Breakfast Bites - Commodity Tariffs begin

Why US markets are responding positively

Rise and shine everyone

Another Monday morning, another set of tariffs. This time it’s 25% tariffs on steel and aluminum being imported into the US.

The reaction has been different though. While we’ve seen the US Dollar and Commodities strengthen, we’re also seeing a bit of a rally in US equity futures. I believe this has to do with the fact that these new tariffs are very specific and actually fulfill the role of protectionism.

Putting tariffs on steel and aluminum actually helps local US producers such as Nucor and Cleveland Cliffs and supports US jobs. They prevent dumping unfairly low-cost goods and give US producers a chance to compete.

While this may increase some costs for manufacturers, it actually helps to get rid of unfair practices and level the playing field in theory.

Is 25% the right level? That remains to be seen. But the market is certainly liking this angle for now.

The news, however, wasn’t received well by many of the Asian steel producers. POSCO initially dropped 4.0% but pared losses to 1.5%. Hyundai Steel fell 2.5%, while Nippon Steel declined 1.0%. Steelmakers across Europe, including Thyssenkrupp and ArcelorMittal, faced pressure, while US steel rebar futures hovered near CNY 3,300 per tonne. Aluminum futures remained above $2,640 per tonne. Major indices started the week cautiously higher. Commodity currencies like the Aussie Dollar are also feeling some of the pressure.

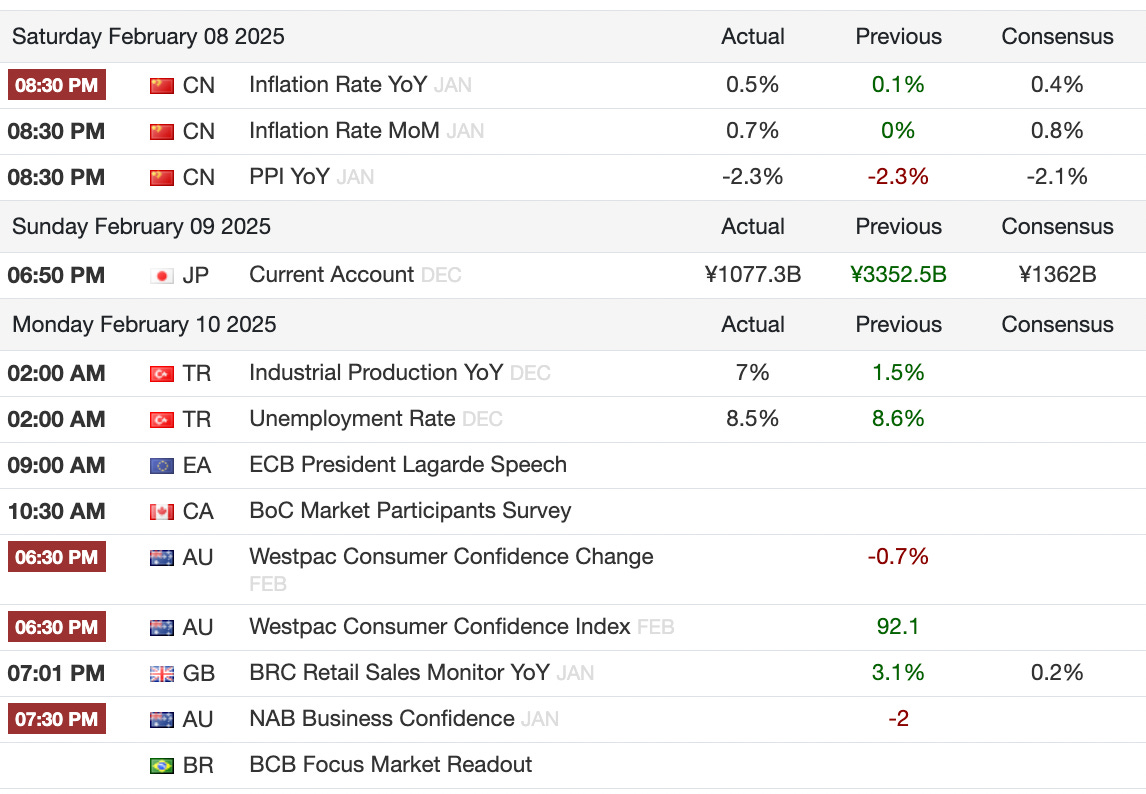

The Hang Seng outperformed, rising 1.7%, while other Asian markets saw limited movement. China’s January CPI came in slightly higher than expected, driven by an early Lunar New Year. However, the temporary boost is likely to be offset in February. PPI remained in deflation at -2.3% for the 28th consecutive month.

Japan’s PM Ishiba finally secured a meeting with former US President Trump. Ishiba committed to doubling defense spending by 2027, increasing Japanese investment in the US to $1 trillion, and reducing Japan’s trade surplus by importing more US energy products. He also pledged AI collaboration, Indo-Pacific security efforts, and progress on North Korea denuclearization. Meanwhile, Nippon Steel appears resigned to a substantial investment in US Steel rather than full ownership.

Japan’s 10-year bond yields edged up to 1.32%, the highest since 2011. The country recorded a record current account surplus in 2024, supported by a weaker yen. The trade balance remained in surplus but only marginally.

On the commodities front, European natural gas futures (TTF) climbed to €58/MWh, the highest since January 2023, driven by colder weather and low storage levels. Gold, silver, and oil are all moving higher this morning.

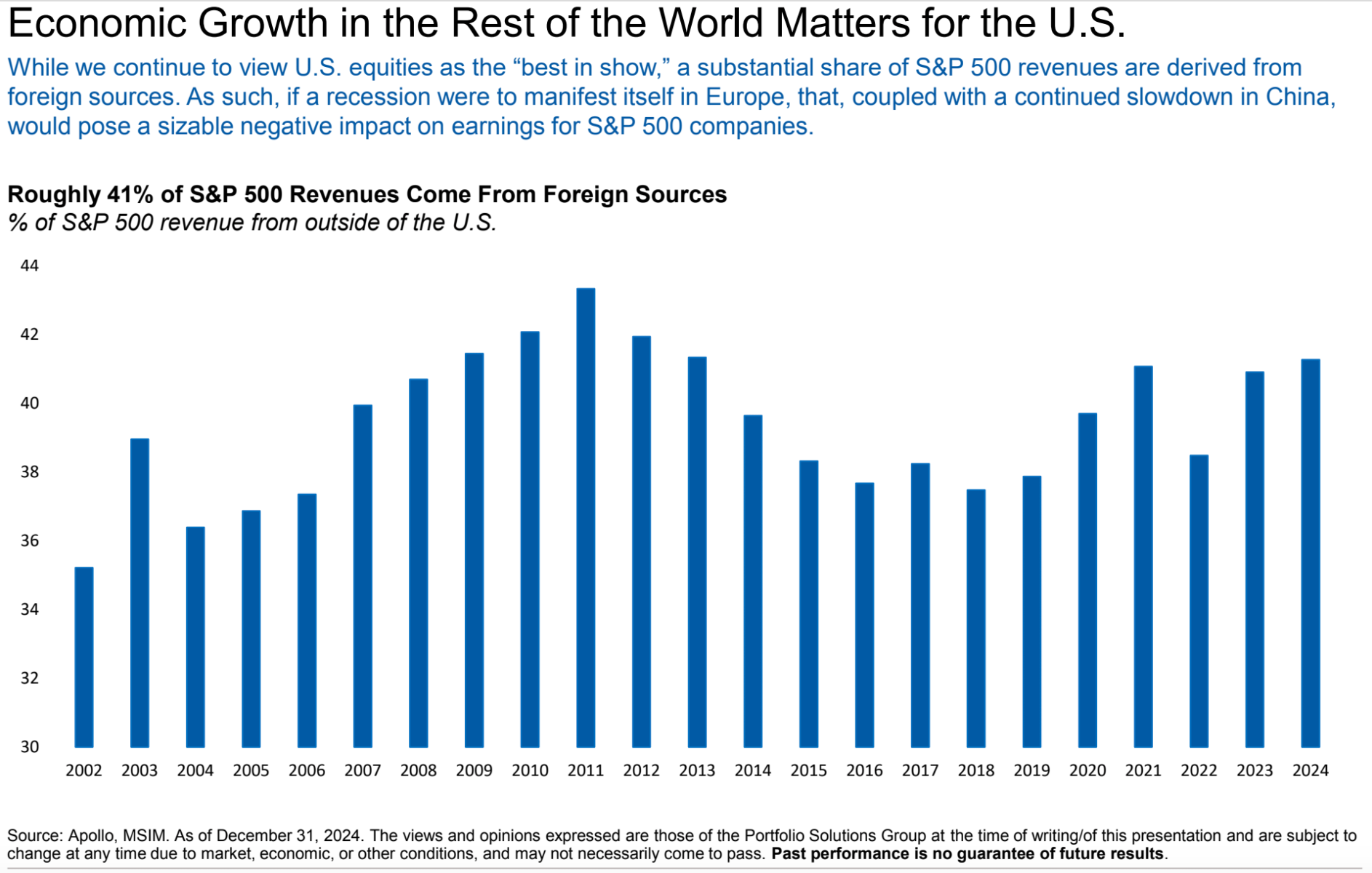

Chart of the Day

About 41% of the Revenues of the S&P 500 companies come from overseas. A stronger US dollar, coupled with Tariffs, could see a slowdown in other countries such as China, and Europe. This could lead to a pullback in revenues for these companies, at least initially. Some companies may eventually make decisions to find alternate sources of revenue, which avoid tariffs, or negotiate special exemptions for their products.

What We’re Watching

Earnings from McDonald’s, Monday.com, Rockwell Automation before market open and Astera Labs (after the close).

Further developments on tariffs

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)