Breakfast Bites: CPI Day Reckoning

US inflation data drops into a market already selling off, Iran hostilities escalate overnight, and Oracle reports tonight.

Rise and shine everyone

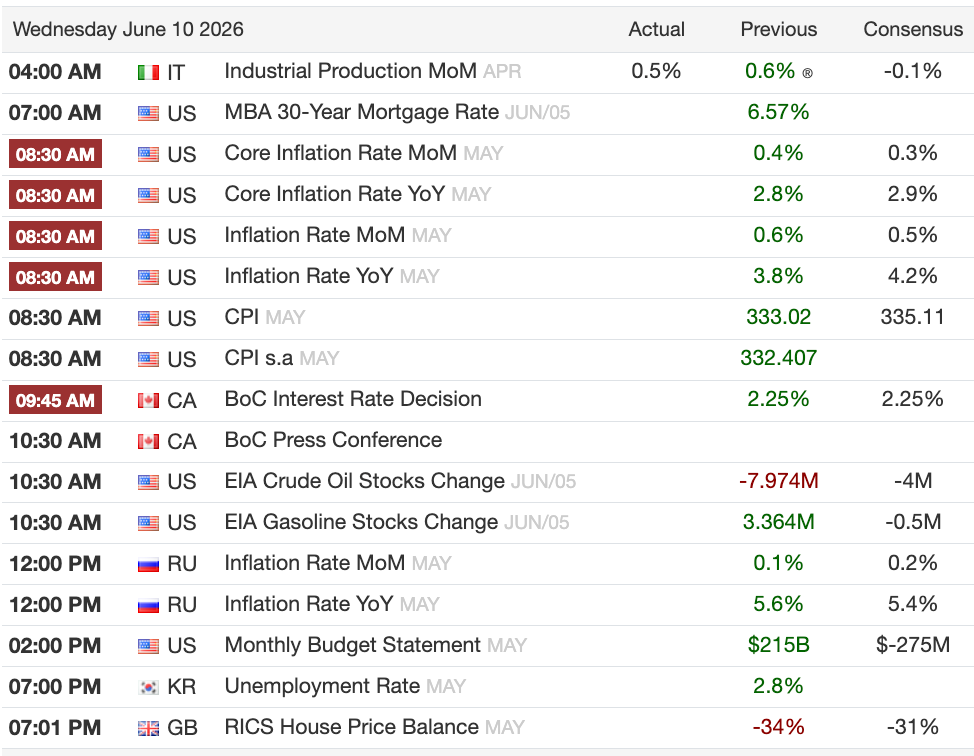

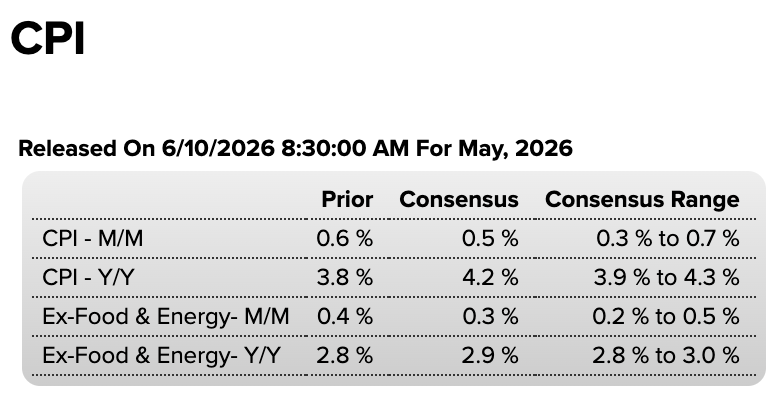

US CPI at 8:30am ET is today’s determining catalyst: a core print above 0.30% MoM could accelerate Fed hike bets and deliver another sharp leg lower in a market already under pressure

US forces struck Iranian air defenses near the Strait of Hormuz overnight; Iran responded with drone attacks on US military bases in Bahrain, Jordan, and Kuwait, putting the April ceasefire at serious risk

Oracle reports 4Q26 after the close tonight: cloud growth acceleration, financing commentary, and any signal on OpenAI's ability to meet its commitments will determine whether the stock's 30% post-3Q26 run holds or reverses into a market with zero tolerance for disappointment

This market does not need a hot CPI print to fall. It is already falling. The Nasdaq dropped 1.1% yesterday, and Asia is heading for its fourth loss in five sessions, with MSCI Asia Pacific down 2.6% overnight. The selling bias is entrenched.

What CPI does today is determine whether the current correction deepens into something more structural. Bond traders have been building hike positions ever since Friday’s jobs report, with some now targeting September for a move. The 2-year yield is at its highest level in more than a year, and US economic resilience alongside rising headline inflation places growing pressure on the Fed to act.

Morning Macro Briefing

Bets on Fed hikes have been building since last Friday’s jobs report, with options on SOFR now targeting multiple moves. The front end is at multi-year highs, and the question has shifted from whether cuts happen this year to whether hikes do.

Three central bank decisions take place within a week. ECB on Thursday, BOJ on June 16, Fed on June 17. Today’s CPI print sets the tone for all three. Markets are pricing more than two 25bp ECB hikes over the next five meetings, and a hot US print tightens the ECB’s view.

Japan’s PPI for May came in hotter, with the yen-denominated import price index rising 25.5% year-on-year, the fastest pace since November 2022. The persistent question remains pass-through to the consumer. Japan has consistently absorbed rather than transmitted PPI inflation, and nothing in the May data changes that thesis.

China’s May CPI printed at +1.2% year-on-year, unchanged from April and slightly below the 1.3% market expectation. PPI ran near 4%, driven by the Iran war supply shock rippling through energy and raw materials. Core inflation ticked down to +1.1%, and Chinese firms are absorbing rather than passing on the shock, which limits inflationary spillover into the global goods supply chain but does nothing to resolve China’s underlying deflation risk.

Indonesia’s central bank surprised with a 25bp rate hike, citing Rupiah stabilization and the need to attract foreign portfolio inflows. The Rupiah initially strengthened but fell back below 18,000/USD during the Asia session. MSCI’s ongoing cautious stance on the country, maintained since January, complicates the inflows thesis.

US CENTCOM struck Iranian air defense positions, ground control stations, and surveillance radar sites near the Strait of Hormuz overnight, using precision munitions from fighter jets. The operation followed President Trump confirming Iran had shot down a US Apache helicopter during a patrol of the Strait, with both crew members rescued. Early indications suggest a Shahed drone collision, though CENTCOM is still assessing whether it was intentional.

Iran did not stand down. The IRGC launched drone strikes against the US Fifth Fleet in Bahrain, with state media also reporting attacks on US military facilities in Jordan and Kuwait. Iran’s foreign minister stated the country “will leave no attack or threat unanswered.”

The April ceasefire is under real stress. Trump continued to reiterate that a deal remained “close” and possibly within “two or three days,” and Pakistani-led mediation continues. But every day of renewed hostilities is another day of elevated energy costs embedding into the inflation data.

Brent rose as much as 1.3% to near $93 before erasing gains and trading around $91.35. Kuwait offered crude to Asian refiners for the first time since the war began, a tangible sign that Persian Gulf shipping flows are gradually recovering despite ongoing Strait of Hormuz risk. Many vessels are still sailing with transponders switched off.

Israel and Iran agreed Monday to halt mutual strikes following a fresh flare-up, with Netanyahu saying Israel would hold fire for now. Israel signaled continued pressure on Hezbollah in Lebanon regardless. The Houthis imposed a “complete ban on maritime navigation” for Israeli vessels in the Red Sea, adding another front to an already multi-front conflict.

The equity supply calendar is becoming a legitimate market overhang. Super Micro’s announcement of a $7B equity financing transaction to fund AI orders sent the stock down an aggregate 14%, doubling its 7% regular-session loss. This comes alongside Alphabet’s roughly $80B equity offering and SpaceX’s $75B IPO expected by Friday, with SoftBank reportedly stalled in its attempt to secure a $6B loan backed by its OpenAI stake.

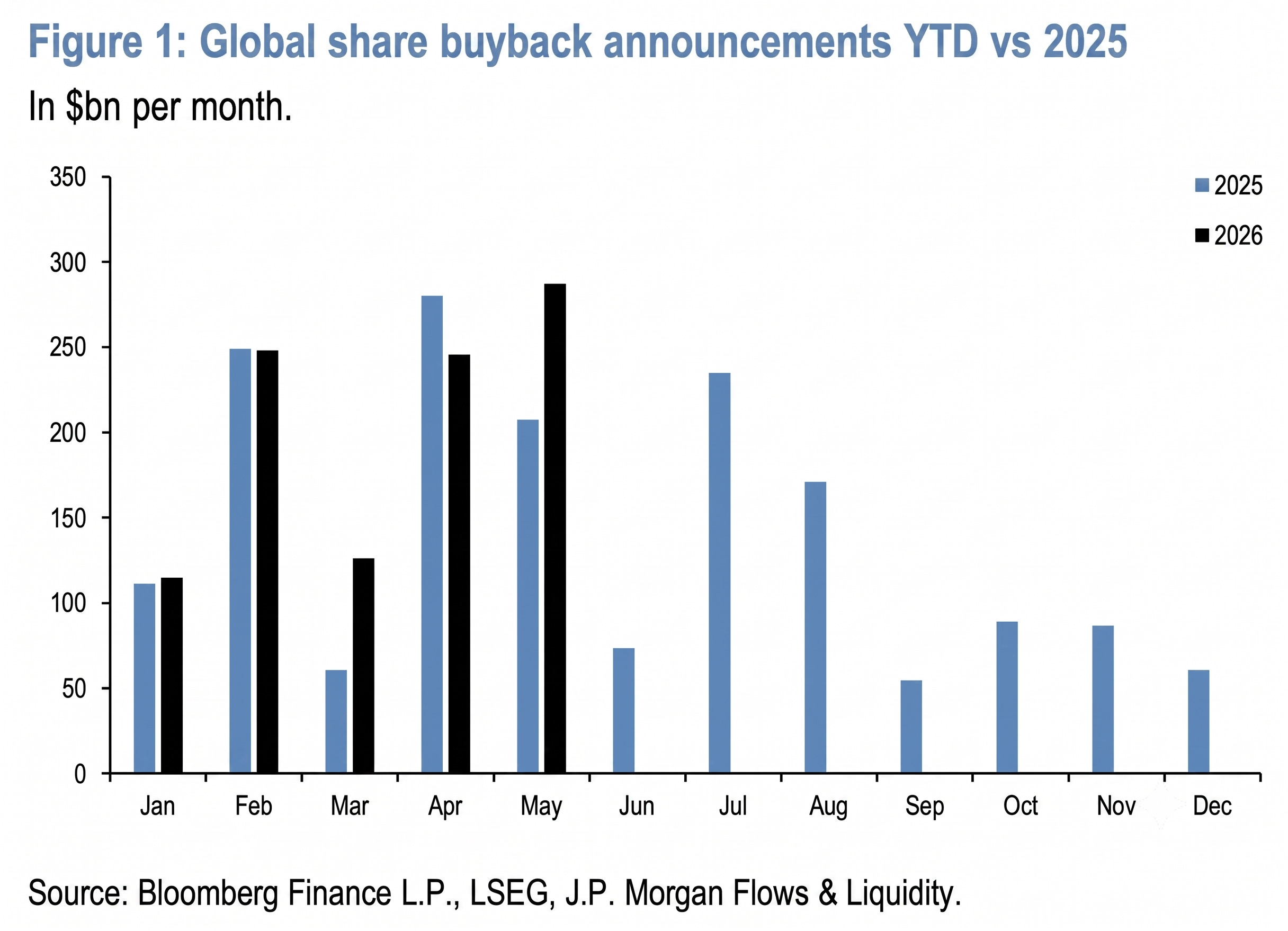

JPM’s flows team offers important context on net supply. Global buybacks reached $533B in April and May alone, a record two-month pace, putting 2026 on track for a nearly $1.9 trillion annualized run rate. According to JPM’s Nikolaos Panigirtzoglou, net equity supply for 2026 is only expected to increase by around $200B versus last year despite the coming issuance wave. That is a structurally supportive backdrop over time. It does not prevent near-term indigestion as the market absorbs a large slug of new paper in the middle of a correction.

China is considering a $295B AI data center build-out over five years, a state-led push that would far outstrip private investment forecasts and puts question marks over other sectors that have enjoyed CCP support. Taiwan is said to be weighing stricter AI chip export curbs to China, aligned with US policy. Xi’s first trip to North Korea since before Covid saw the two nations agree to expand cooperation, a reminder that the geopolitical map is being redrawn on multiple axes simultaneously.

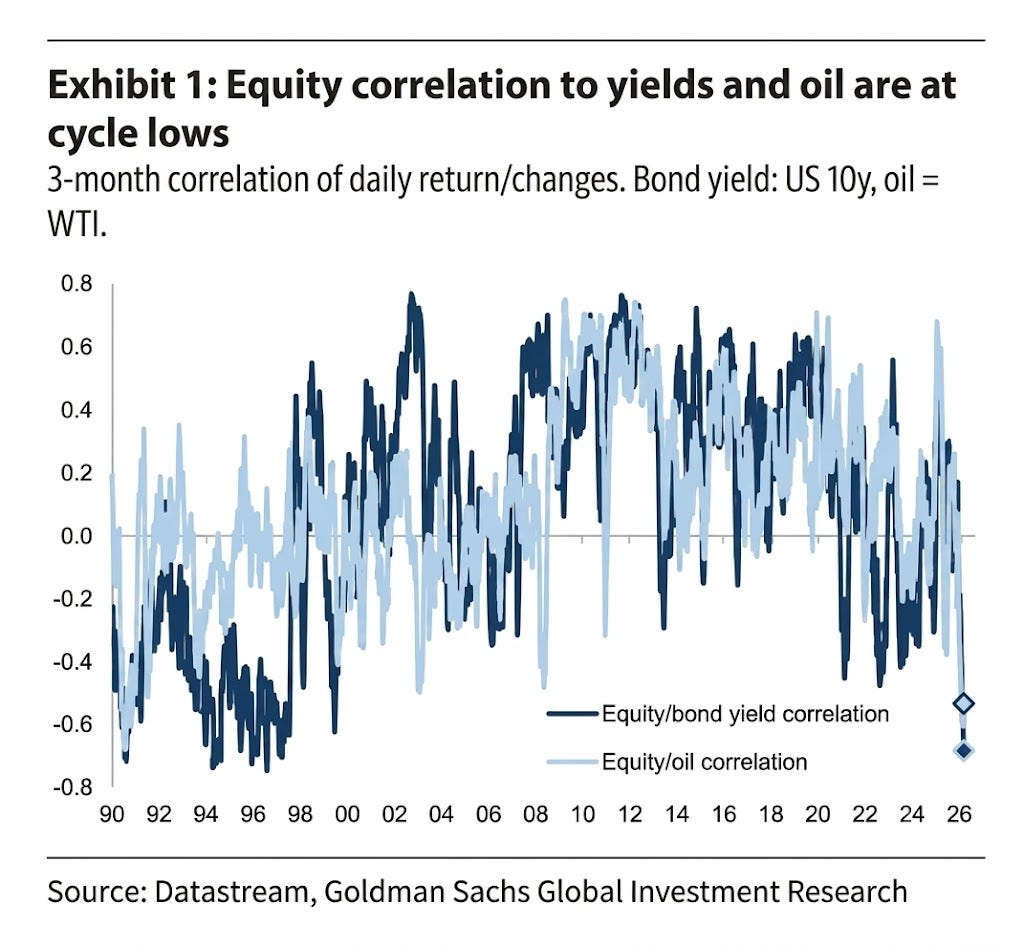

Chart of the Day

This chart shows the 3-month correlation between equities and bond yields, and between equities and oil, both sitting in deeply negative territory at cycle lows. That means rising yields hurt equities and rising oil hurts equities — the market has moved into a regime where both traditional growth signals are now headwinds rather than tailwinds.

Yesterday’s session illustrated exactly why this matters: yields fell 4-5bp, oil dropped 3%, and equities still finished lower. Even with both supposed headwinds easing, the market could not find a bid.

When correlations are this deeply negative, the relief rally everyone is waiting for requires both yields and oil to fall simultaneously and meaningfully — and stay there. Today’s CPI print will determine whether that is on the table or whether the pressure builds further heading into next week’s Fed.

Calendars

US CPI Preview

Consensus expects headline CPI to accelerate to 4.2% year-on-year from 3.8% in April, driven primarily by energy. JPM’s Michael Feroli forecasts headline MoM at +0.58% and core MoM at +0.27%, putting core year-on-year at 2.9%. Goldman’s economists are meaningfully more dovish, seeing core at just +0.17% MoM, a year-on-year rate of +2.79% against the consensus +2.9% — an unusually large divergence between the two houses this month.

Goldman’s softer call rests on shelter moderation, with both OER and rent forecast at +0.22%, and a benign autos print with used car prices flat and new vehicles up only +0.1%. Airfares are expected up 2% in May, capturing direct passthrough of elevated jet fuel prices since the Iran war’s onset. Potential residual seasonality in the communications category, which has declined every May for the past three years, provides additional downward pressure in Goldman’s model.

The wildcard sits in core services. Goldman expects energy to contribute around +4.2% MoM to headline, while core services ex-shelter has been grinding higher — and that is where persistent inflation from the Middle East is most likely to show up over subsequent months. If shelter stays contained and goods behave, the Goldman undershoot case is credible. But JPM flags that elevated oil prices will keep boosting core inflation and risks remain tilted to the upside if Middle East disruptions are more prolonged.

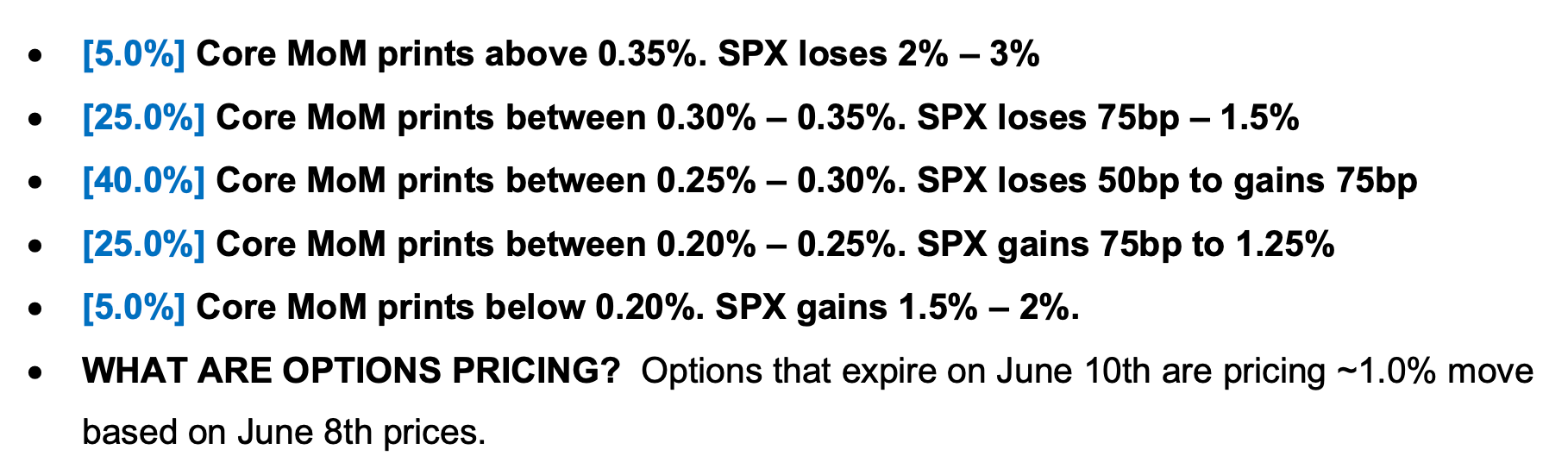

Options expiring today are pricing roughly a 1% SPX move, meaning the tails are underpriced in both directions — and given tech sitting at the 73rd percentile of crowdedness with longs already unwinding, the downside tail is the one that matters more today.

Market Prep

Tuesday’s session ended with SPX -0.3%, NDX -1.1%, RTY +0.4%. Oil-sensitive and yield-sensitive names outperformed as WTI fell 3.1% to $88.38: Airlines +4.6%, Housing +4.3%, Retail +2.5%. Bond yields finished 4-5bp lower, and the tech selloff extended for a second straight day with software, semis, and AI photonics among the worst performers.

The sell-off continues this morning. Nasdaq futures are -0.6%, the Kospi is down -6.5% extending the most extraordinary whipsaw in Asian equities this year, and the Nikkei is off more than -2%. Gold has dropped -1.5% to around $4,200, now roughly a fifth below its pre-war peak after breaking its 200-day moving average, weighed down by rising rate hike expectations. Bitcoin is down over -1% to around $61,200.

Dealer gamma positioning matters today. Options expiring on CPI day are pricing roughly a 1% SPX move; a hot print into a negative gamma environment could amplify the downside considerably. JPM’s delta-one desk highlighted puts on QQQ or high beta as the cleaner short-term expressions, and flagged that a CPI replay of last Friday’s jobs report could trigger momentum unwinds as the key rotation. The de-escalation shorts basket remains relevant if any Iran deal headlines break during the session.

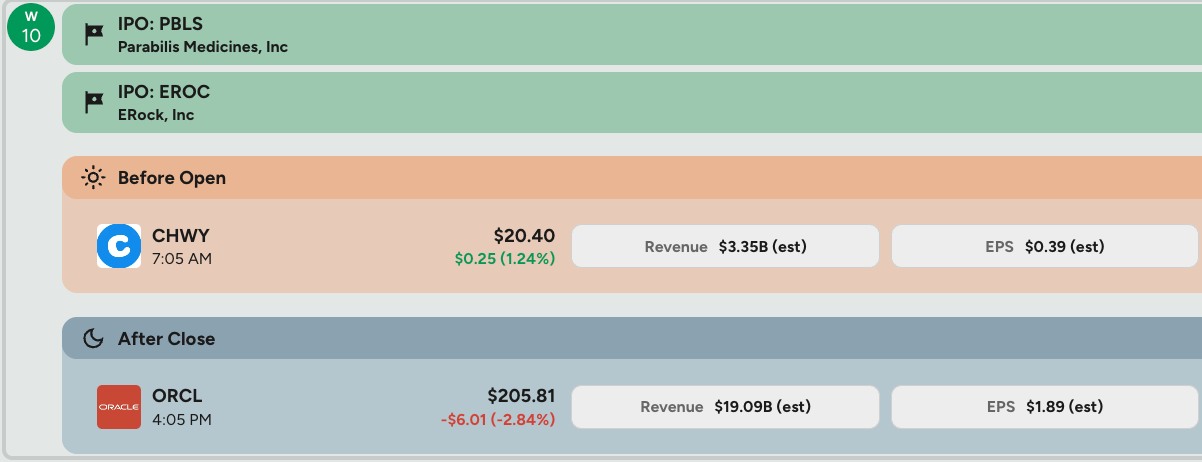

Oracle reports 4Q26 after the close tonight. The stock has already run 30% since the 3Q26 print and 45% since March, leaving little room for disappointment. With consensus non-GAAP EPS at $1.97 and total revenue around $19.1bn, the bar for a positive reaction is high.

The key number to watch is Cloud PaaS/IaaS growth, expected to accelerate to 94% year-on-year from 84% last quarter as incremental data center capacity comes online and enables RPO recognition. Cloud now represents 52% of total revenue versus 44% a year ago, making margin trajectory and new compute deal announcements increasingly important reads on the business. Any acceleration in cloud margins would be a genuine positive surprise.

The harder question is the balance sheet. Capex is expected at around $11bn in the quarter alone, with free cash flow running deeply negative at roughly -13% margin. The market will be listening carefully to any commentary on financing needs, with estimates suggesting Oracle needs to raise tens of billions more over the next few years to fund the buildout.

The risk hiding in plain sight is OpenAI, which represents more than 50% of remaining performance obligations. Any signal that OpenAI is struggling to meet revenue targets or access sufficient capital is a direct hit to Oracle’s backlog story. In a session already selling off into CPI, a miss or soft guidance tonight would not stay contained to this stock.

Watch the 10-year yield reaction at 8:30am first. Equities will follow rates, not the other way around today. A print that meaningfully surprises in either direction resets the narrative heading into next week’s Fed.

Today’s dominant catalyst is CPI and Real Average Hourly Earnings at 8:30am ET, with the Bank of Canada also deciding at 9:45am ET. Oracle reports Q4 after the close alongside Chewy and CNM. The ECB meets Thursday with PPI and jobless claims on the same morning, and Adobe reports after the close.