Breakfast Bites: Beware the Ides of March

The possibility of a prolonged conflict is weighing on markets but there's more to it than just that

Rise and shine everyone

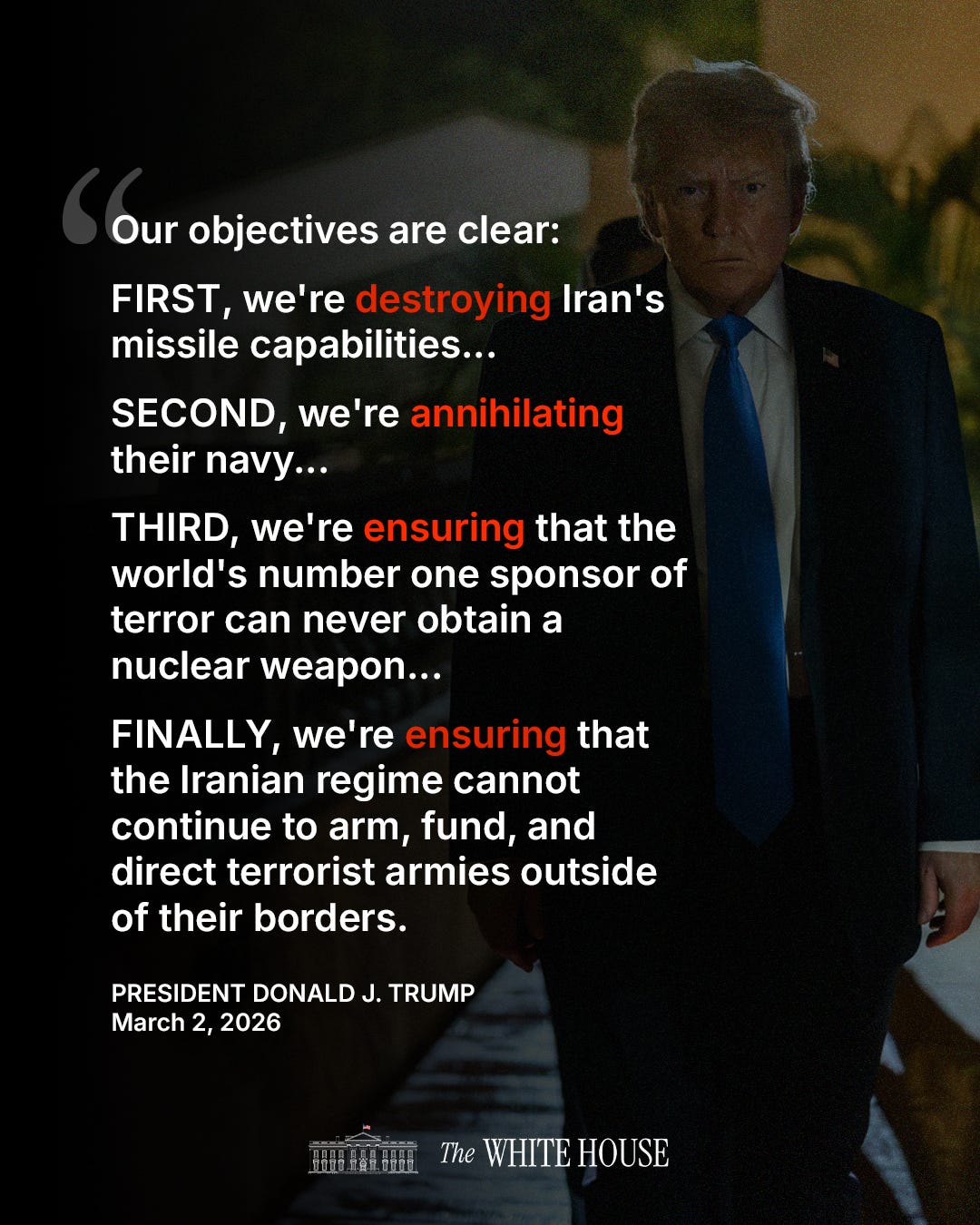

US Equity Futures are under considerable pressure this morning. It would seem that there’s been overnight selling, after President Trump delivered his speech and the White House released their 4-point agenda below.

The President talked about the war lasting 4 weeks but also mentioned that the plans were well ahead of schedule. The issue is that the focus of the war has now shifted, from just toppling the prevailing regime to a wider agenda. This would naturally create some fear.

We’re also seeing a spike in Brent Crude this morning, after attacks continue on the Gulf countries, some hitting energy assets as well (direct or falling debris). Iran has also threatened to attack ships passing through the Strait of Hormuz (with some unconfirmed hits already).

The idea of “stagflation” is starting to become a little more realistic, as various scenarios are being priced in to what may be a more prolonged conflict.

But, that’s not all that’s weighing on US equities. Seasonality is not on the market’s side, and we cover more details under Market Prep below.

Morning Macro Briefing

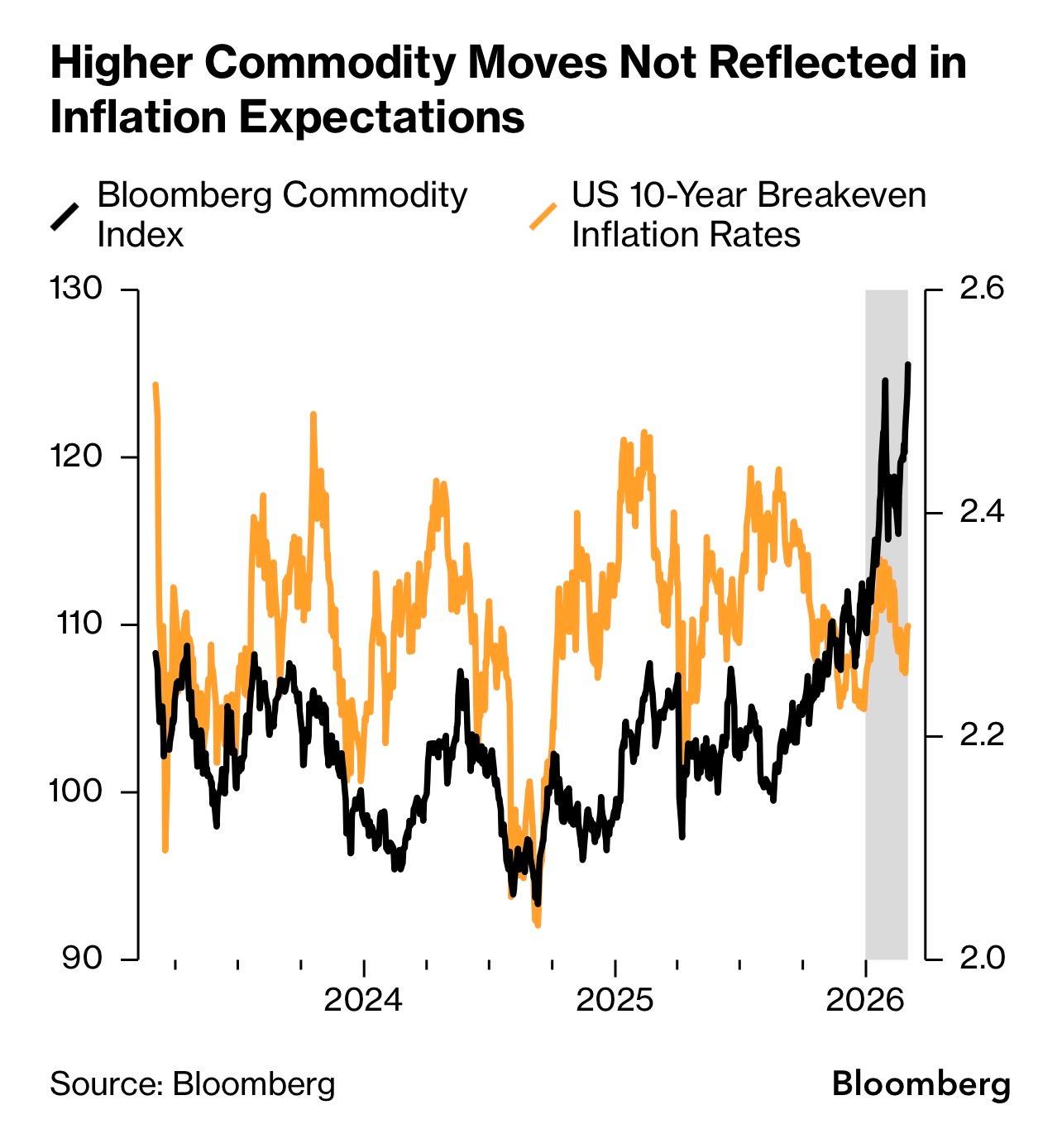

We’re seeing interesting macro moves. US Treasury Yields moved higher yesterday and continue to see upward pressure today. Some of that is the stagflationary scenario being priced in as we see the 2Y move more than the 10Y (see below).

However, I think it’s too early to talk about rate hikes. Looking at inflation expectations, we see that the moves are still not fully priced in, as we see below.

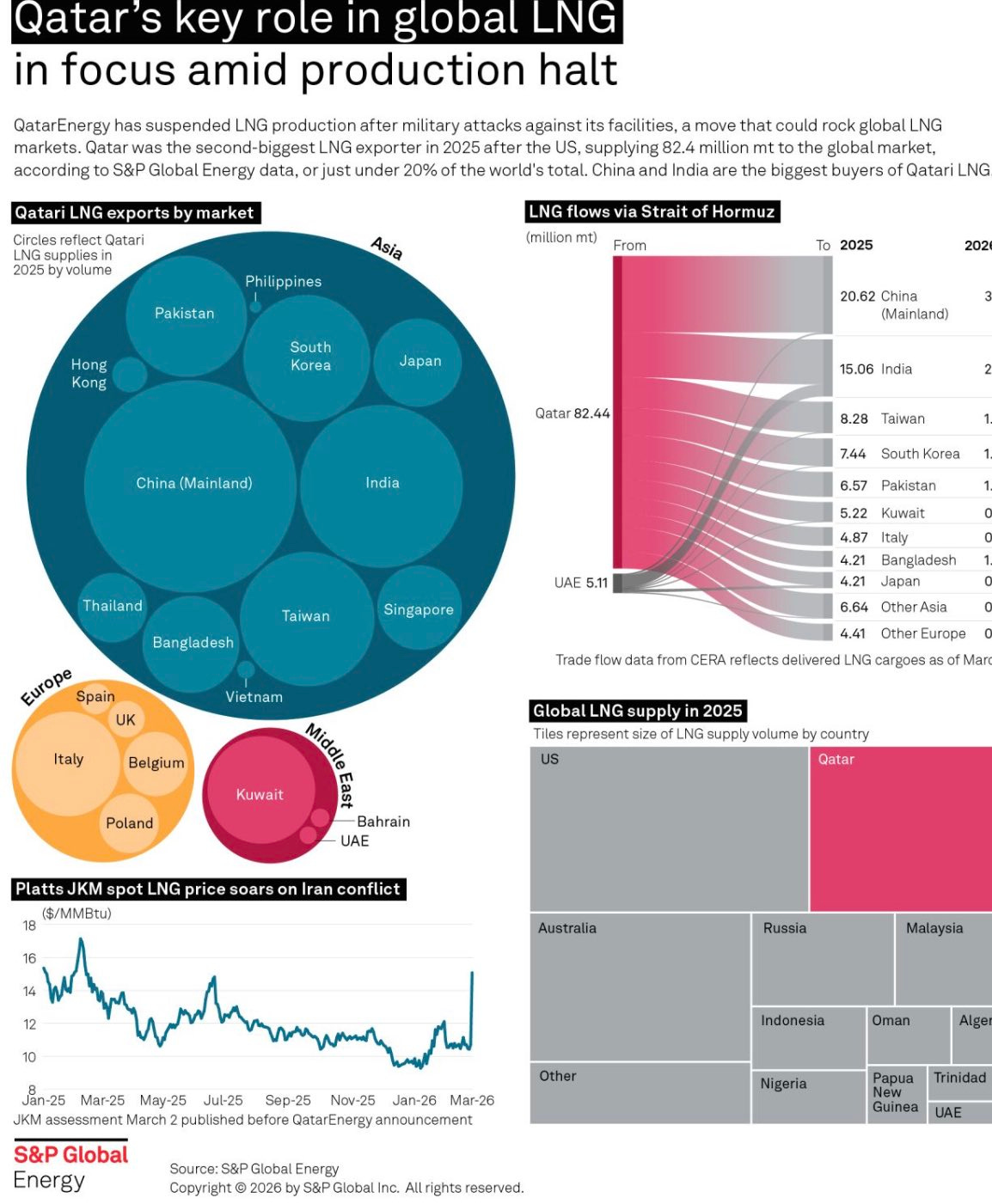

But, as this war drags on, we’re likely to start seeing more pressure in global commodities markets, pushing up prices across the global.

Energy, of course, remains the first hit, and after yesterday, we’re seeing that Gas prices are also soaring. European gas stocks are low, and that’s why we saw that massive spike in European gas prices yesterday. Today, I hear that Korean gas stocks are also running low (I have not confirmed this). But it stands to reason that Gas (LNG) is a bigger threat.

There are stockpiles of Crude Oil, but LNG stocking is limited in most countries.

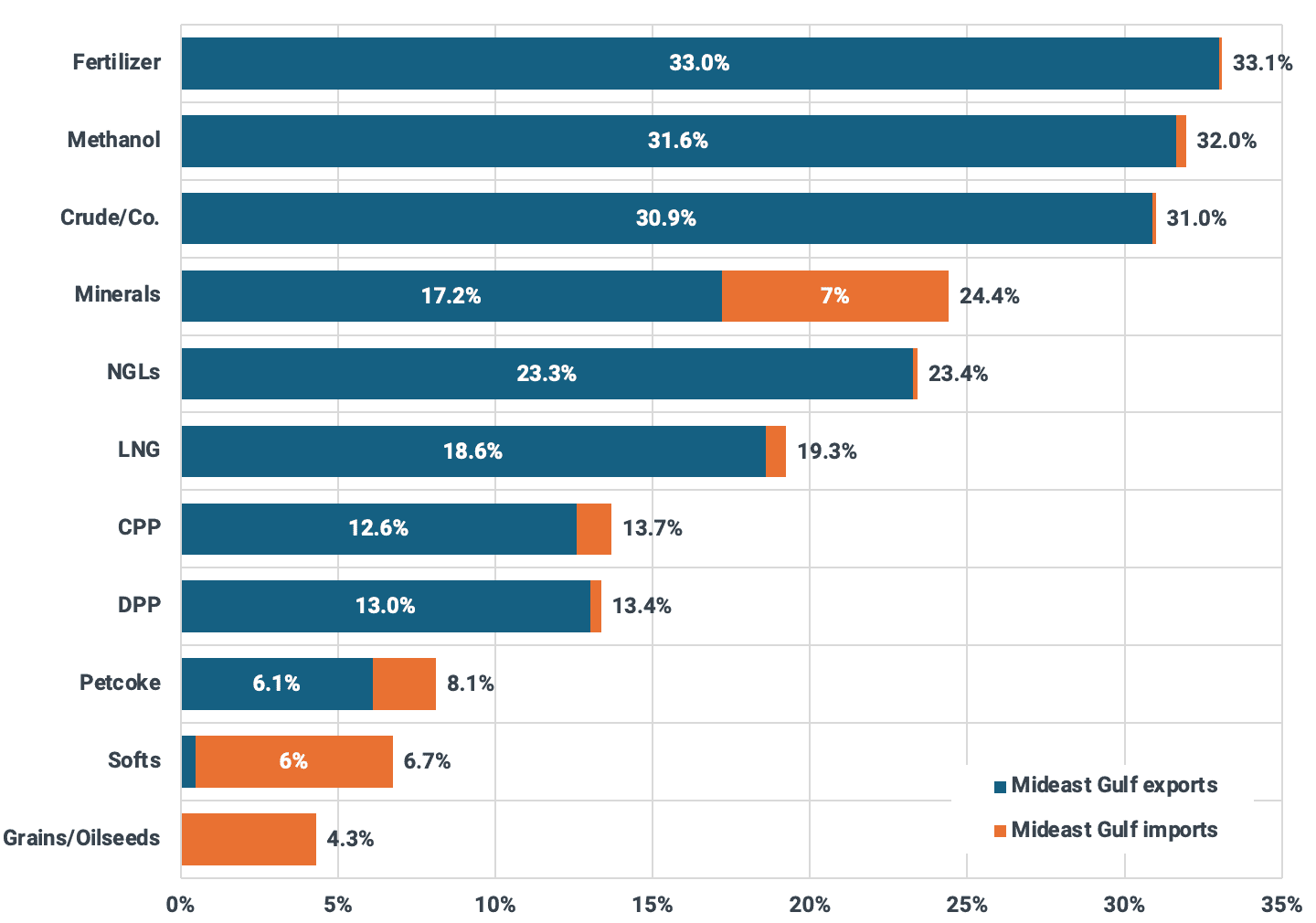

We also have other commodities that could see second-order effects. Yesterday, our chart of the day was from Kpler, and it showed that 33% of the world’s fertilizer passes through this Strait. There is speculation now that a shortage of fertilizer could hamper the crop planting season, and consequently, global food prices. This effect could actually go on for a while.

None of the news is good, and the longer this war goes on, the more dire and far-reaching the effects will be.

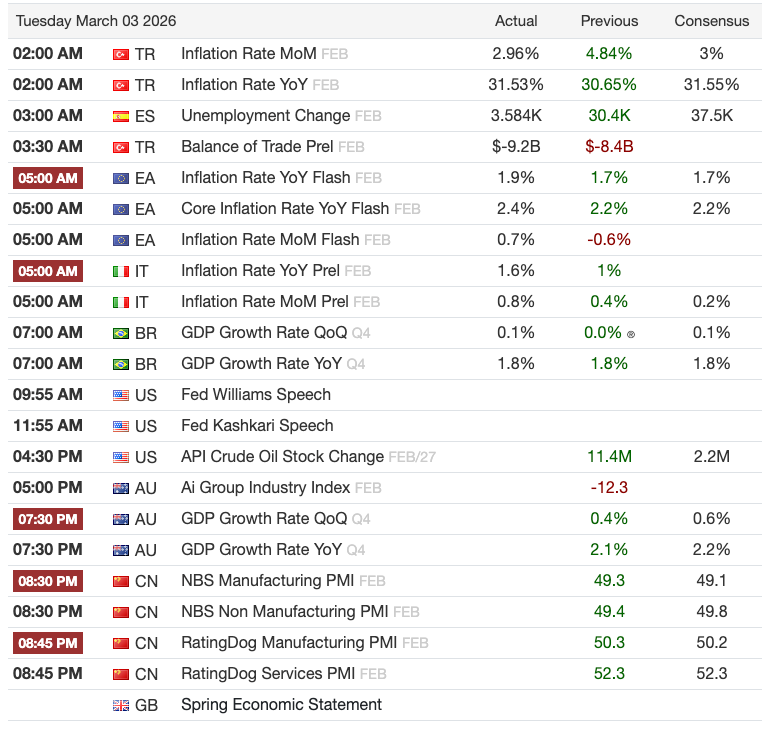

Calendars

Market Prep

Equity markets are climbing a wall of worry. But the wall is not just the war in the Middle East. We see several factors that contributed to the overnight sell-off, with the war making it much worse.

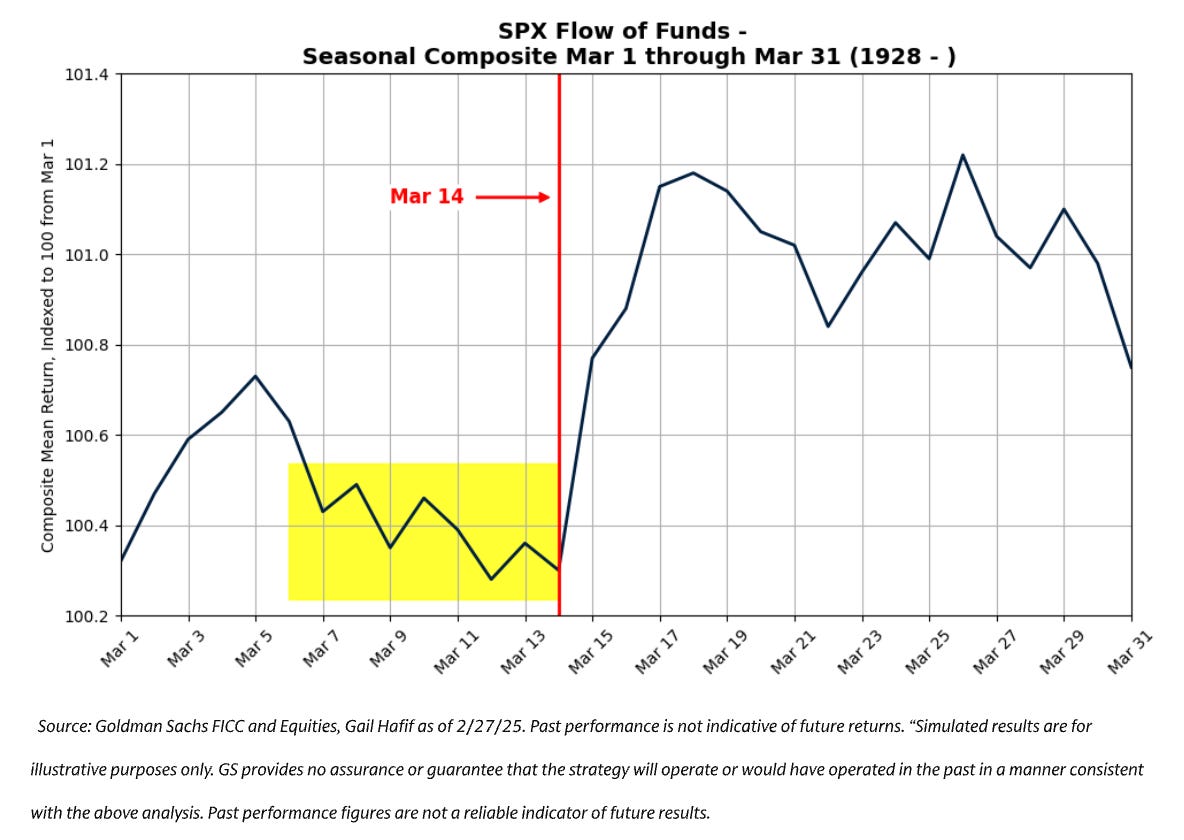

“Beware the Ides of March”, they say. Well, there’s some truth to that. We are in a seasonally weak period for stocks until 14 March. Historically speaking, March tends to be the 4th worst month for stocks. The second half of March shows some improvement, and then April sees a rally.

We continue to see de-risking in AI and some cyclicals, despite a relatively stable macro backdrop in the US. Yesterday’s ISM Manufacturing number was a relatively solid print at 52.4 vs 51.8 est. We’ll know more when the jobs numbers are released throughout the week and on Friday.

And then we also have the private credit weakness. Yesterday’s news of 1.7 billion in redemptions from BlackRock also hit that part of the market hard. “Redemption requests from the $82bn Blackstone private credit fund, known as Bcred, rose to 7.9 per cent of its assets in the first quarter, eclipsing a 5 per cent threshold that allows the private investment group to limit payouts to withdrawing investors.” - FT

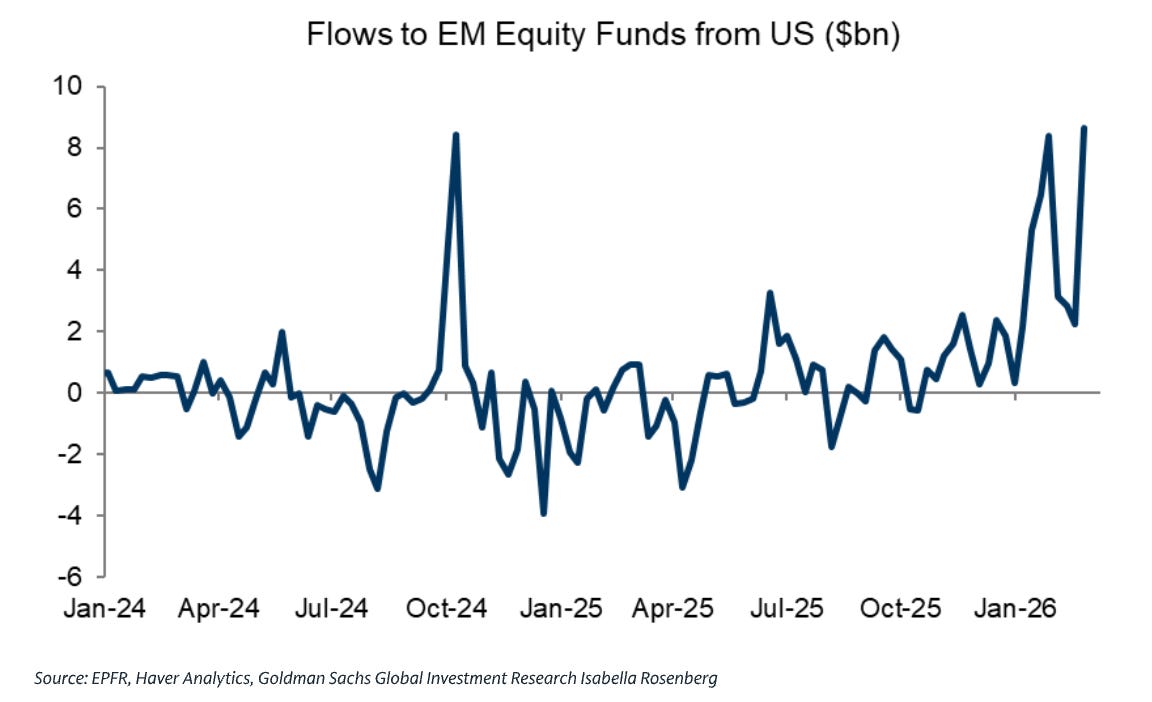

Rotation within sectors in US markets is one thing but we’re also seeing rotation to other countries. Internationally, global fund flows have rotated quite a bit to Emerging Markets, as we highlighted last week. Korea saw the highest inflows in the past few weeks but Chinese inflows have also turned positive, as investors chase the AI story there.

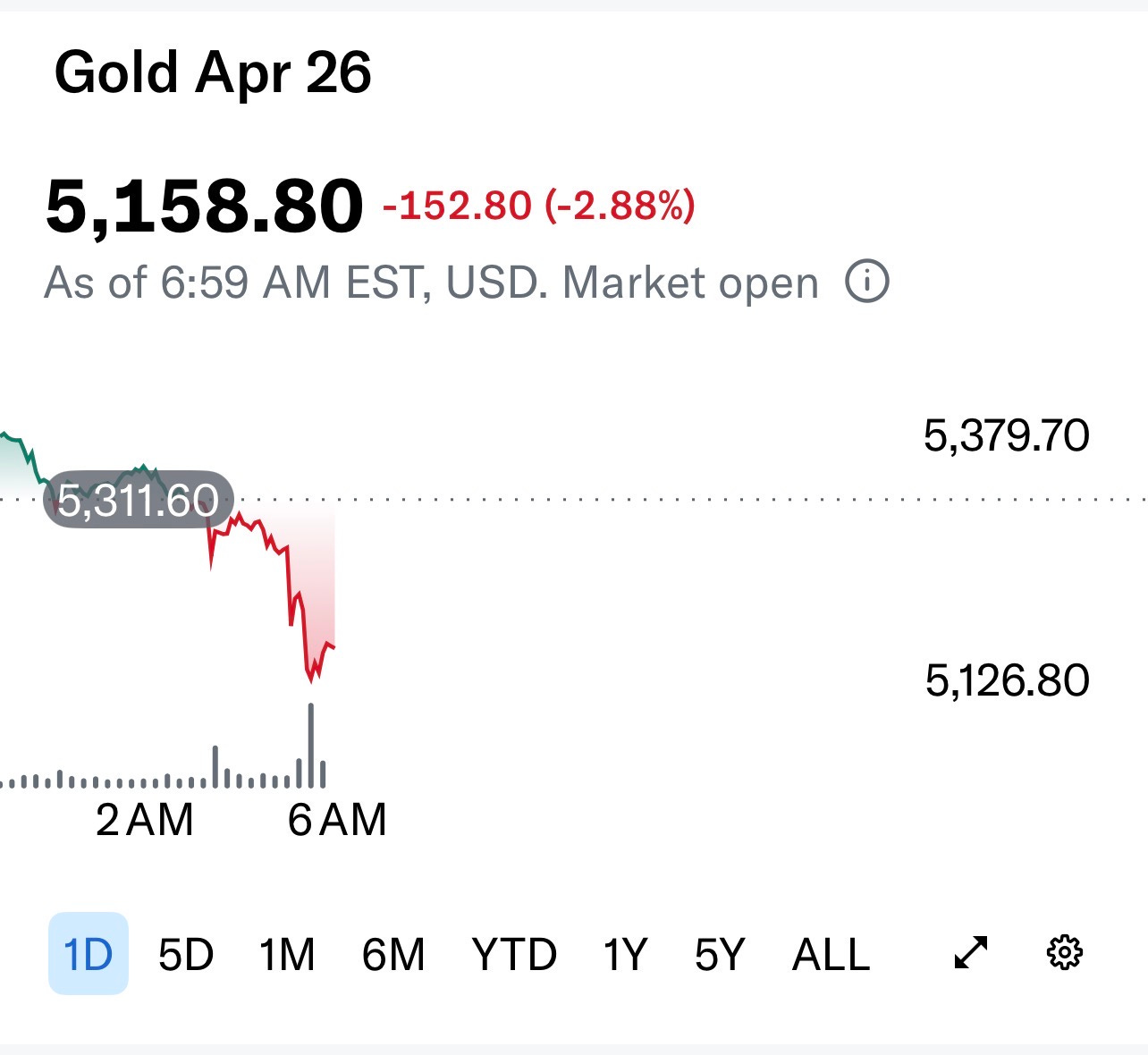

We have yields moving higher again. I think some of the sell-off in treasuries is also because most countries have been looking at Gold as a substitute safe haven asset. But what is interesting today is Gold selling off in the pre-market.

I think this is a rotation to the USD. Remember, the short positioning in the USD was already stretched, and now we have a catalyst. We talked about this yesterday - commodities, including oil, are priced in US Dollars, which is creating demand for the currency. All these months, many stockpiled Gold, quite likely for this day!

A higher dollar puts pressure on earnings, and that never helps market sentiment. So we have a number of factors that are causing the market to sell off. Nevertheless, this pressure continues to be touted as a buy-the-dip opportunity. I would agree with that, but with a caveat. I think scaling in is a better option, given the war right now.

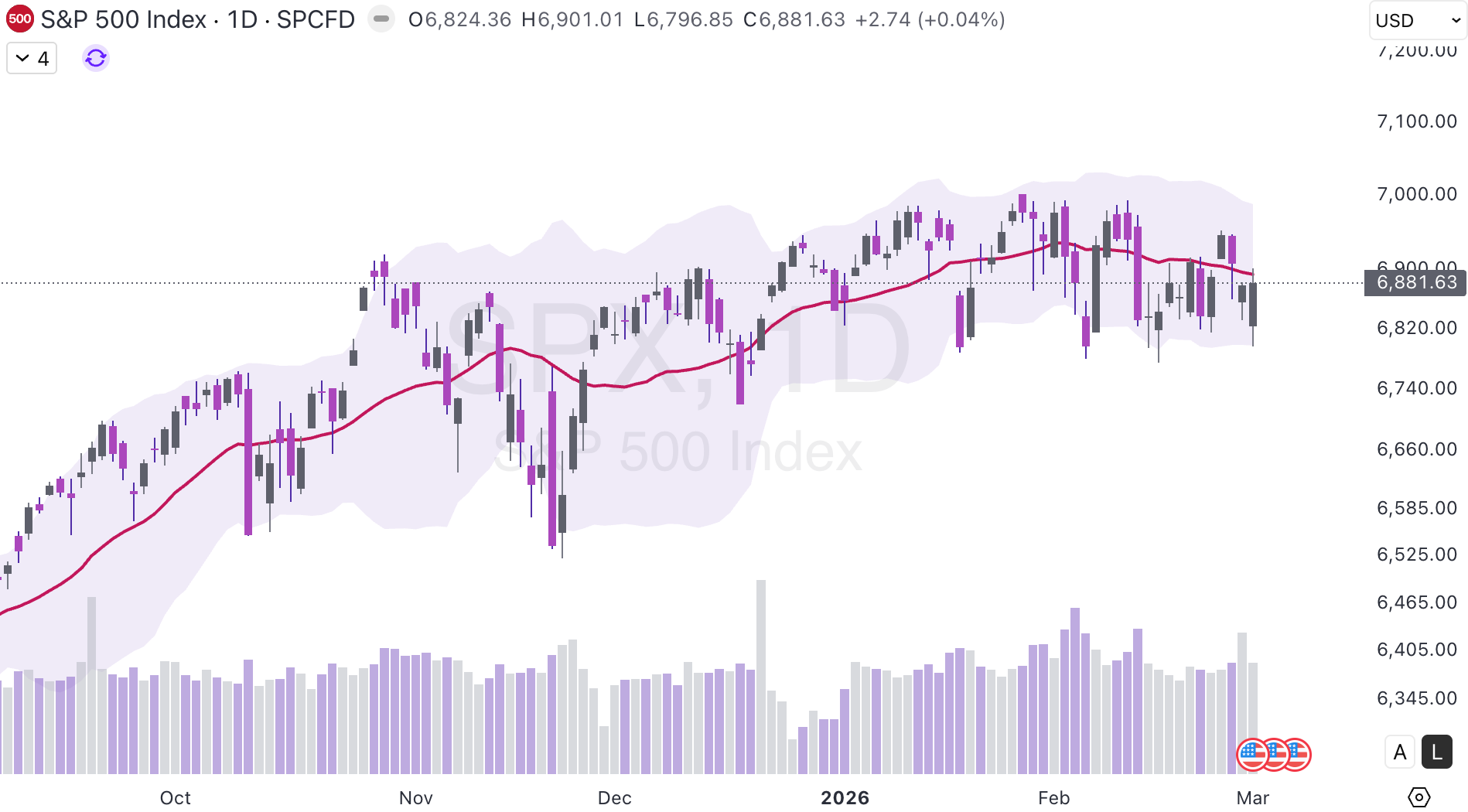

The S&P 500 has been relatively range-bound, and the likelihood of a break to the downside is currently higher before it can reclaim 7000.

My Take

US equity futures are under heavy pressure right now as the expanding overseas conflict makes stagflation a much more realistic threat. Rising energy and agricultural commodity prices are pushing Treasury yields higher and negatively impacting overall market sentiment. We are also fighting against historical seasonal weakness, a surging US Dollar, and notable private credit fund redemptions nearing 8%. Given all these complex global headwinds, slowly scaling into new positions seems to be the smartest way to navigate the current environment.