Breakfast Bites: Ceasefire Confusion

UAE gets attacked again; US Markets pull back with oil higher; Iran puts forth demands

Rise and shine everyone,

The war is back on. The US fought off Iranian attacks to give safe passage to two US-flagged vessels through the Strait of Hormuz. Meanwhile, the UAE defended four cruise missiles, but Fujairah port sustained a hit. Al Jazeera reports that Iran has denied claims of the attack against UAE, instead pointing the finger at the US. Sometimes I wonder if we’re really in the middle of a war, or some crazy soap opera.

Oil prices spikes yesterday, giving some of that back this morning. US Stocks all closed lower, alongside European stocks. The UK was closed for holiday. US Yields rose across the curve, as did the DXY. Markets are easing somewhat this morning with oil lower, Asian equities and US equity futures slightly higher.

I’m not convinced we’re seeing the end to an escalation here. For today, the focus is on US ISM Services PMI, US JOLTS and AMD earnings after the close.

Morning Macro Briefing

What we do know about the war is that the status of the ceasefire is unclear. Over the weekend, Iran submitted a 14-point revised proposal to the United States through Pakistani mediators. The proposal involved scrapping any notion of the existing temporary ceasefire, and rather pushed for a permanent end to the conflict under a strict timeline.

Iran has proposed a 30-day timeline to resolve issues about the naval blockade, Lebanon, and the status of the war within this timeframe. Further, a second phase of negotiations specifically regarding the nuclear program would only begin after the initial 30-day deal is sealed.

There’s more. US Treasury Secretary Scott Bessent asserts that the United States maintains “absolute control” over the strategic waterway, and called on international allies and specifically urged China to “step up” its diplomatic efforts to pressure Iran into reopening the passage to global shipping. The NYT reports that China has been prodding Iran to negotiate with the US, all the while still supplying materials that could potentially be used as military weapons. The meeting between Trump and Xi scheduled for May 14, should be an interesting one - with Xi potentially using the war as leverage for discussions.

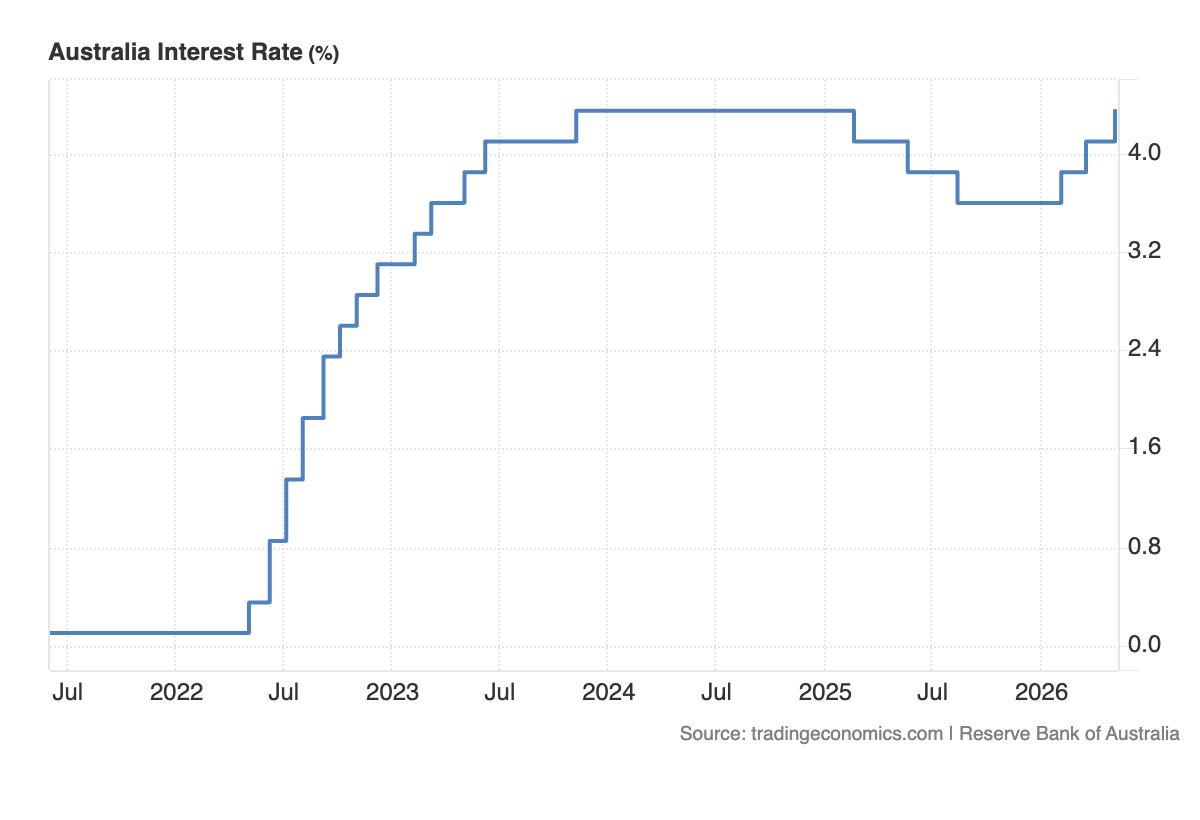

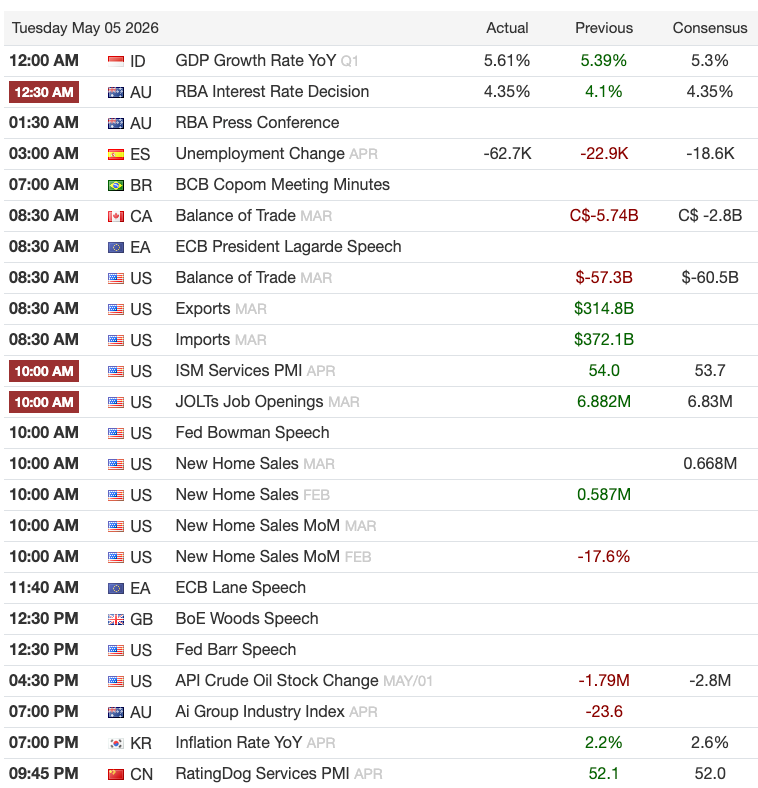

The Reserve Bank of Australia increased the cash rate to 4.35% to address persistent inflationary pressures. The rate has now reached the post-pandemic hiking peak. One thing to remember is that Australia started hiking before the war. This 25-bp hike reflects concerns over rising energy costs and significant domestic capacity constraints. Policymakers will remain data-dependent as they monitor how geopolitical tensions might further impact global commodity prices.

Chart of the Day

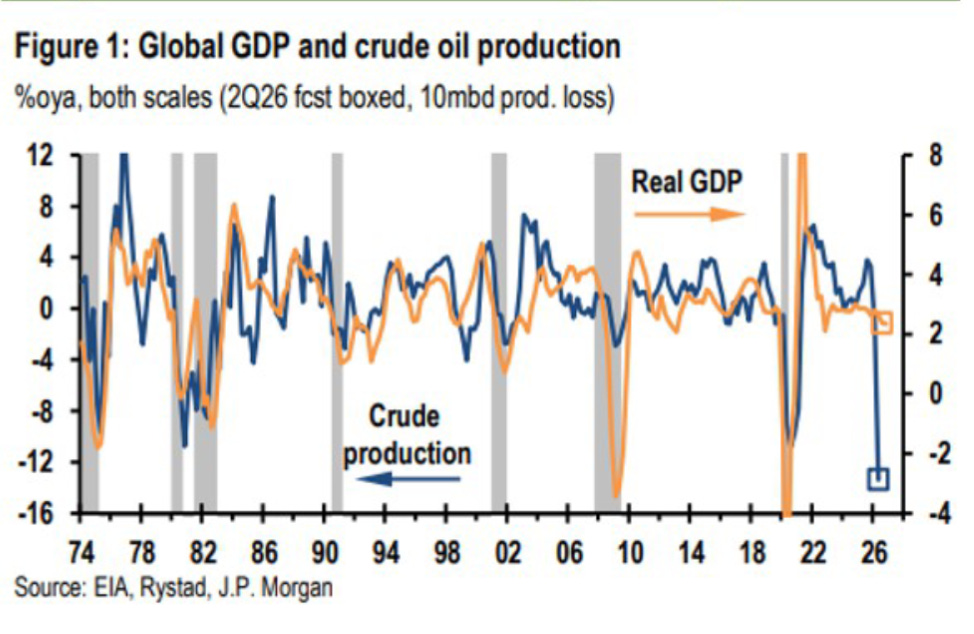

“Crude production run rate is down 12% y/y... but the GDP growth so far is resilient thanks to buoyant tech spend.” - JPM

This is actually good news; the world remains more resilient than expected.

Calendars

Market Prep

Monday’s session was softer than it looked. The S&P 500 fell 0.30%, the Dow dropped 0.86%, and small caps were the weakest of the major indices. The culprit was oil: renewed fighting in the Middle East sent Brent crude up over 5% to nearly $114, and Energy was the only sector that finished in the green.

Tech stocks moved in very different directions on the same day. Cloud and AI infrastructure names surged, with some up 6-12%, while chip stocks tied to traditional computing fell 2-4%. Memory and storage companies held up well, and Amazon and Microsoft closed higher, while Google and Apple gave back some of their recent gains.

Big investors were mostly in selling mode. Both hedge funds and long-only funds were net sellers on Monday, with activity levels on Goldman’s desk described as low. Goldman’s own measure of market skew sits at -4%, meaning the desk is leaning toward selling rather than buying.

JPM’s desk flagged a specific concern: their clients are worried about a potential 3-4% pullback in the S&P 500. The risk is that momentum-driven and systematic funds start unwinding their long positions at the same time. The usual hedges like bonds and gold haven’t been working well lately, so JPM is recommending VIX calls and index puts as protection.

One positive offset is that corporate buybacks are coming back online. Goldman estimates around 69% of S&P 500 companies exited their earnings blackout windows as of yesterday, rising to roughly 88% by the end of this week. That is a meaningful source of steady buying demand that was absent during earnings season.

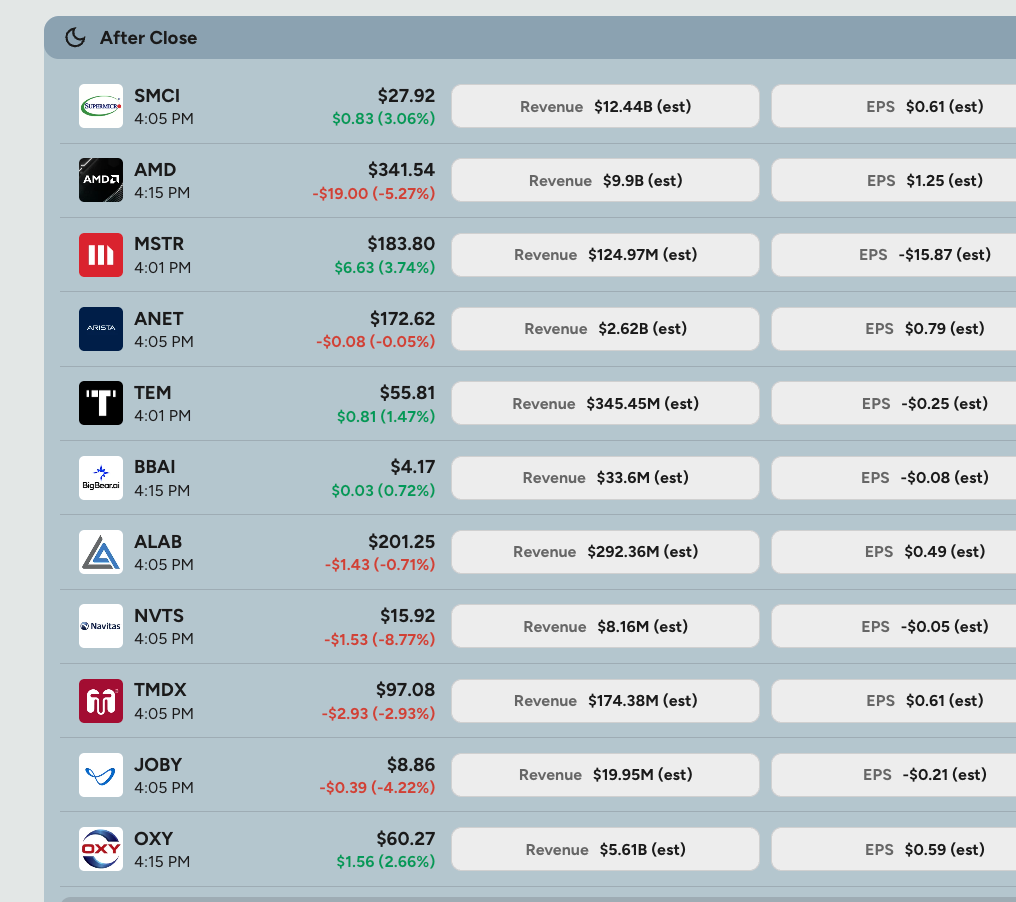

AMD reports after the close today, and the result matters for how the market thinks about the chip sector over the near term. The stock fell 2-4% yesterday even while other tech names rallied, which tells you expectations are cautious. A strong print will need to show clean revenue growth, healthy margins, and an encouraging outlook on AI chip demand to move the stock meaningfully higher.

Palantir reported Monday evening and beat estimates comfortably, with revenue of $1.63 billion against an expectation of $1.54 billion and earnings well ahead of forecasts. Despite that, the stock is only down about 2.8% in premarket, which is actually a calm reaction by Palantir’s historically volatile standards. The three things to watch today are oil prices and whether geopolitical tension escalates further, whether large institutional buyers start returning to the market after sitting out the recent rally, and AMD’s earnings after the close.

My Take

We’re back in unpredictable territory for the Middle East war. While Iran has put forth a 30-day timeline for demands, it doesn’t really conform to what the US wanted, which is to discuss the nuclear program now. It’s tough to say whether the US concedes on this issue, but most likely not.

Meanwhile, missiles are flying again, with the US and Israel allegedly threatening to retaliate after Iran attacked the UAE. It’s a mess. People are guessing that the UAE may enter the war, now that they have left OPEC. Again, no one knows, and the UAE is quite good at playing it close to the vest.

The three things to watch today are the trajectory of oil given ongoing Middle East uncertainty and what it does to yields and energy sector flows, whether the LO demand vacuum persists or whether any re-engagement emerges into the strength of the recent rally, and AMD’s print after the close on both the AI GPU revenue line and the data center guidance.