTY +0.9%. Momentum was the real story. AI names, semis, and data centers ran hard. Software reversed sharply. It was one of the biggest single-day momentum moves in several years.

[CHART: Momentum factor, year-to-date]

This morning futures are flat to -0.3%. European markets opened lower on the tariff news.

The general trend is still bullish. Markets are near all-time highs, Q2 GDP has been upgraded twice this quarter, and earnings are still growing. Three pockets of real pain right now worth watching: healthcare stocks are in a crowding unwind with names down 20-40% in single sessions; exchange stocks are getting hit hard on CFTC news around perpetual futures, with CBOE, NDAQ, and CME all down sharply; and software is starting to roll after its massive run.

The risk that flips the narrative is oil and bond volatility. If Iran escalates further or the tariff picture worsens, that combination is what ends the bullish call, not the data alone. Consider hedges in energy and volatility if running momentum-heavy or cyclical-heavy books.

Today: ADP at 8:15am. ISM Services at 10am, where prices paid and delivery times matter more than the headline. Beige Book at 2pm for the Fed’s own read on the macro picture. AVGO after the close.