Breakfast Bites: Ceasefire on a Knife’s Edge

US-Iran strikes over the weekend, a last-minute Doha pause, and a pivotal week for the Fed and payrolls.

Rise and shine everyone

The weekend gave us the most intense military exchange of the conflict. US forces struck Iranian military targets Friday night, concentrated in southern Iran and around the Strait of Hormuz. Iran retaliated against Bahrain and Kuwait with missiles and drones on Saturday, and the US responded with a heavier bombardment Saturday night. Iran called it a violation of the ceasefire.

Then, twenty minutes before Monday’s market open, Axios reported that both sides agreed to halt strikes and meet in Doha tomorrow. Everything changed. Oil opened less than 1% higher. US equity futures moved to +0.6%. The de-escalation reflex is intact, but the fragility here is real. US-Iran-UAE tensions are still flaring beneath the surface, and one bad outcome in Doha reverses all of it. Just be wary - the source is Axios.

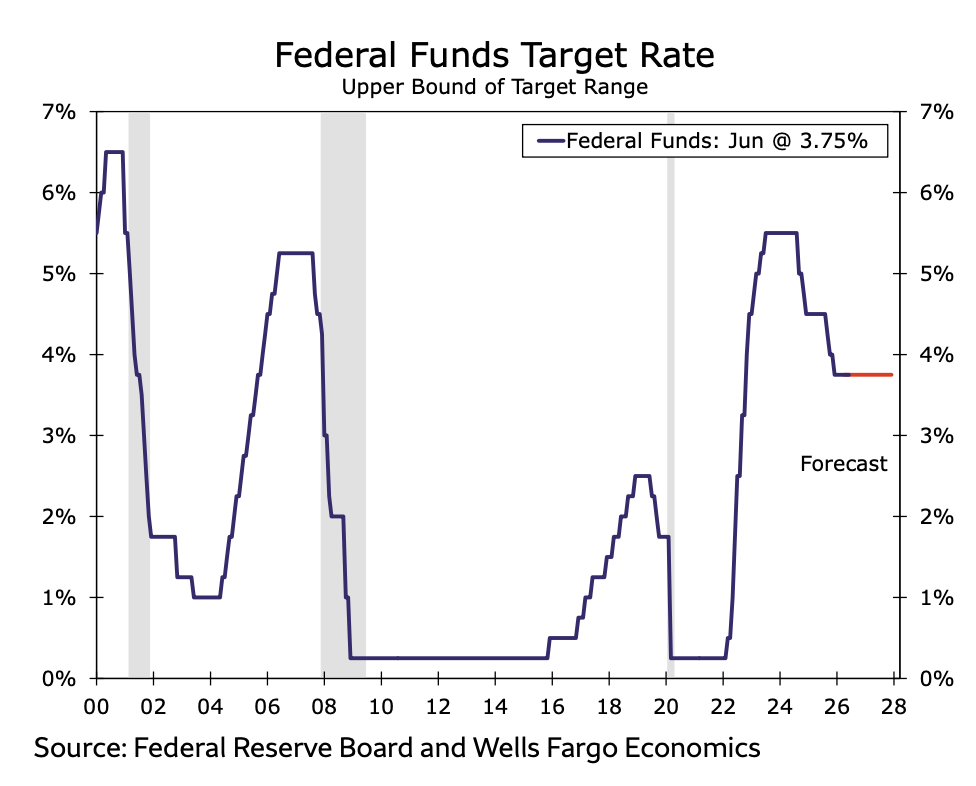

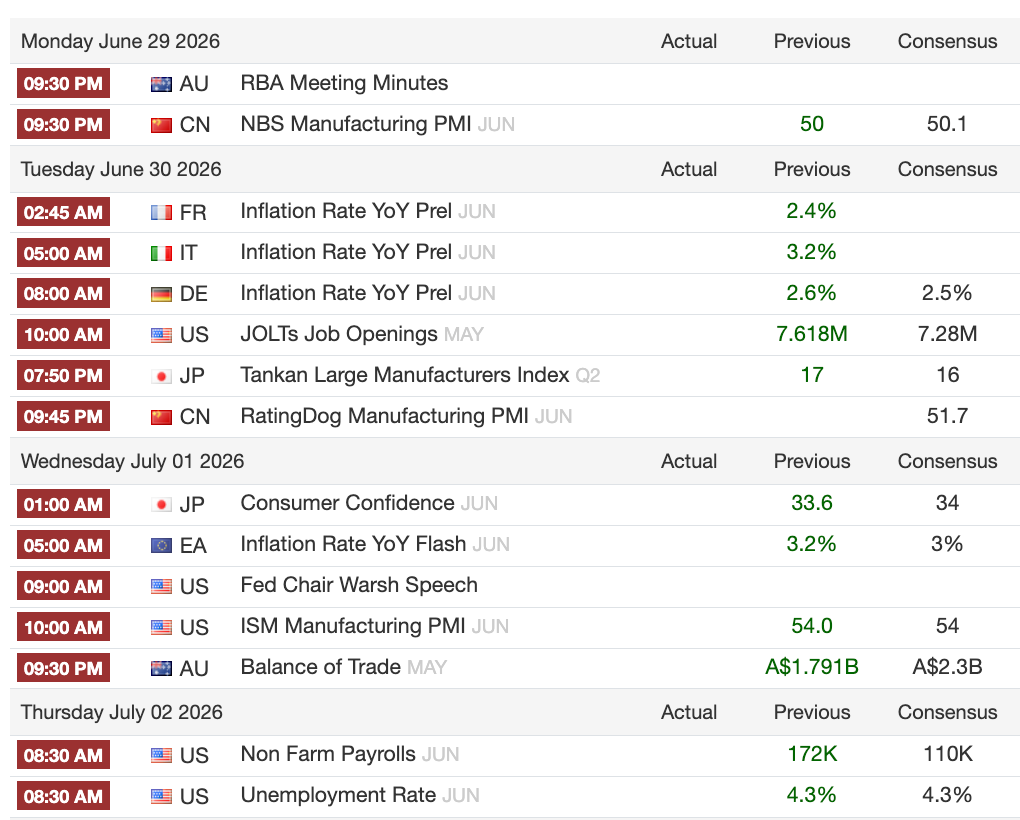

The domestic week is shortened but consequential. NFP prints Thursday morning. Fed Chair Warsh makes his first major international appearance Wednesday at the ECB’s Sintra Forum. A solid payrolls number will reinforce the case for a hold and sharpens the hike debate that markets are already partly pricing. We have 28 basis points of tightening priced through year-end, down from 40bps on June 21.

Here is what we are watching this week:

Whether the Doha talks produce a genuine ceasefire commitment and what that means for oil and the Strait

Warsh at Sintra on Wednesday and any signal he sends on the near-term policy path

Thursday’s NFP print, with GS expecting +130K and Wells Fargo at +120K against a prior of 172K

Morning Macro Briefing

The weekend’s military exchange was serious, but markets decided the Doha meeting changes the equation. The process still points toward a sustained détente, per JPMorgan’s morning note, because neither side is keen on full resumption. The case for expanded oil supply makes Iranian pragmatism structurally attractive. What the ceasefire does not change is the UAE flare-up, which adds a live risk that the market is not fully pricing this morning.

Oil is behaving like a market that believes the diplomatic track holds. WTI fell 8.7% last week, returning to pre-war levels, as Persian Gulf crude exports recovered to at least 75% of pre-conflict flows and Strait of Hormuz shipments reached their highest levels since the conflict began, per Bloomberg data cited by Goldman. A clean Doha outcome could push oil lower still.

The ECB’s Sintra forum runs today through Wednesday July 1. The main event is Warsh on a televised panel at 9:30am ET Wednesday alongside Lagarde, Bailey, and Bank of Canada’s Macklem. It is his first major international appearance as chair. Wells Fargo expects him to stay structural and avoid near-term guidance, focusing on price stability and central bank communication frameworks. That base case is probably right, but any deviation gets repriced fast.

The underlying macro picture heading in is not bad. May core PCE came in at +0.31% month-over-month and +3.38% year-over-year, in line with consensus. Personal spending beat at +0.7% and income at +0.5%. Goldman’s Jan Hatzius nudged H2 GDP up to 2% on lower gas prices and continued AI-driven capex and reduced his 12-month recession probability to 15% from 25%, with Brent now seen at $80 by end-2026. He still bases on no hikes. A few Goldman competitors are now formally penciling them in.

Trump threatened the EU and UK late Friday with 100% tariffs on goods from any country imposing a Digital Services Tax on US firms. The timing is notable with Warsh, Lagarde, and Bailey all in the same room Wednesday. JPMorgan upgraded EU equity targets this morning, seeing 5-10% additional upside on the SoH reopening and normalization in business sentiment coming through in flash PMIs.

Japan’s May retail sales were significantly stronger than expected, nearly +2% month-over-month against a consensus of -0.5%, with the year-over-year reading at +5.0%. This follows strong department store numbers earlier in the week.

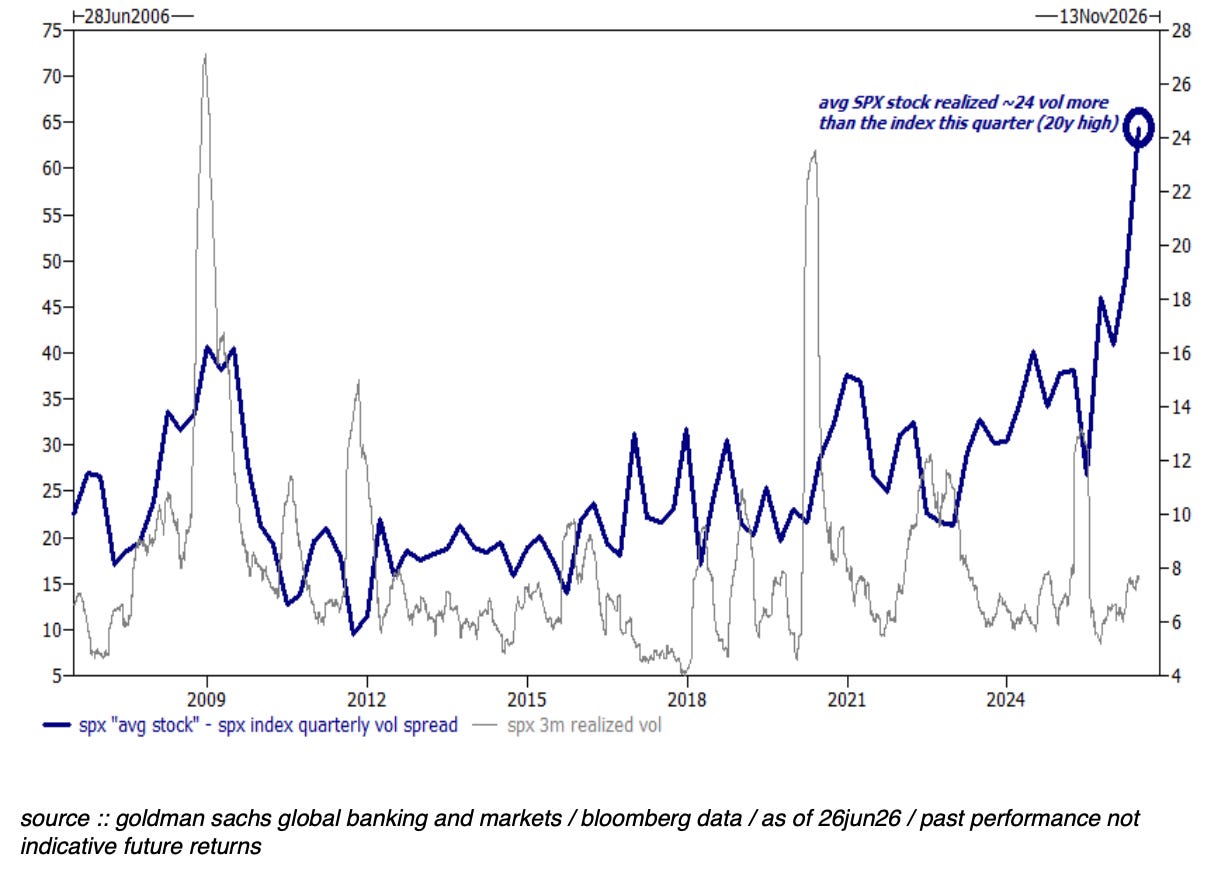

Chart of the Day

The gap between how much individual stocks are moving and how little the index is moving just hit a 20-year extreme. The average S&P 500 stock realized nearly three times the volatility of the index itself this quarter, per Goldman data. That is the most dispersive environment for single stocks in two decades, and it has been a significant tailwind for long/short strategies. Whether it continues into the second half is the setup question heading into earnings season.

Calendars

The US week runs Monday through Thursday, with Friday closed for the Independence Day holiday. The two events driving the narrative are Warsh’s Sintra panel on Wednesday and June NFP on Thursday morning. The USMCA also hits its required six-year formal joint review on Wednesday July 1, which is worth watching for any US-Canada-Mexico trade signal given ongoing tariff tensions.

Market Prep

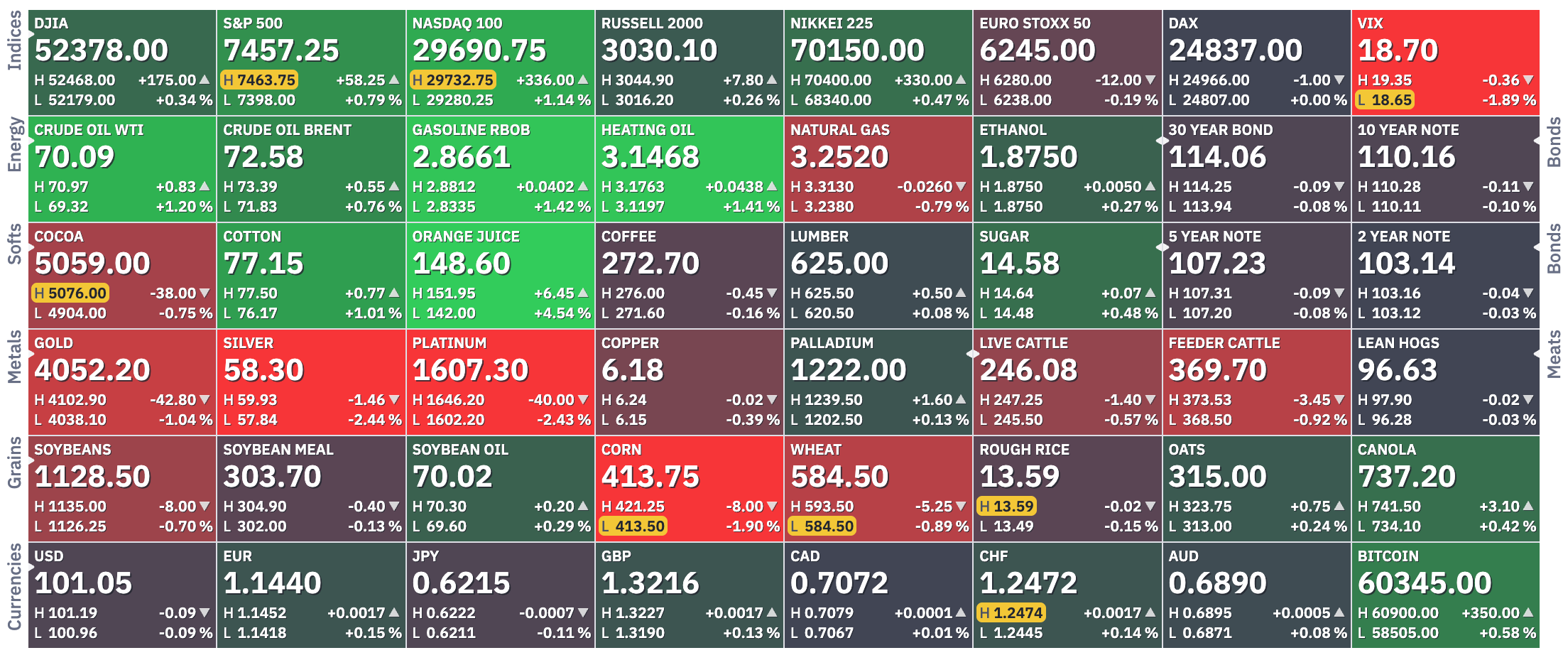

Last week was ugly at the index level but far more nuanced underneath. The S&P 500 fell 1.95% and the Nasdaq dropped 4.60%, with Nvidia down 8.6% and Alphabet down 8.3% leading the move. The Russell 2000 hit fresh record highs, up 1.02%. Healthcare gained 7.89%, Real Estate 3.95%, and Utilities 3.91%. The equal-weight S&P 500 outperformed the cap-weighted benchmark by more than 200 basis points. This was rotation, not a broad risk-off event.

US equity futures are +0.6% heading into Monday’s open on the Doha news.

The Nikkei opened higher but slipped to -1% by mid-session, weighed down by sharp tech dispersion.

Korea was the worst performer in Asia. The KOSPI fell as much as 2.6%, extending the nearly 8% loss from Friday. Mega-cap tech was the culprit. Samsung and SK Group formally announced a KRW 2,000 trillion ($1.29 trillion) 10-year investment plan in chips, AI, and infrastructure during the session. The fact that a $1.3 trillion commitment could not stabilize those stocks tells you everything about current sentiment toward the theme. The KOSDAQ, which excludes Hynix and Samsung, was up 7% on the same day.

Hang Seng outperformed, up 1.7%, with Alibaba rebounding and the Hang Seng Biotech Index posting its largest intraday gain since March 2022 amid growing interest in Chinese biotechs.

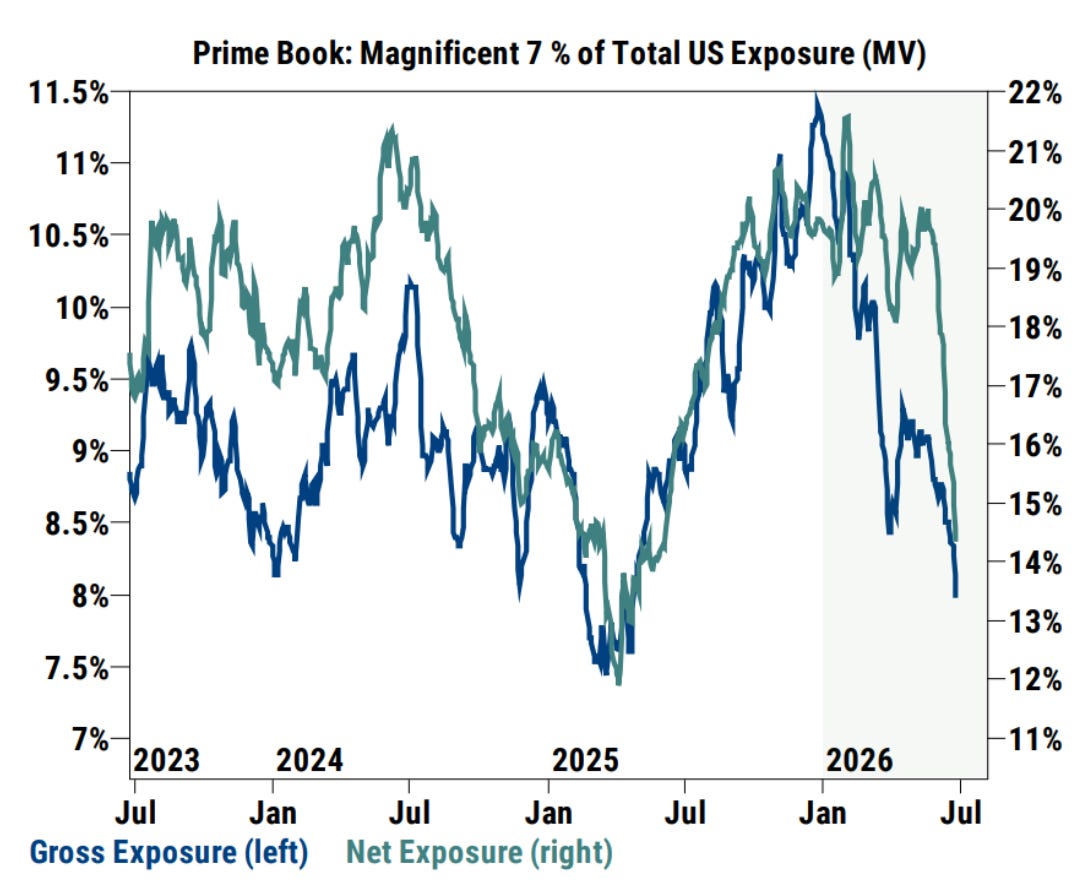

The positioning picture is one of deliberate risk reduction. Goldman Prime Brokerage data shows the prime book saw both gross and net leverage fall at the fastest pace since March, the second consecutive week of de-grossing. Mag 7 gross and net exposure are approaching three-year lows, sitting at roughly the 4th and 6th percentiles respectively. Semis saw eight consecutive sessions of net selling, with more than half of US tech outflows concentrated in semis and equipment. Global gross and net allocations to tech still sit at the 96th and 94th percentiles on a one-year basis, so this is a deliberate trim, not capitulation.

What makes the setup interesting is that the earnings backdrop remains strong. Q2 EPS consensus is at +22% year-over-year, the highest estimate going into an earnings season since 2021. Goldman’s Ben Snider notes that the entire S&P 500 gain over the last 12 months has been earnings-driven, with the forward P/E holding at 20x. Goldman expects AI infrastructure to contribute roughly 60% of Q2 EPS growth, with MU and NVDA alone accounting for more than 40%. The market is not questioning the fundamental story. It is questioning concentration and valuation at these positioning levels.

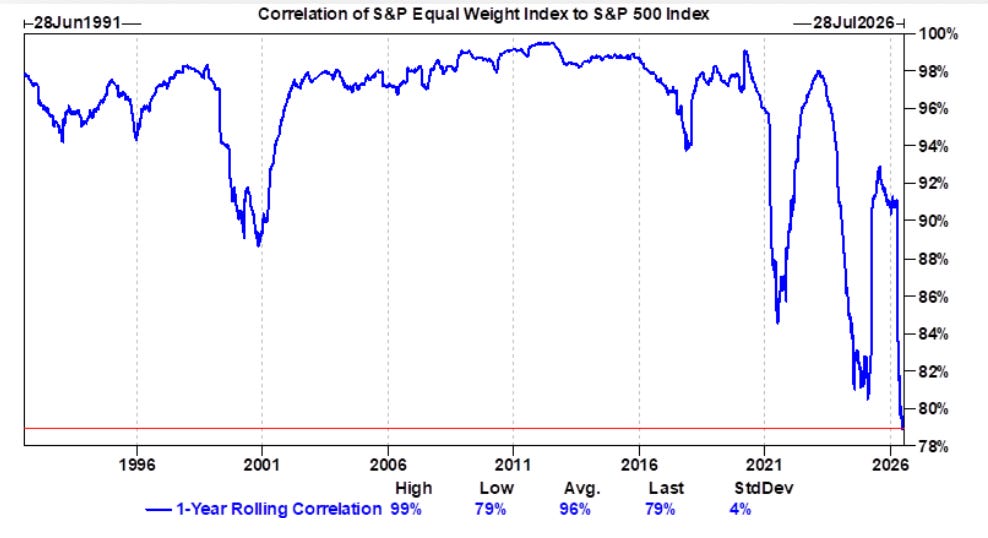

One signal I am watching closely: the 1-year rolling correlation between the S&P Equal Weight index and the S&P 500 has dropped to 79%, the lowest reading ever against a long-run average of 96%. US equities are trading less as a single index and more as a collection of individual businesses. That is a structurally different market, and it raises the value of stock selection significantly heading into earnings season.

Market structure adds a mechanical layer to all of this. US levered and inverse ETF AUM is now near $200 billion, with SOXL alone at roughly $30 billion. Daily rebalance flows buy strength and sell weakness, which amplifies moves in both directions even when the fundamental story is intact. 185 new US-listed ETFs launched in June alone, a record, per Goldman data.

Three things matter most this week. Whether Doha holds and how oil responds is the macro regime question for the second half — a genuine ceasefire reopens the SoH trade and shifts the energy disinflation thesis forward. Warsh on Wednesday is the Fed communication event of the month, and I am watching closely for any hint that his structural views carry a near-term read-through. Then Thursday’s NFP, where GS expects +130K and Wells Fargo +120K against a prior of 172K. A downside surprise eases hike pressure. An upside print brings the debate back to the table fast.