Breakfast Bites - Contradictions

China willing to talk; Nvidia faces profit hit from chips to China; Liquidity still weak; Powell speech at 1:30 pm ET

Rise and shine everyone

We’ve had quite a few developments overnight, and early this morning.

The latest on the trade war is that China is open to talks if the President can rein in cabinet members and show some consistency. The market spiked on this news but promptly gave up half the gains.

Earlier in the day, China replaced its main trade representative, and true to form, didn’t provide a reason. At the time, the foreign ministry was still reiterating that the US should use dialogue, not pressure or bullying, to resolve disputes.

President Xi also encouraged Chinese enterprises to invest in Malaysia and welcomed additional Malaysian agricultural products. Other news suggest that China is making a deal with Australia for beef and will stop importing from the US.

So, quite a few contradictory issues are going on. But the reaction probably came as news floated about that China could face up to 245%.

Speaking of contradictory, yesterday’s White House Press Conference celebrated a win with Nvidia moving manufacturing to the US. And later, they said, be that as it may, Nvidia would still need export licenses for China. It seems that this will result in a $5.5B charge in Q1:2026 associated with its H20 chip, which will reduce the company’s bottom line. The stock sold off hard in the after-market -7%, and continues to struggle in the pre-market.

This is weighing on the global chips market. Japanese chips stocks were down. ASML shares are also trading lower after the company reported Q1 2025 net bookings that fell short of expectations. While ASML maintained its full-year revenue and margin guidance, management flagged tariffs as a fluid and disruptive near-term risk, adding to investor caution despite the steady outlook.

We also heard from the EU yesterday that they expect most US tariffs to stay put after little progress was made in trade talks this week. Markets didn’t like that yesterday at all.

So again, we’re still in an event-driven market and this choppiness will only likely resolve once we get full clarity on what’s happening on the tariff front.

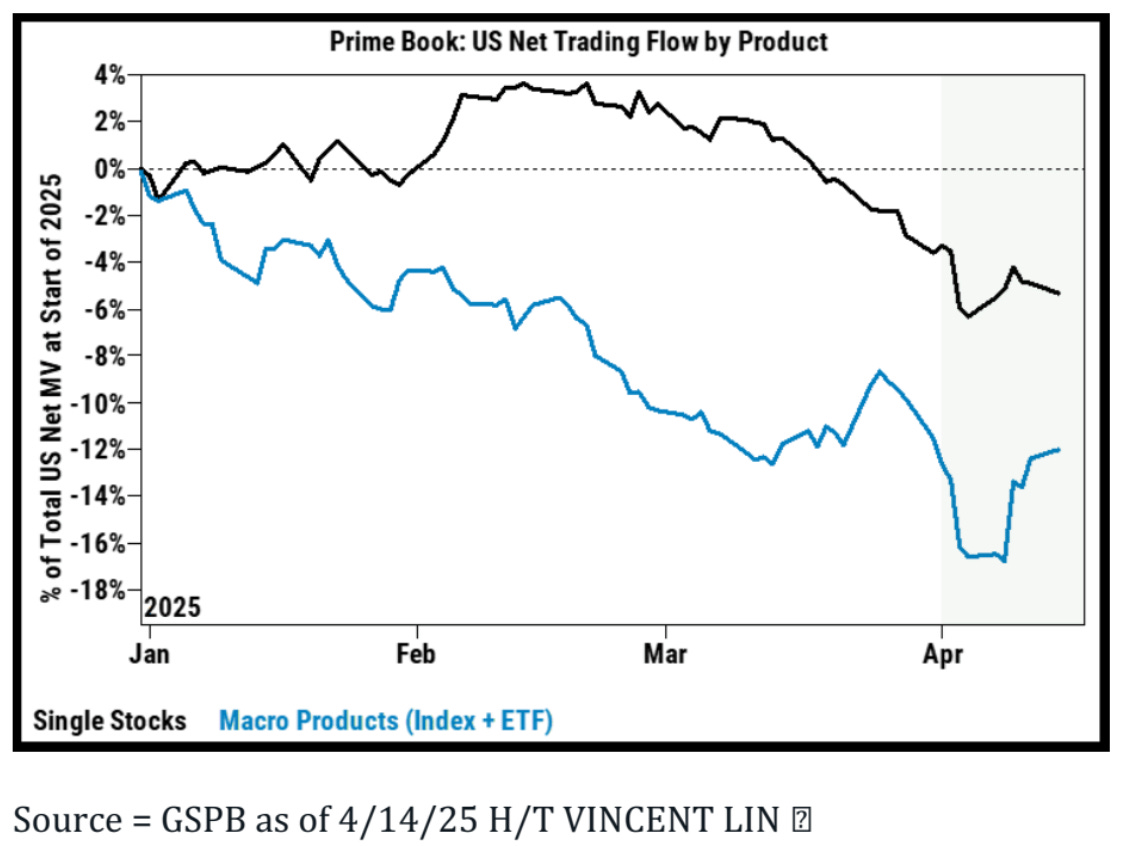

At this stage, we’re not seeing the big buyers step back, neither are we seeing much fund flows, particularly in single stocks. Liquidity continues to remain and thin, and the flight from US assets is quite clear from the drop in the US dollar.

EIA 2025 Energy Outlook: Oil to Peak in 2027, Energy Demand Slows

The EIA’s Annual Energy Outlook 2025 projects US oil production will peak at 14 million bpd in 2027, then ease to 13.31 million bpd by 2030. Total oil product demand is expected to reach 20.52 million bpd in 2026, marking a post-pandemic high.

Meanwhile, US energy consumption is projected to decline over the next several years and doesn’t begin rising again until the early 2040s. In most scenarios, 2050 consumption is lower than 2024 levels.

The report outlines several scenarios:

High oil price case sees Brent at $155/bbl by 2050 (vs $91 in the reference case and $47 in the low case)

High supply case assumes stronger recovery rates and faster tech improvements

Low zero-carbon tech cost case sees 40% cost declines by 2050

High economic growth case assumes 2.1% GDP CAGR through 2050

The EIA also upgraded its modeling tools with a new hydrogen module, carbon capture framework, and improved upstream oil and gas resource assumptions.

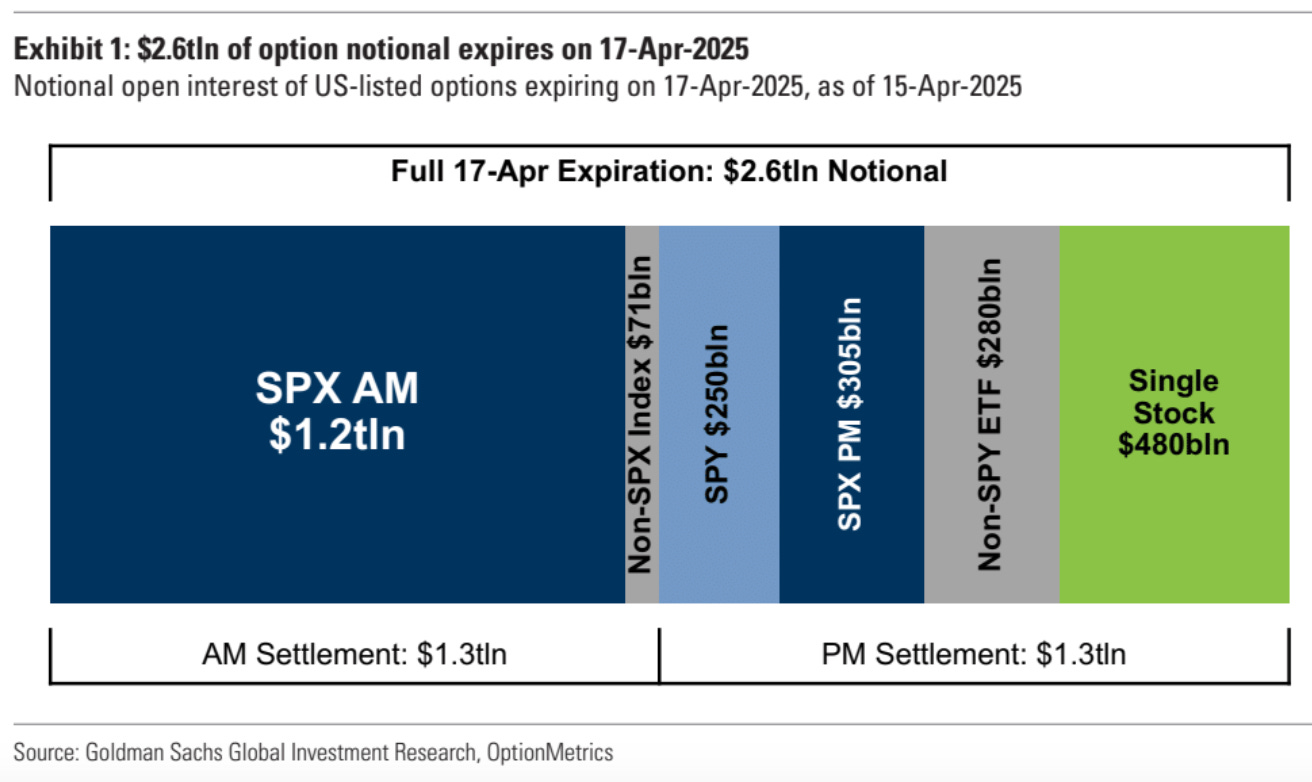

Chart of the Day

Goldman Sachs estimates that over $2.6 trillion of notional options exposure will expire tomorrow (04/17), including $1.2 trillion of SPX options and $480 billion notional of single stock options.

What We’re Watching

1:30 pm ET - Fed Chair Powell Speech

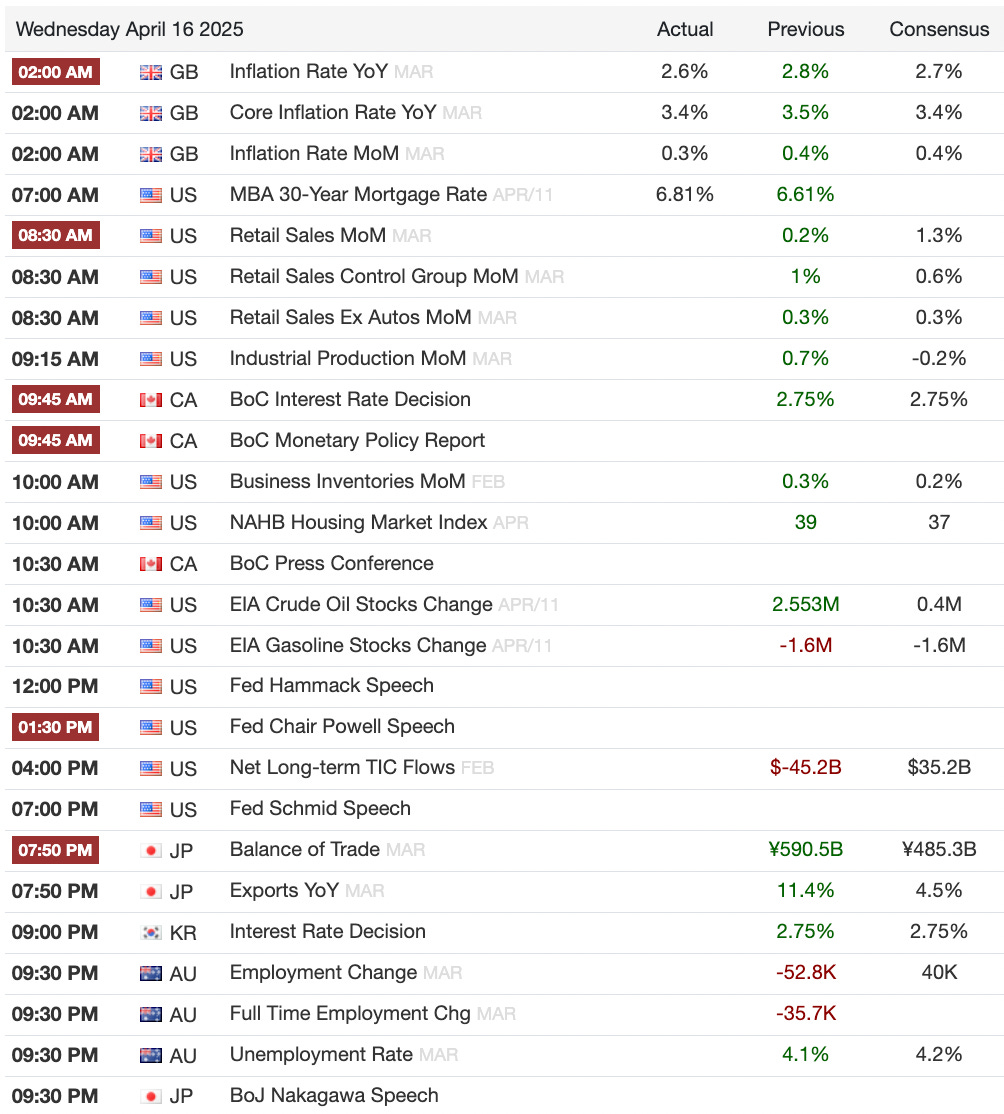

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)