Rise and shine everyone

Happy Friday.

As expected the ECB decided to hold rates at yesterday’s meeting, after a series of cuts. Given that the trade agreement is yet to be reached with the US, it would seem that most Central Banks are taking a wait-and-see approach.

Nikkei fell nearly 1% this morning after a strong two-day rally of more than 5% following the Japan-US trade deal. The Hang Seng also underperformed, down 1% in a weak session for Asian equities overall.

Japan’s June Services PPI came in line with expectations, while July Tokyo CPI was slightly below forecast but still nearly a full percentage point above the Bank of Japan’s 2% target. Rate hike expectations continue to rise, with overnight OIS pricing now implying a 66% chance of a BOJ move by October, up from 61.5% a day earlier.

A major bank has brought forward its BOJ rate hike forecast to October from January 2026. There’s also growing chatter about a potential surprise hike as early as next week. Markets are starting to price in political risk around PM Ishiba potentially stepping down in August or September, especially now that the Japan-US trade deal has cleared a key overhang.

In Australia, President Trump announced that the country has agreed to accept imports of American beef, possibly as a way to preserve its relatively low 10% US tariff rate. Trump added that countries refusing US beef are now “on notice.”

Despite the evolving trade backdrop, markets remain focused on micro drivers as we move deeper into summer and into the heart of Q2 earnings.

Next week brings a heavy slate of reports, with the rest of the Mag 7 set to report. Goldman notes earnings estimates are up 14% for the Mag 7, compared to just 1% for the remaining 493 names in the S&P 500.

We’ll also see a steady stream of labor market data throughout the week, keeping macro in the mix.

Chart of the Day

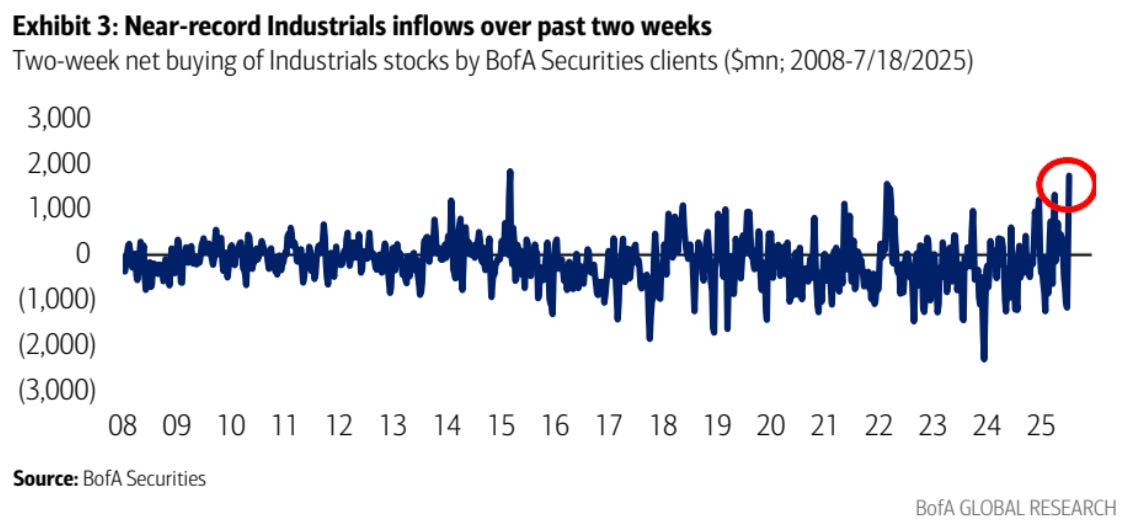

BofA Flow Recap – Broad Inflows, Rotation into Cyclicals

Clients returned to buying U.S. equities last week with $1.8B in net inflows, snapping a three-week selling streak. Flows were broad-based across large, mid, and small caps. Single-stock buying resumed for the first time in a month, while ETF inflows extended their streak to 13 consecutive weeks.

Private clients led the buying, with inflows in 30 of the last 32 weeks. Hedge funds were net buyers for a second straight week. Institutions, however, remained net sellers—offloading equities for the 10th time in the past 11 weeks.

Buybacks picked up as earnings season kicked off but remained below seasonal norms for the third straight week.

Sector-wise, Industrials and Financials saw the largest inflows again, supported by strong bank earnings. Investors favored cyclicals over defensives for a second week. Notably, the rolling two-week inflow into Industrials was the second-largest on record and ranked in the 97th percentile when adjusted for sector size.

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)