Breakfast Bites - Earnings warning of slowdown

FedEx, Nike, Lennar and Micron all fall after earnings

Rise and shine everyone.

US Equity Futures are lower this morning. Yesterday, earnings after the close failed to impress. FedEx was down -9%, Nike down -7%, Lennar down -4% and Micron down -3%.

MU stock initially rose nearly 6% in the after-market but lost momentum as investors grew frustrated with margin weakness and a lack of visibility, likely leading to downward earnings revisions. Concerns include the stock being overheld by hedge funds and the absence of strong results to support its valuation, despite outperforming SOX and NVDA YTD. Citi’s Chris Danely highlighted that revenue levels are similar to three years ago, yet gross margins are 10 points lower, raising doubts about their ability to recover to previous highs.

FedEx reported Q3 earnings of $4.51 per share on $22.2B revenue, slightly missing profit expectations but beating revenue forecasts. The company lowered its full-year outlook to $18.00-$18.60 per share, citing U.S. industrial weakness.

Nike posted Q3 revenue of $11.27B, down 9% YoY but above estimates. The company warned of a tough Q4, expecting sales to decline in the low to mid-teens due to inventory clearing and new tariffs.

Lennar reported fiscal first-quarter net earnings of $520 million, or $1.96 per share, down from $719 million, or $2.57 per share, a year earlier. Revenue rose 5% to $7.6 billion, with home deliveries increasing to 17,834 units from 16,798 units the previous year. Lennar’s stock fell due to weaker-than-expected margins, a decline in average sales prices, and a challenging housing market amid high mortgage rates and inflation.

So clearly, companies are looking for lower growth just as we have been discussing.

In Asia, Hang Seng Tech fell 3%, with the Hang Seng down 2.1%, coinciding with an 83% y/y surge in Hong Kong court winding-up orders to a 15-year high, while its premium over mainland equities neared its widest since 2020. Foreigners made a sharp shift out of Japanese short-term securities (-¥2.3T) into long-term bonds (+¥3.4T), the second-largest weekly purchase ever, as Japan’s CPI came in slightly above expectations and USD/JPY rebounded to ¥149.40. European markets opened lower amid trade uncertainty, stalled EU countermeasures to US tariffs set for April 2, and geopolitical concerns, with Italy’s FTSE MIB leading declines from a 17-year peak.

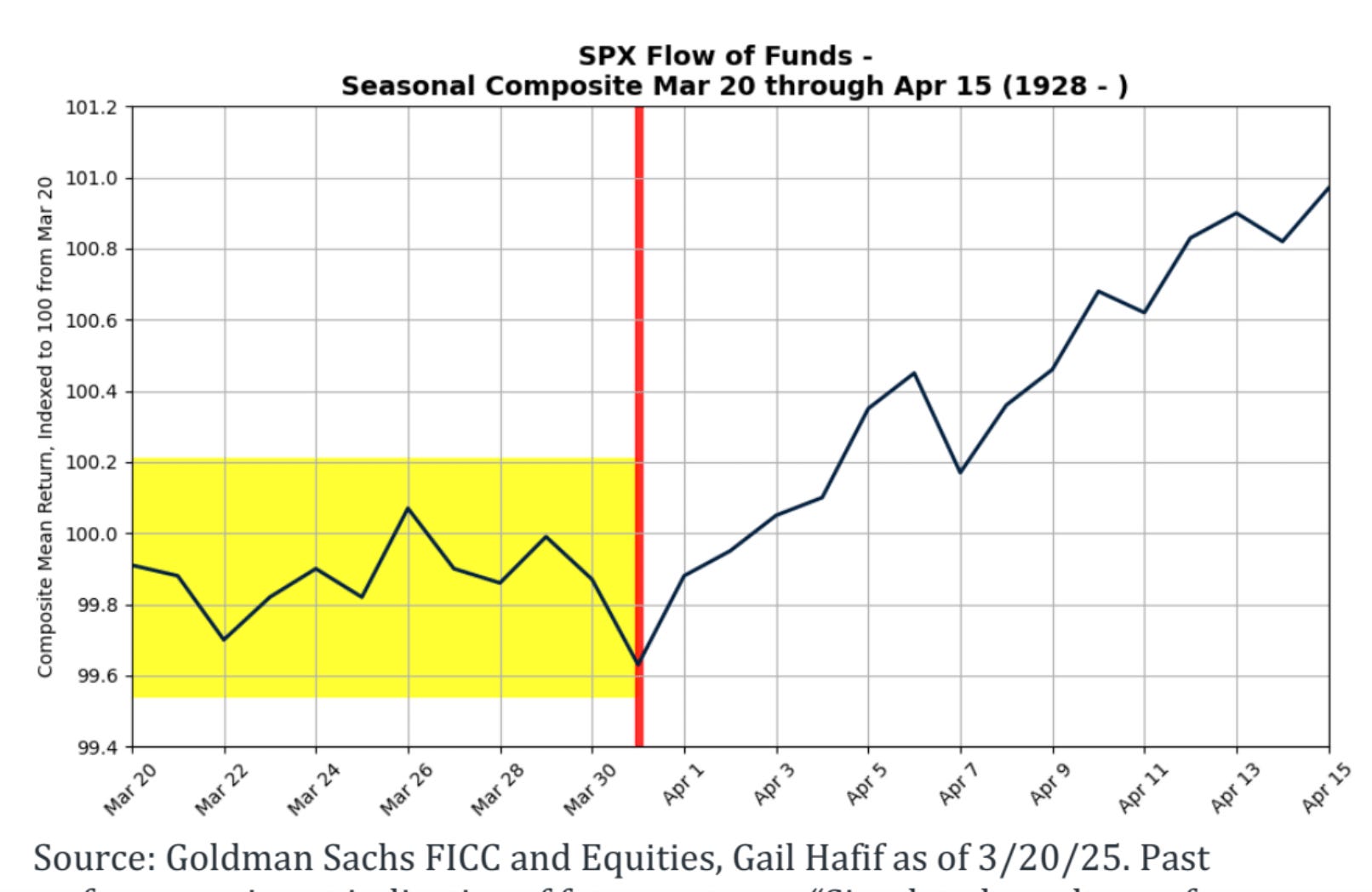

Chart of the Day

Seasonality Outlook: The second half of March has been historically choppy since 1928, and this year appears to follow the same pattern.

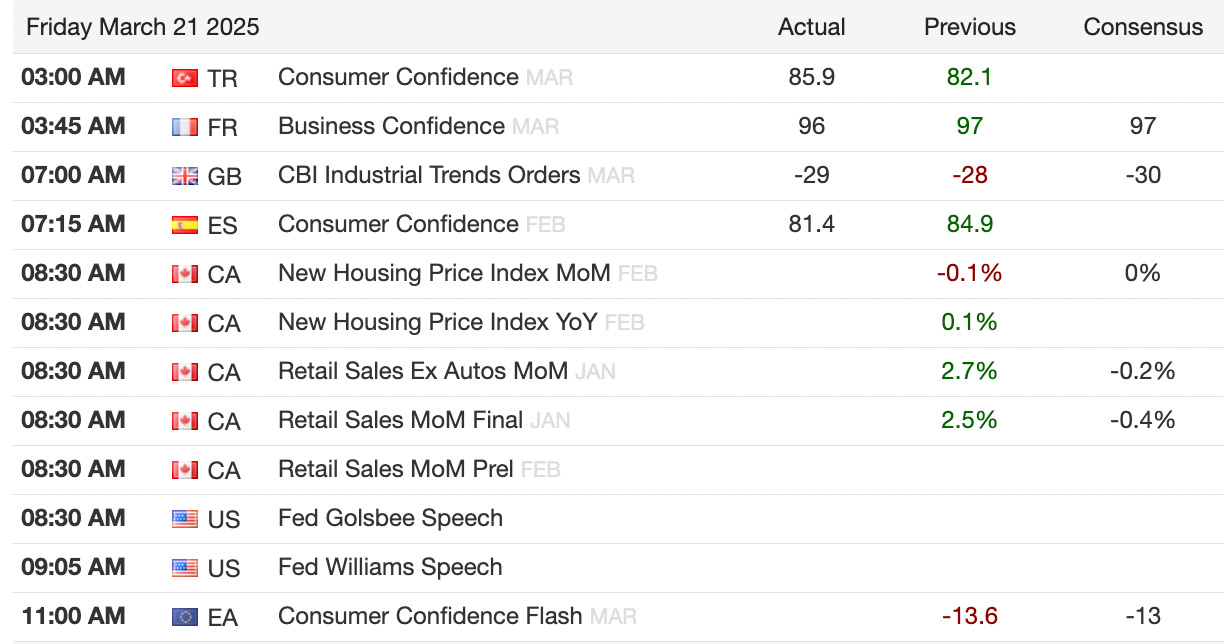

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)