Breakfast Bites: Buybacks and Yield Stories

US Treasury doing buybacks; Yields are spiking in Japan and China; Flows are still now high conviction

Rise and shine everyone

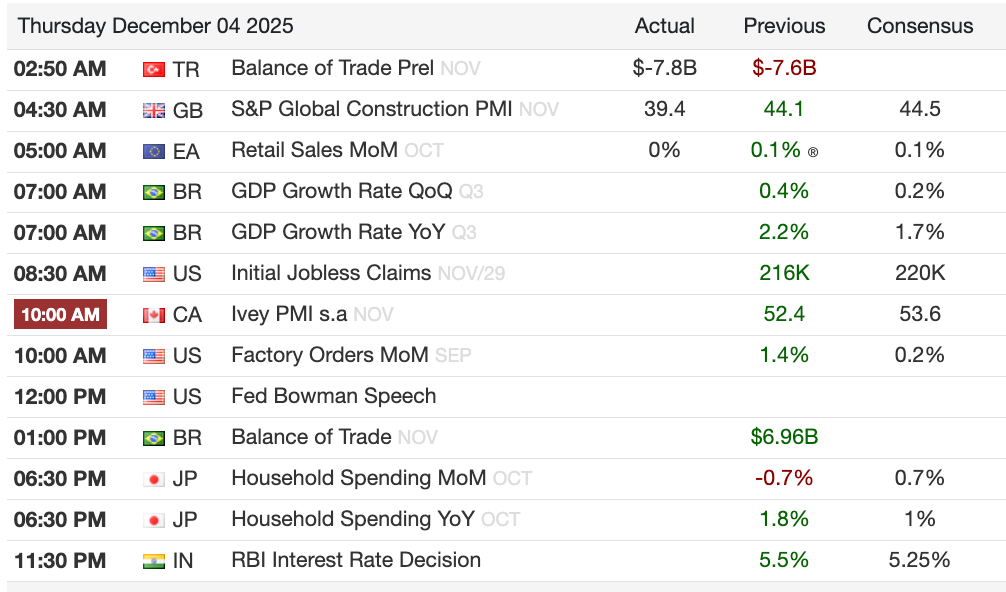

A few interesting things in the Macro Briefing section today. Tomorrow will be the macro-heavy day with US PCE and Sentiment data releases.

Morning Macro Briefing

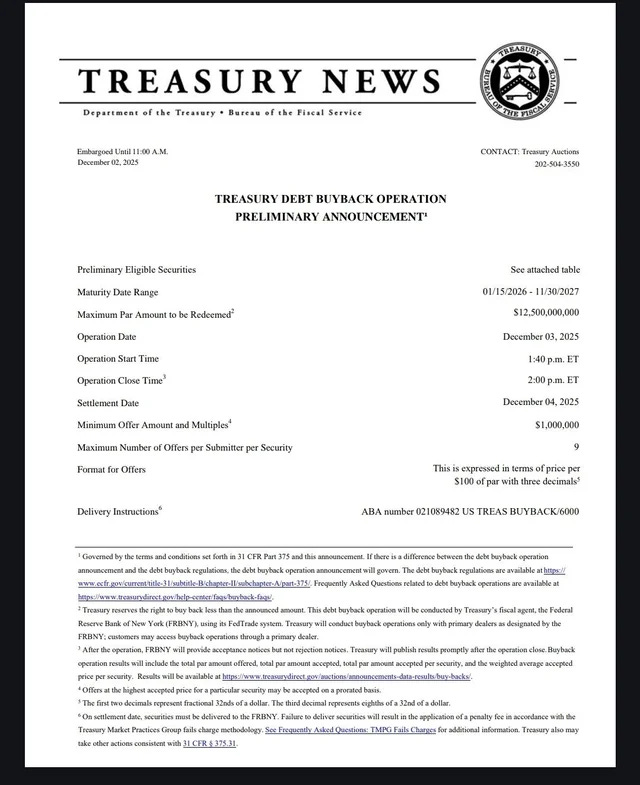

Let’s talk about the Treasury Buyback announcement. Mayhem posted this on Twitter:

So the amount is $12.5B. The amount is large but not enormous. Usually, these buybacks target off-the-run, less liquid securities. Put another way, this helps to unlock liquidity for the treasury market, which in turn introduces liquidity to the broader market.

Now sometimes, the US Treasury will do buybacks for cash management. According the FAQs: “Cash management buybacks are intended to reduce volatility in Treasury’s cash balance and Treasury bill issuance, minimize bill supply disruptions, and/or reduce borrowing costs over time.” In other words, this is to meet day to day expenses.

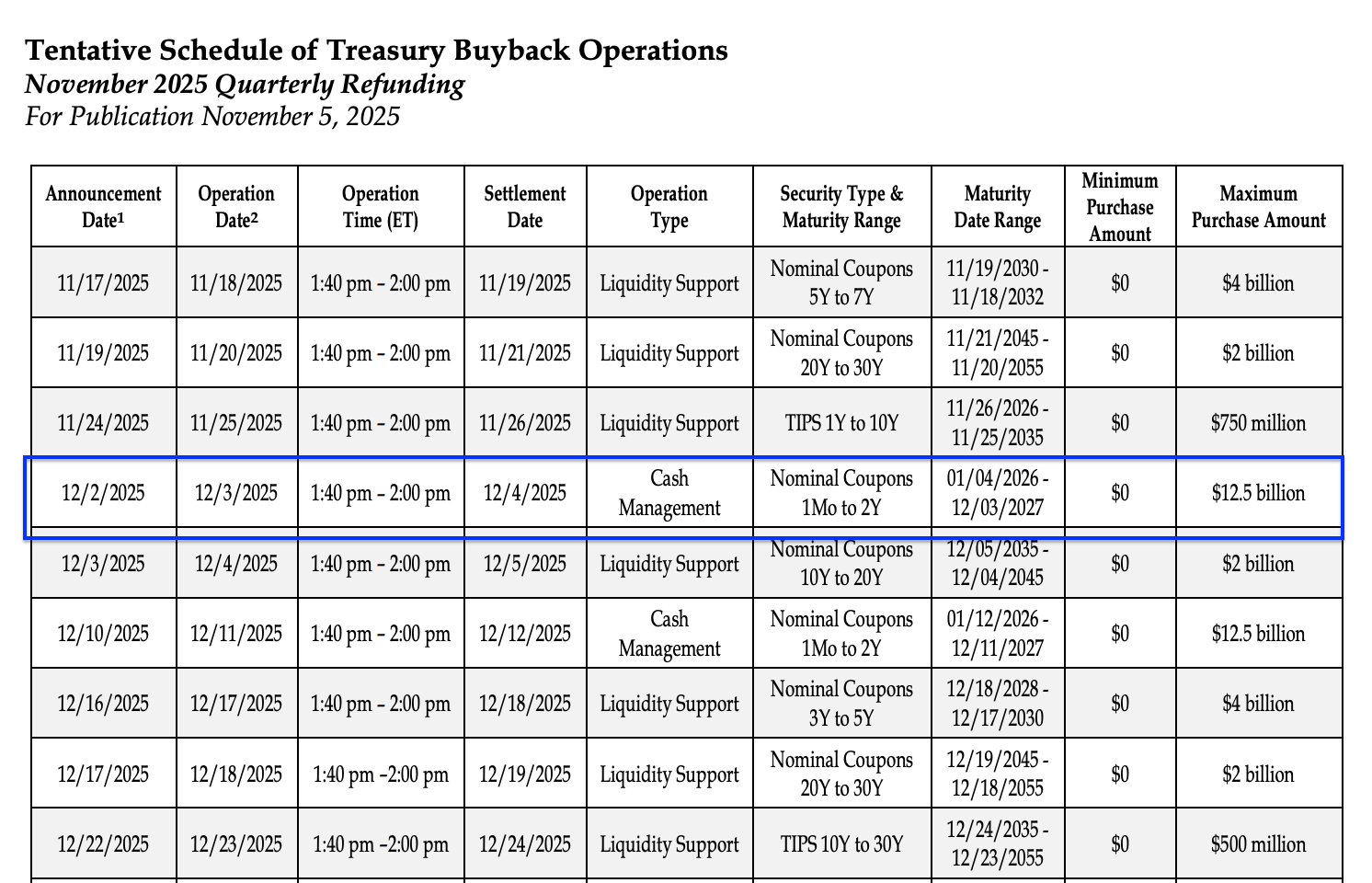

If we look at the chart below from the US Treasury, this is termed a Cash Management Buyback, and it’s sizable compared to the others.

This is just a theory, but we are still waiting for the tariff ruling from the US Supreme Court. In the meantime, about $200 billion in tariffs have been collected. Some of that may have to be refunded, and it’s possible that these funds go towards that.

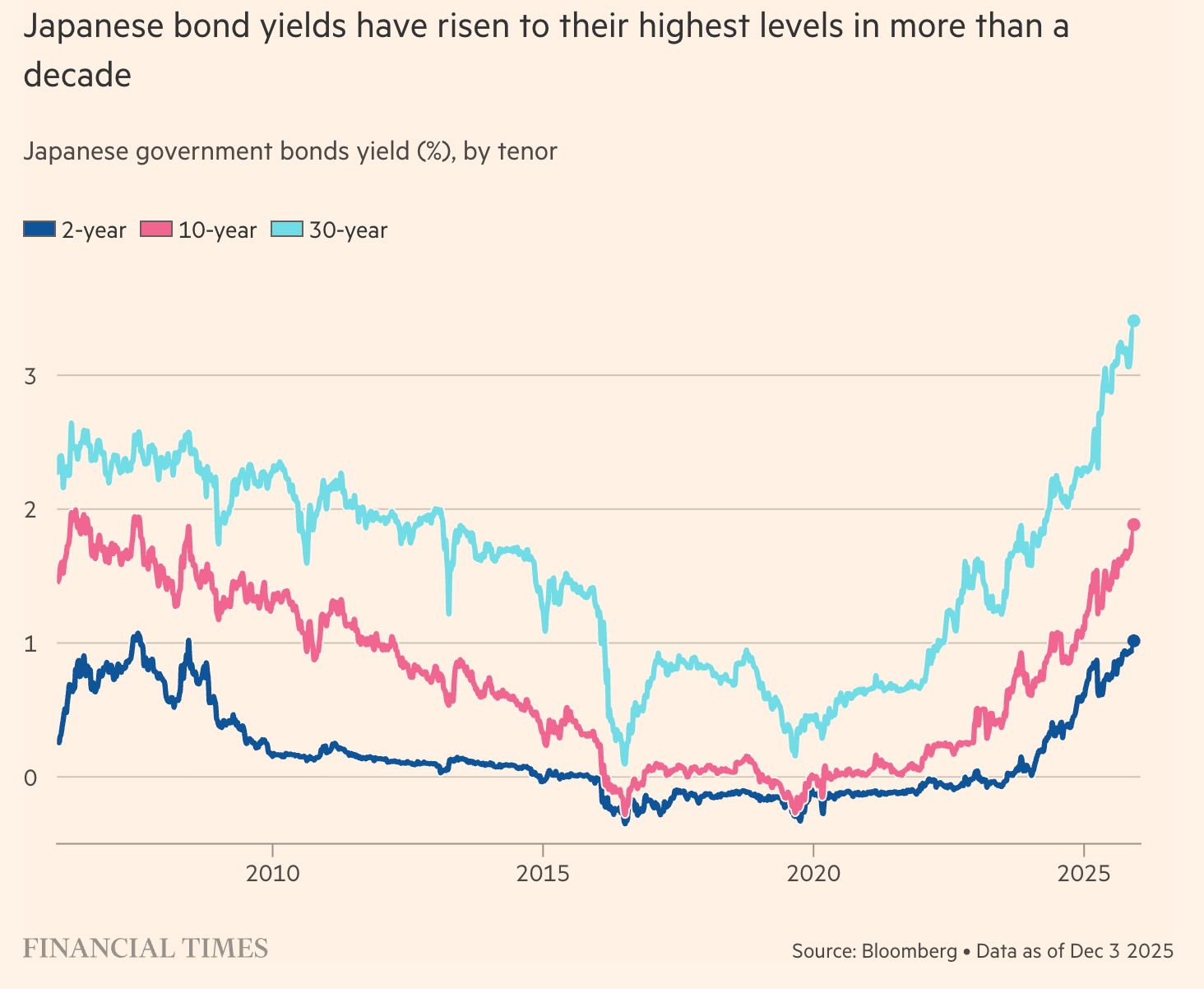

Everyone’s also talking about the Japanese Government Bond (JGB) Yields. This is not new for us… we talked about it on Tuesday already, and I said this is something we will be watching. What I’ve learned since though - the last week of November showed foreign buying of JGBs of up to JPY 1 trillion for the week. That’s substantial!

Bid-to-cover on the latest 30Y auction was the strongest since 2019 and the auction had the narrowest tail since Feb. Investor demand is increasing. Again, what does this mean for market? It means there is a rotation of capital allocation. Some of that would’ve left the US market, and some the global markets. This could very well be one possible reason that liquidity remains relatively low in the US markets.

Chinese Government Bond yields are also inching up. We talked about Vanke and the stress in the property market becoming an issue again. That backdrop is colliding with the more “prudent” tone from the PBoC, which briefly supported the yuan before renewed concerns around funding stress in property quickly pulled it weaker again.

There’s not much in terms of macro today. But tomorrow we have the PCE and UoM Sentiment data for the US.

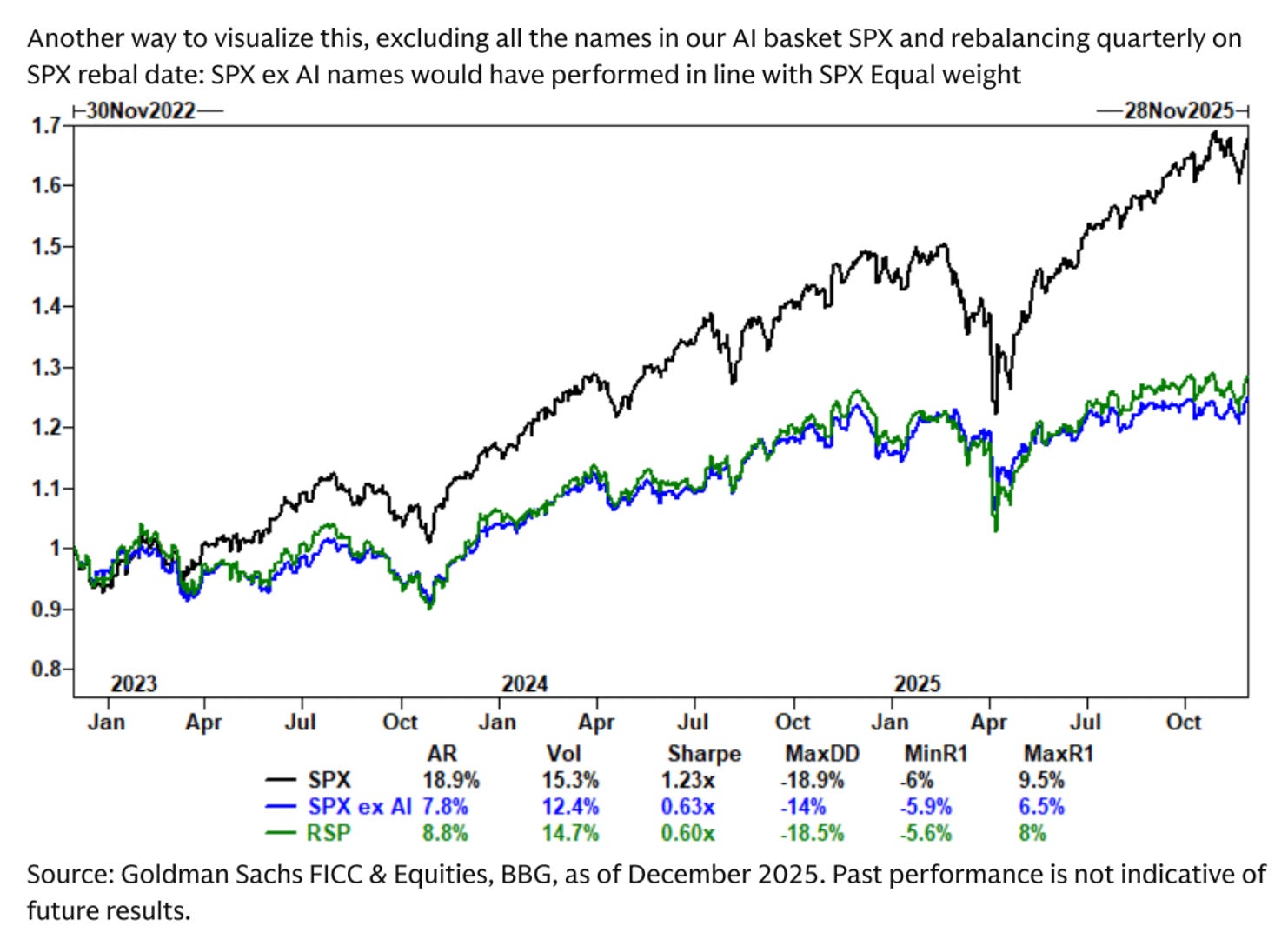

Chart of the Day: GS asks Where would the market be if ChatGPT wasn’t invented?

Brilliant chart from GS. They have a basket of AI stocks. So they ran a simulation to see what the market would look like without this basket of AI stocks. The chart below shows the SPX, and SPX-AI.

Calendars

Market Prep

Flows remain the core driver coming into the session, with yesterday’s move still looking more like positioning balancing than renewed conviction.

The US yield curve flattened ever so slightly, because the short end likely saw some pressure as front-end yields held firmer helped by buyback announcement we talked about under the macro section.

Bitcoin holding above 90K continues to underpin broader risk appetite, even as volumes remain uneven across cash equities.

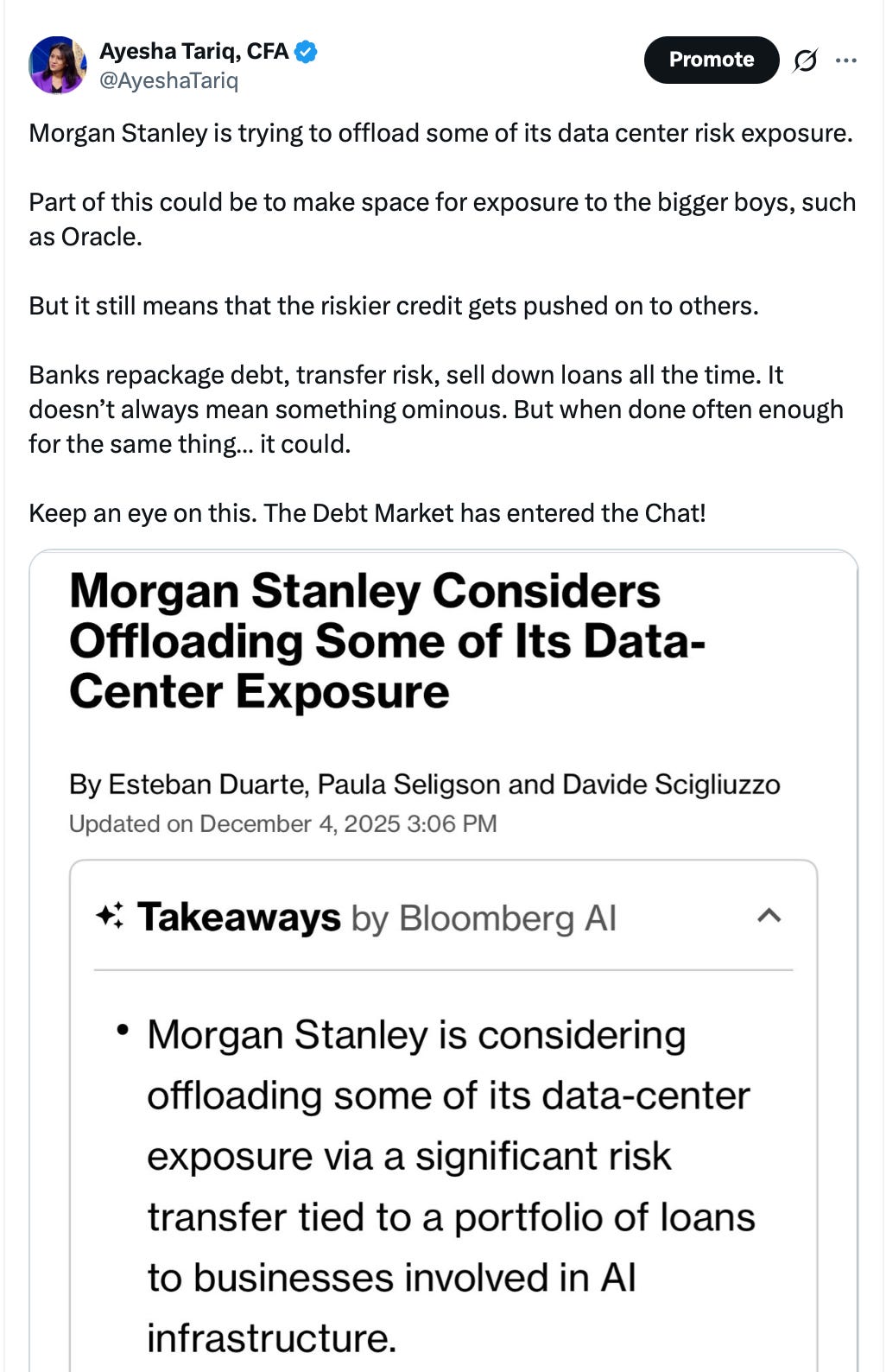

Sector tone is still led by tech and AI, but with clear dispersion. Software and semis are trading tightly around earnings and guidance, while the broader AI complex is struggling to extend gains without fresh catalysts. Yesterday, Bloomberg posted an article about MS transferring some of their data center risk:

Here are my thoughts on that.

Energy is stuck between geopolitics and the 2025 oversupply narrative, keeping rallies capped. Oil is firmer on renewed attacks on Russian energy infrastructure and stalled Ukraine peace efforts, but longer-term supply concerns continue to limit upside.

From the European open, the tone is cautiously constructive rather than outright risk-on. Equities are modestly higher with defense, renewables, and semis outperforming, while exporters benefit from a softer dollar.

My Take

What matters into the open is the US data and the rates response. Jobless claims and PCE will decide whether the front-end remains anchored by buybacks and Fed expectations, or if the curve re-steepens on a data surprise.

Gold’s reaction will be an important read on how much easing is already priced. Bitcoin above 90K remains the key sentiment anchor for high beta, while traders watch if yesterday’s short squeeze has any follow-through or if breadth finally improves.