Breakfast Bites - Copper jumps on tariff news

US Macro & sentiment data not so stellar; UK Spring Statement in focus

Rise and shine everyone.

Copper futures are surging, as President Trump discussed implementing copper tariffs within weeks. Prices spiked crossing 5.35, as the news came in.

Yesterday market volatility returned to the US on macro news releases.

The standout was the sharp rebound in the S&P Global US services PMI, which came in above expectations. The strength wasn’t just on the surface — new business and employment components both moved higher, suggesting that demand in the services sector remains solid.

In contrast, the manufacturing side told a different story. The S&P Global US manufacturing PMI slipped back into contraction territory and fell more than expected. The underlying details were weak across the board, with output, new orders, and employment all declining. The Richmond Fed’s regional manufacturing index confirmed the broader trend, falling to -4 versus expectations of a small positive print. Business conditions in that survey dropped sharply to -14, and new orders also softened.

One theme across both surveys was rising price pressure. Input and output prices increased for both services and manufacturing, and S&P noted that companies are now attributing much of the input cost inflation to tariff policies. That’s worth watching, especially if supply-side drivers begin to complicate the disinflation narrative the Fed has been hoping for.

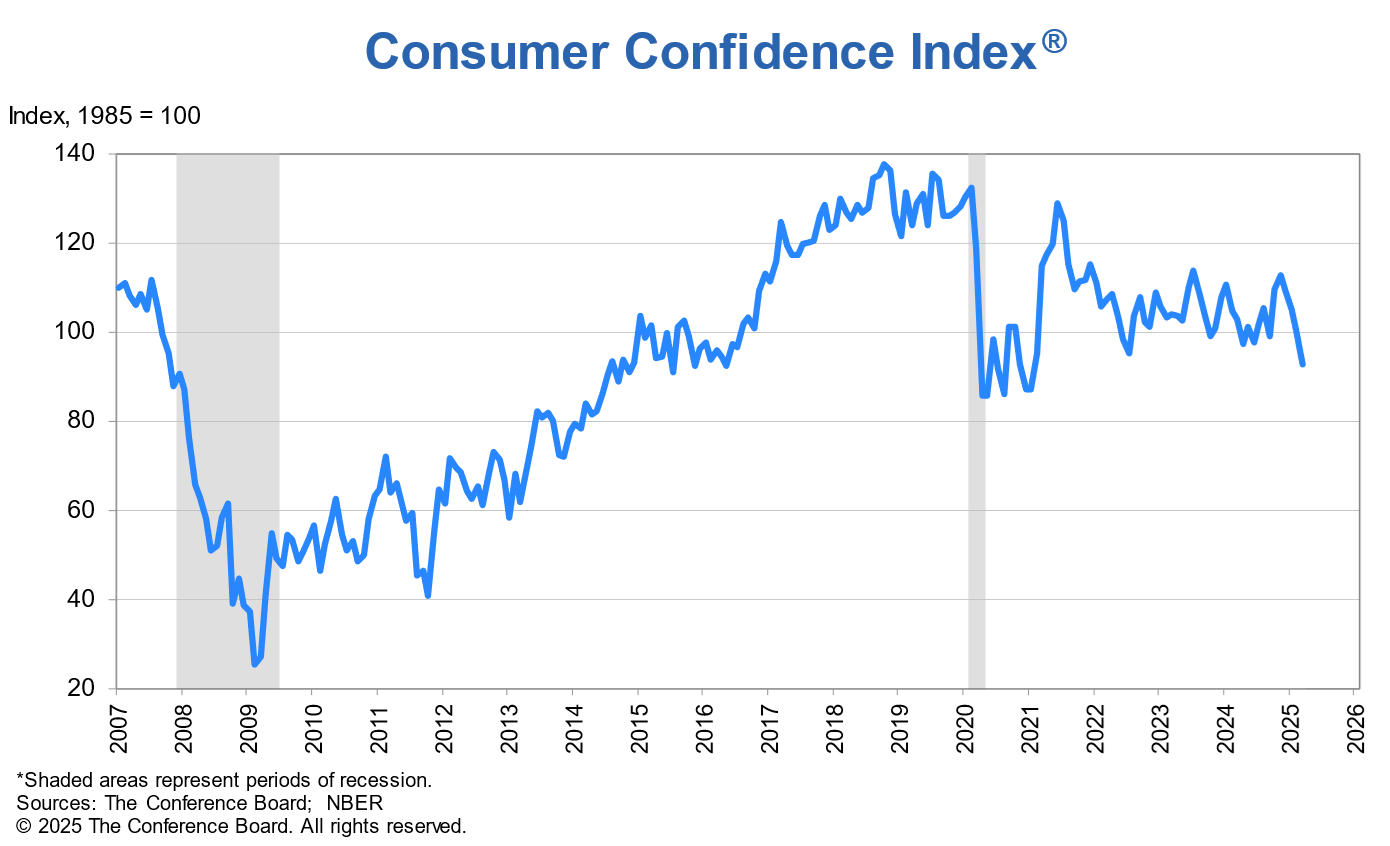

On the consumer front, sentiment continues to weaken. The Conference Board’s Consumer Confidence Index fell to 92.9 in March, below expectations and marking the lowest level since July 2022. Concerns around the labor market and income expectations appear to be weighing on households, even as services activity looks strong on the business side.

US Housing data added another layer to the story. New home sales in February came in slightly below expectations at 676K, while home prices continued to push higher. The S&P CoreLogic 20-City Home Price Index rose 0.5% month-over-month and is now up 4.7% year-over-year. We’re seeing a familiar dynamic: prices are rising even as sales slow, which speaks to tight inventory and affordability issues. Higher mortgage rates haven’t fully cooled the market, but they’ve certainly made it harder for new buyers to step in.

Internationally, Asian equities had a calm but upbeat session. The Kospi and Nikkei both climbed over 1%, despite the absence of major headlines or catalysts. It was a sentiment-driven move, with traders largely shrugging off recent global uncertainty.

In Japan, Governor Ueda continued his third day of parliamentary testimony. He reiterated much of the same messaging, avoiding any direct comment on FX. However, he noted that the belief prices and wages won’t rise in Japan is “fading,” even if the overall price trend still lingers below the 2% target. Markets took his tone as dovish, and the yen weakened further. USD/JPY pushed back up to the 150.50 level.

Over in Europe, equities were more cautious as investors braced for US tariffs taking effect April 2nd. The focus remains on Trump’s “dirty 15” list and potential auto levies. Reports of a phased approach and possible exemptions offered limited relief, but new mentions of copper tariffs kept sentiment in check.

UK macro data came in slightly softer, with inflation easing to 2.8% in February from 3.0% — a touch below expectations. However, services inflation held steady at 5%, suggesting persistent underlying pressures. Markets are now pricing in about a 70% chance of a May rate cut. Attention is shifting to Chancellor Reeves’ Spring Statement, with expectations of spending restraint amid a £1.6 billion fiscal shortfall and likely OBR downgrades.

US Equity Futures are glat to higher this morning. 2Y yield is lower but the longer term yields are higher - the curve seems to be steepening. The real standout is the commodities complex.

Chart of the Day

US High Yield Spreads are nowhere close to signaling a recession. The light blue bars indicate a recession in the chart below, and we can see the spike in spreads, as the economy starts to enter a recession.

What We’re Watching

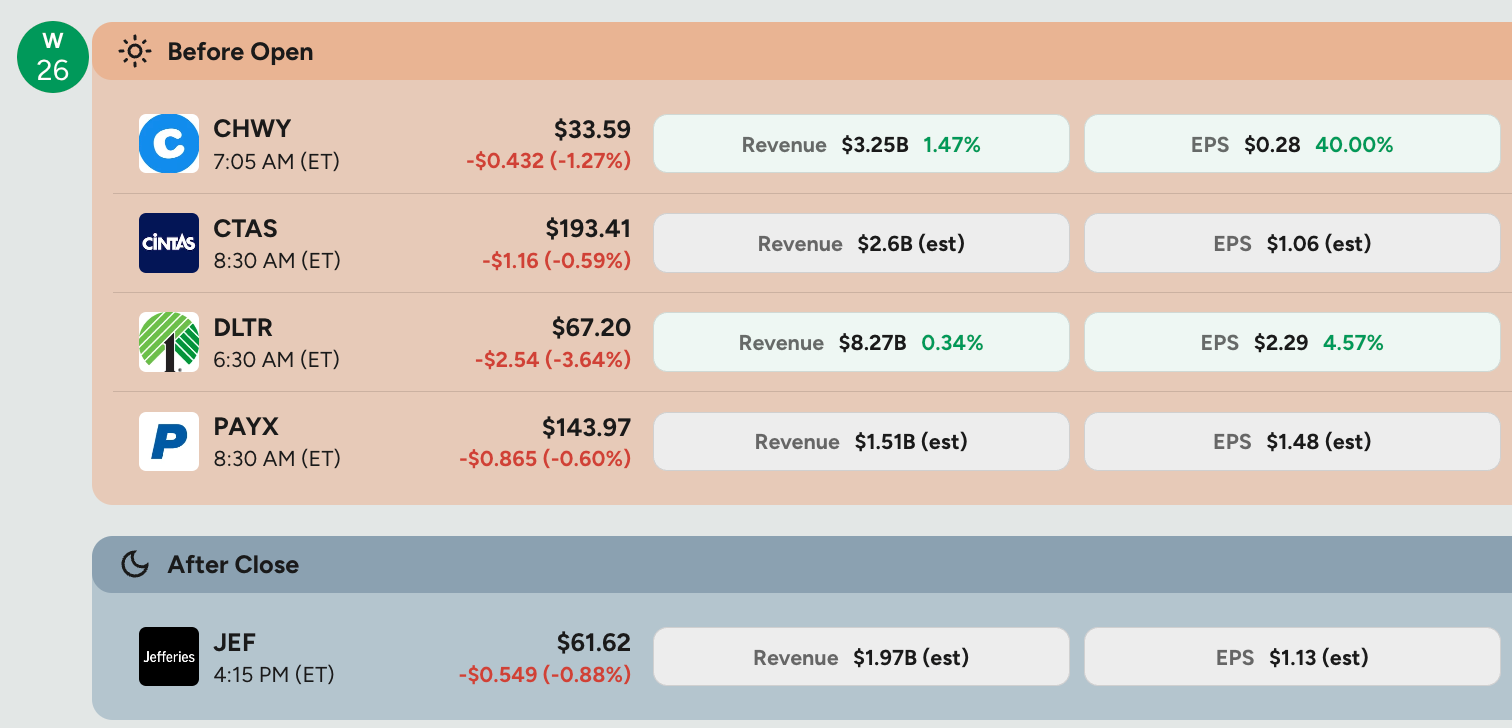

No macro data of note. We do have a few interesting earnings before the open - watch for Cintas and Paychex, both of which can give us clues to small business performance.

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)