Breakfast Bites: Bouncing Off the Lows

Futures claw back after Thursday's brutal selloff as Russian crude sanctions ease, but stagflation risk is far from priced out and headlines still drive price action

Rise and shine everyone

It’s Friday, and we’re almost two weeks into the Middle East war. There’s no sign of de-escalation.

President Trump described the war as going “well” and threatened further action against Iran. Iran’s new leadership, under Mojtaba Khamenei, vowed to continue blocking Hormuz and targeting US bases & forces until attacks cease.

Oil prices are still as volatile, and have now moved up the trading band. Brent hovers around the $100/bbl mark, while WTI crude hovers around $94/bbl. The volatility continues to drive volatility in equities, not just in the US but across the globe.

Morning Macro Briefing

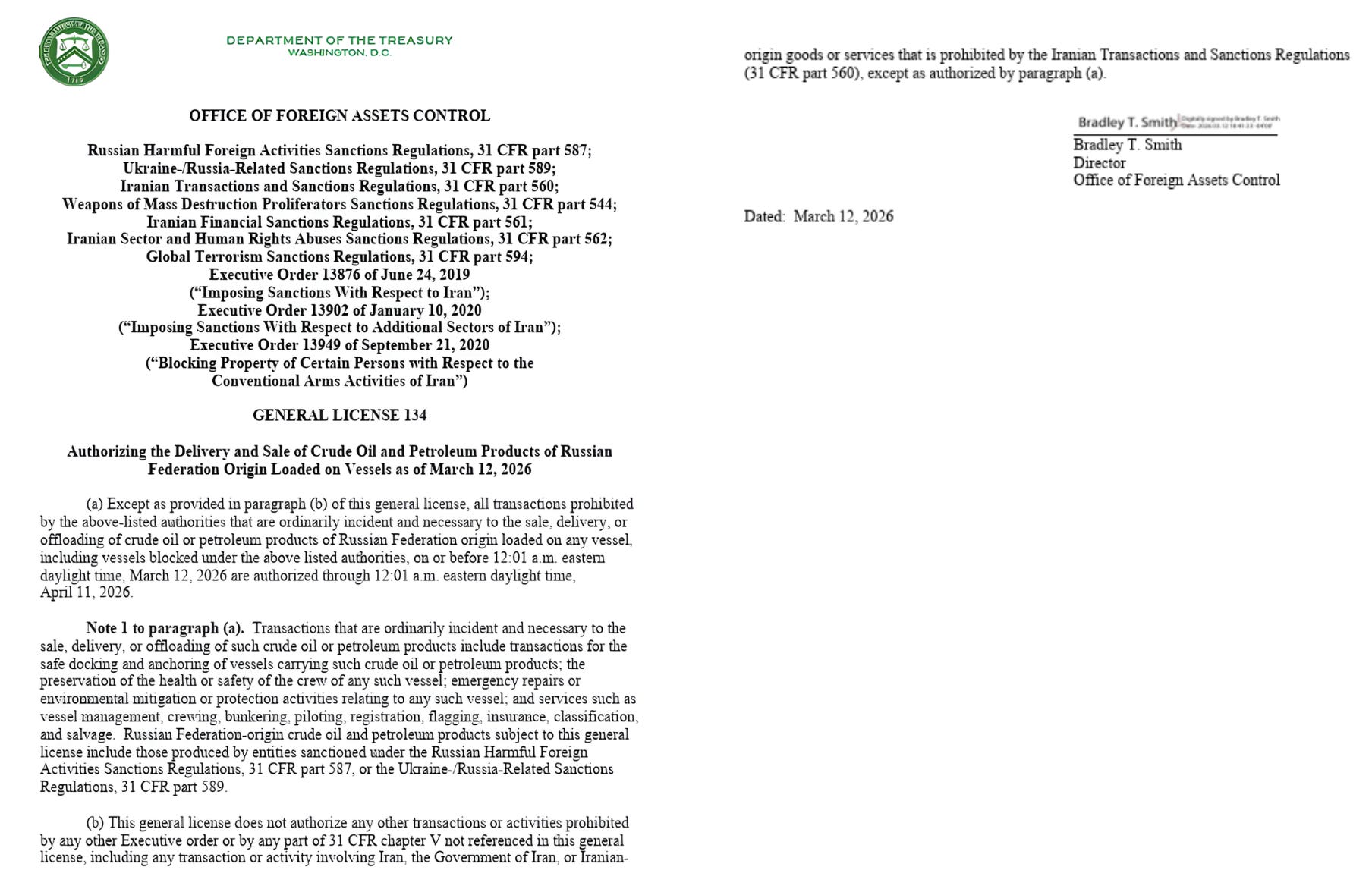

The major overnight news is the US easing sanctions on Russian crude, easing some pressure on oil prices. (Announcement below)

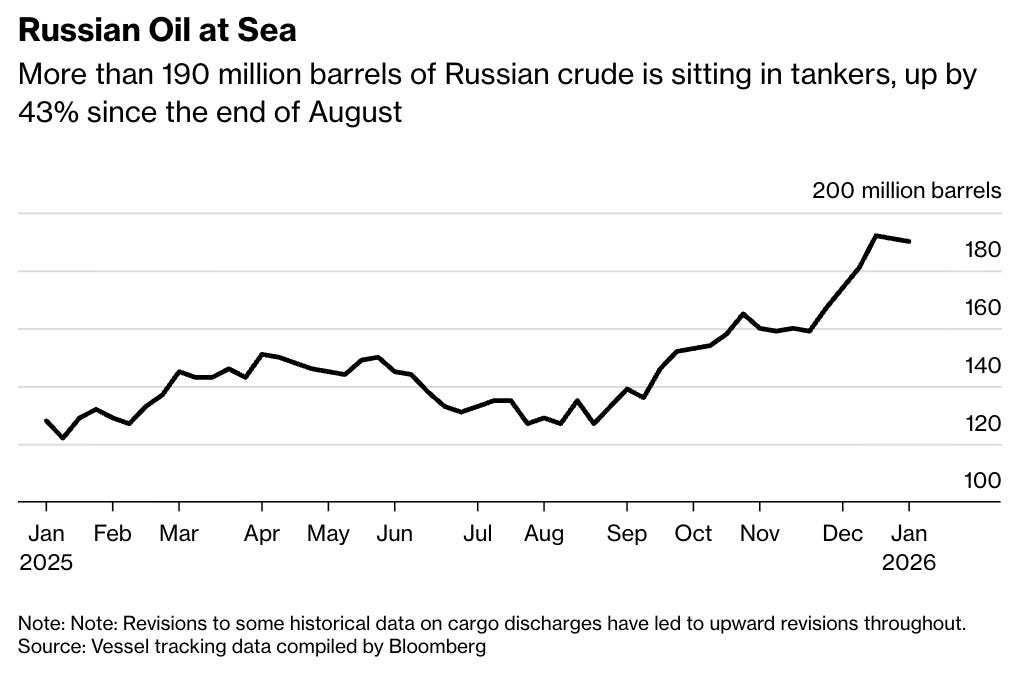

We’ve had data for a while that there’s plenty of Russian crude floating on water - 190+ million barrels, as of the end of January. This makes it easier for those to be delivered to distressed buyers, at a much higher price than previously anticipated.

However, one thing to note is that much of Russian crude, the Urals, tends to be heavier. Therefore, not all refineries have the capabilities to process this crude. This is particularly true of many developing countries, which have outdated refineries.

Meanwhile, India is turning to biomass, kerosene and fuel oil, all polluting fuels, to cover current gas shortages. The country has also reportedly asked China for urea for fertilizer, as the planting season gets started.

In other news, USTR Greer is joining Treasury Secretary Bessent in Paris this weekend for high-level trade talks with China’s Vice Premier He Lifeng.

Secretary of State Rubio plans to join the upcoming presidential trip to China despite being sanctioned by Beijing since 2020. This diplomatic push coincides with a potential olive branch as the Trump administration opts against new duties on Chinese battery materials.

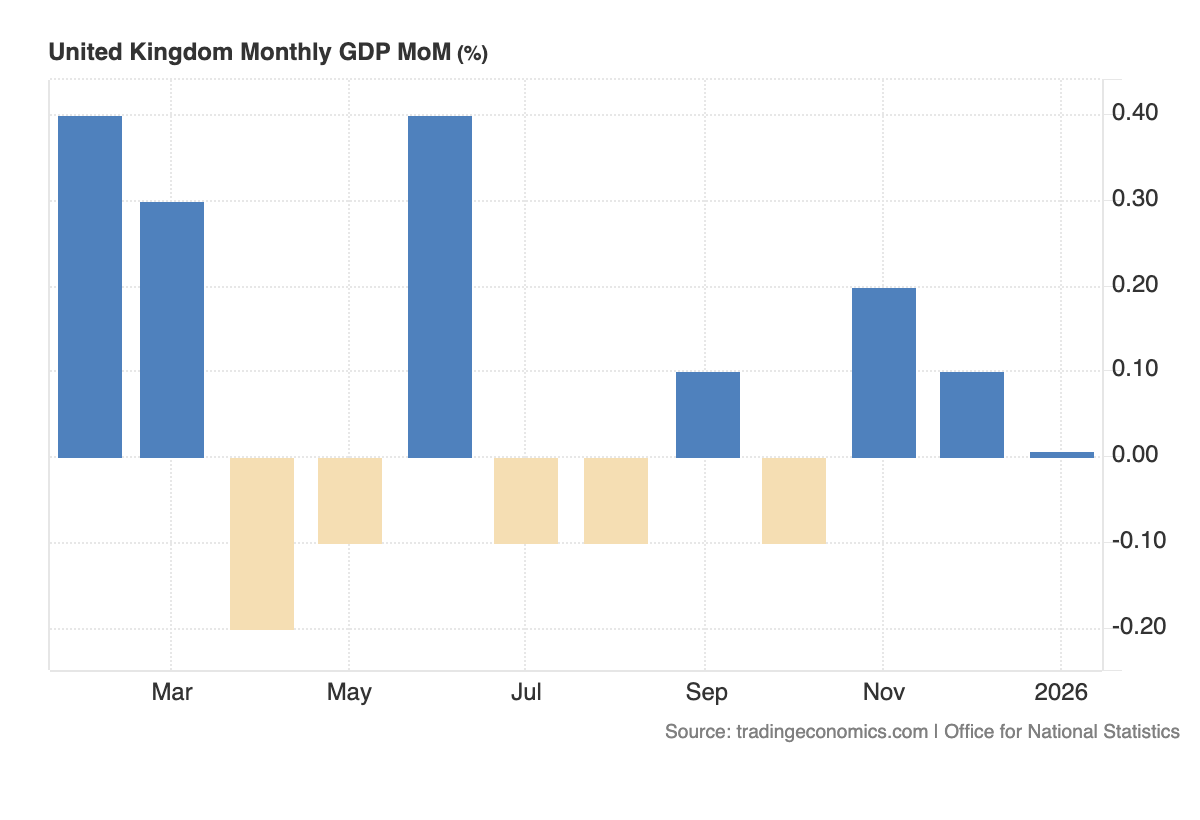

UK economic growth stalled in January 2026 after missing the projected 0.2% gain. A slump in administrative and production sectors offset modest improvements in retail and construction. Despite this monthly stagnation, the economy expanded 0.2% over the last three months. This brings the yearly growth rate to a total of 0.8%.

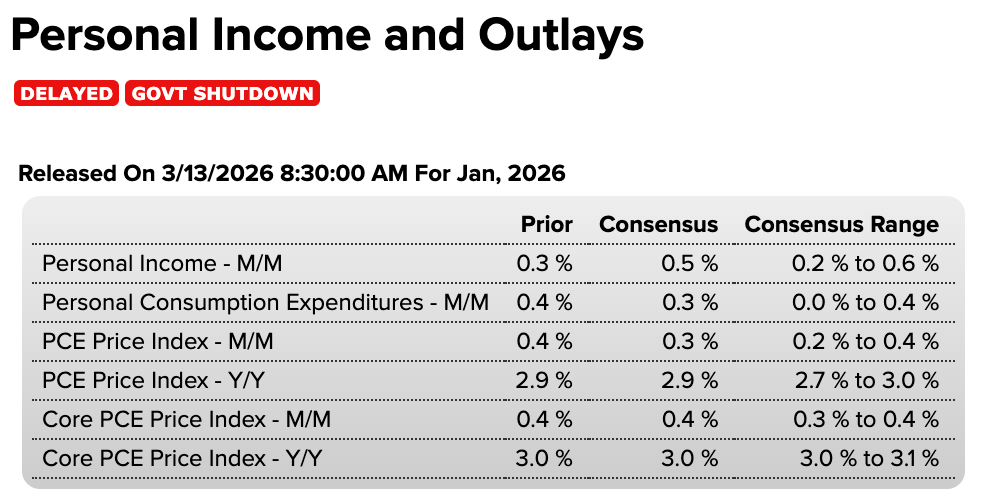

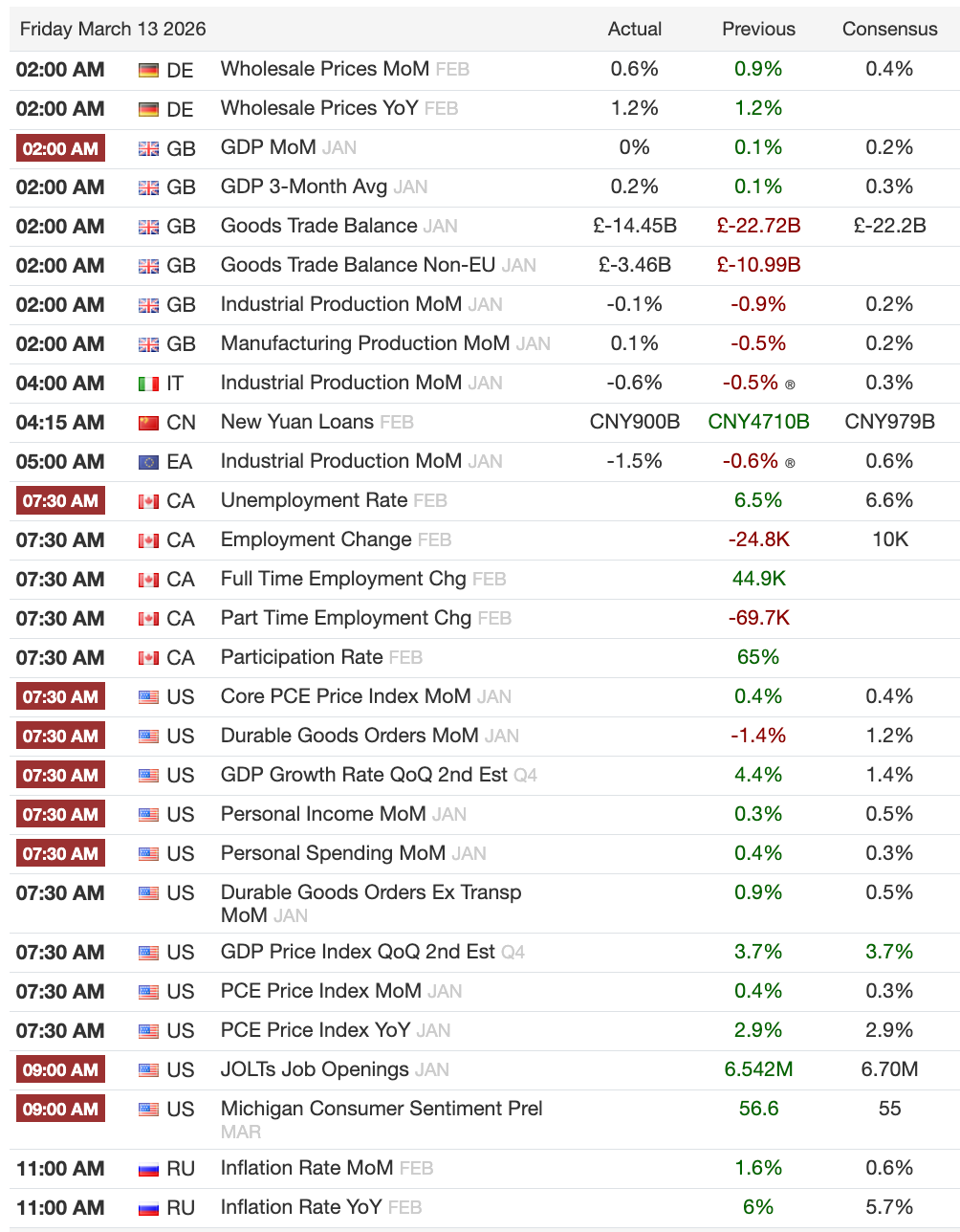

Finally, today’s focus will be on US PCE and UoM Preliminary Sentiment data. As with the CPI though, we’re not likely to see it move the needle as much since the conflict data will not play a part, and geopolitical headlines still dominate the narrative.

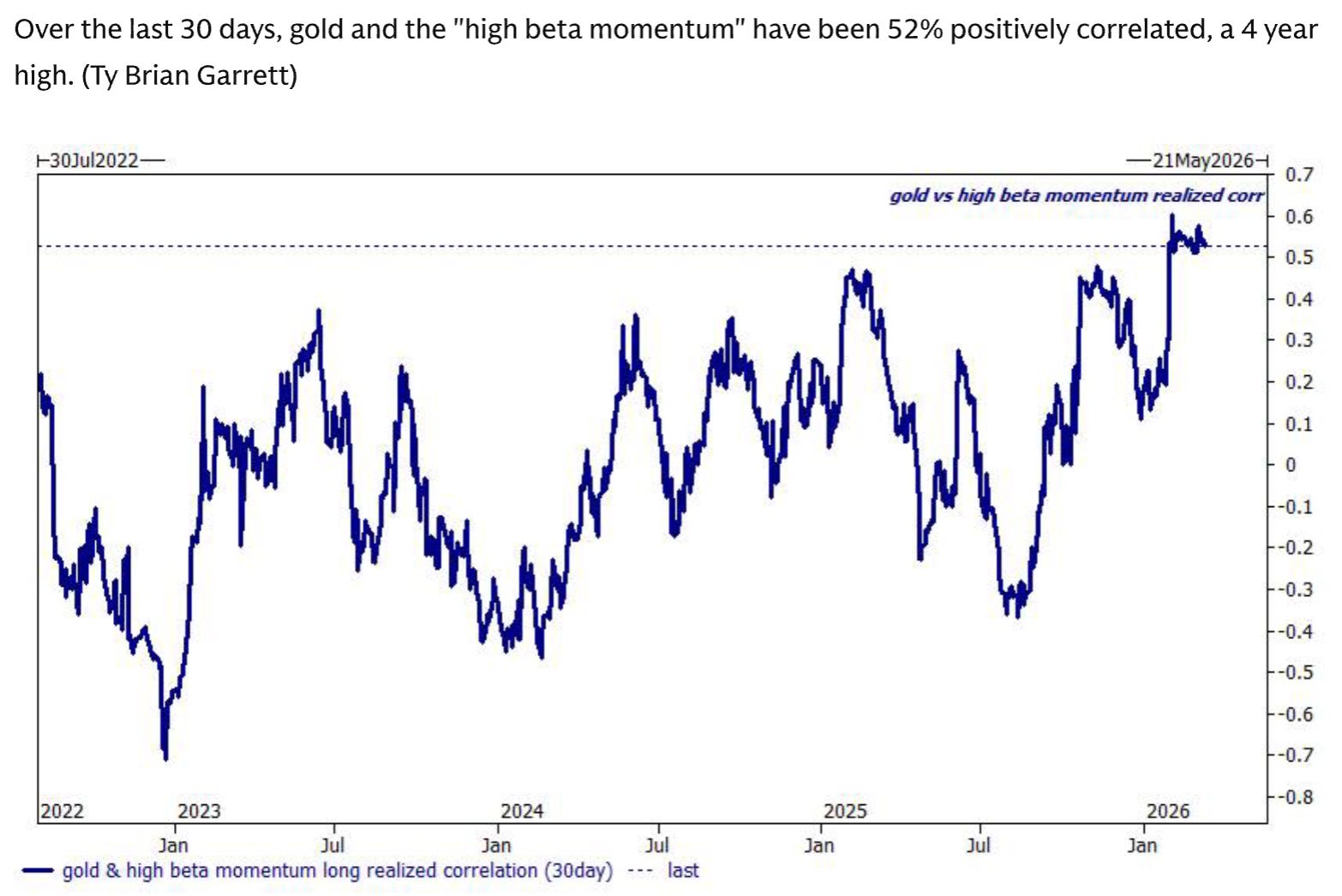

Chart of the Day

Gold and high beta momentum are showing a 52% correlation. So moves in gold could give us a good indicator of risk on assets, surprisingly!

Calendars

No earnings of note.

Market Prep

US Equities sold off overnight but are are now recovering ground in pre-market trading.

Risk assets saw a modest recovery during the Asian session as slightly lower oil prices supported a bounce in crypto and US equity futures. Despite verbal intervention from Japan regarding close coordination with US Treasury officials, the yen remained under heavy pressure. The currency hit its lowest level since July 2024 as it approached the 159.50 mark.

European equity markets dropped 1% on Friday as geopolitical tensions and rising energy costs kept investors on edge. While consumer and financial stocks faced heavy selling pressure, defense and energy firms managed to post modest gains. Strong corporate earnings provided a bright spot for some individual stocks, though the broader benchmarks ended the week largely flat.

Markets are recalibrating for a hawkish week as expectations for US rate cuts continue to diminish. Investors now see a 46% chance that the Fed stays on hold through the end of the year. In Europe, the outlook has shifted dramatically toward potential rate hikes starting as early as July.

Bernstein analysts report that the semiconductor industry is currently safe from Middle East-related helium shortages despite Qatar supplying 36% of the world’s output. While helium is an essential chipmaking ingredient with no substitute, major players like TSMC and SK Hynix have buffered the risk with solid inventories. The supply chain might be tight, but the industry is not holding its breath just yet.

My Take

There’s not much to consider other headlines for this market. We have seen some rotations under the surface, as we discussed yesterday but the situation continues to remain largely volatile.

Yesterday’s close was brutal - all broad market indices posted their lowest close of 2026. Energy stocks including Chevron and Exxon were among the few green spots Thursday, while banks and tech led the losses. Cruise operators Royal Caribbean and Carnival each shed around 5-6% as oil hit $100. Cybersecurity names like CrowdStrike, Palo Alto, and Fortinet are attracting attention given the escalating threat of pro-Iranian cyberattacks on US companies.

With efforts on multiple fronts to bring back energy supply to the market, we may see oil prices stabilize for a while, thereby bringing some relief to markets.