Breakfast Bites - Banks report but Tariffs still the headlines

Deal reached with Indonesia; Pharma tariffs threatened; Nvidia maybe allowed access to Chinese market

Rise and shine everyone

Earnings season started on a mixed note, with JP Morgan, Bank of America delivering beats, but Wells Fargo falling short.

Indonesia is the latest country to secure trade terms with the US, agreeing to a 19% duty on exports while allowing zero tariffs on US imports. This is a significant drop from the 32% imposed in April, and Indonesia hailed the deal as a major win for its labor-intensive sectors.

President Trump hinted that India is moving along similar lines and said 5 to 6 trade deals are currently in progress, with 2 to 3 likely to be finalized by August 1. For smaller countries, he suggested a blanket tariff of just over 10%.

On pharmaceuticals, Trump confirmed that initial US tariffs will be kept low but will rise significantly in about 18 months, particularly for non-US made drugs. The same phased approach will apply to semiconductors, though with fewer complications. European pharma stocks came under pressure on the back of this announcement.

Nvidia CEO Jensen Huang noted that the company has not yet received export licenses for its H20 chips but remains confident they will be granted quickly, given the volume of orders already in place.

Asian equities were mixed. Hang Seng initially outperformed, hitting a three-year high, but ended flat. Kospi and ASX lagged behind. In Japan, yields on the 40-year bond fell 5bps as the yen weakened past 149 to the dollar.

Iron ore prices topped $100 per ton, with analysts attributing the strength to improving sentiment around China. Rio Tinto also flagged strong Chinese demand for raw materials, helping to offset tariff-related pressures elsewhere.

Tensions between Japan and China may rise after a Chinese court found an Astellas employee guilty of spying. The employee has been detained since March 2023.

In the US, Trump assured that the House would pass the GENIUS crypto bill tomorrow, after today’s failure. Some lawmakers were unhappy that the bill lacked provisions banning a Central Bank Digital Currency, which Trump had previously pushed through an executive order.

European markets appeared flat overall, but under the surface, there was a sharp sector divergence. Autos fell after Renault cut its full-year guidance following a weak June. Tech stocks also dragged, with ASML narrowing its full-year outlook and warning about FY26 due to geopolitical uncertainty.

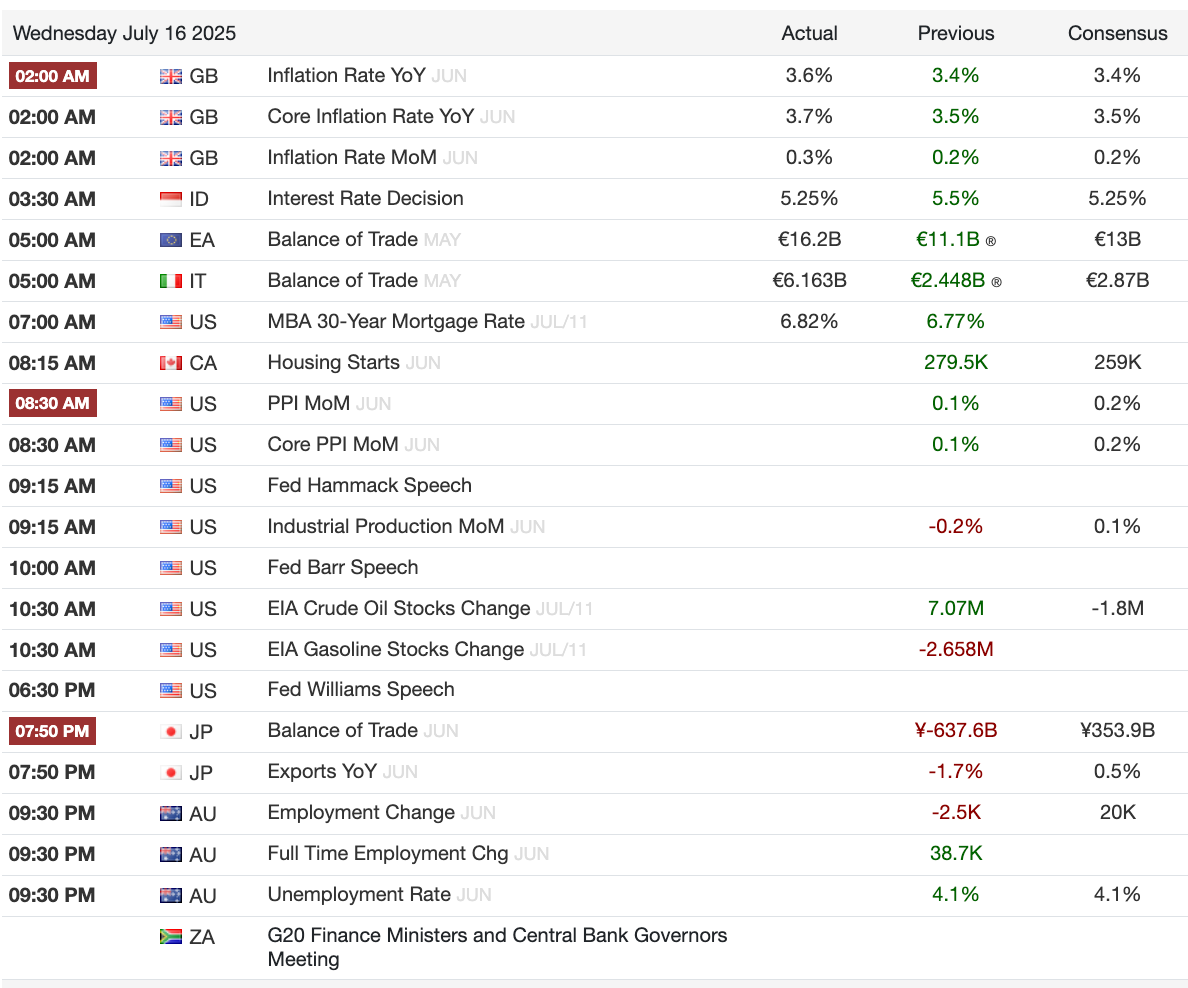

UK inflation surprised to the upside. Headline CPI rose to its highest level since January 2024, and core inflation hit 3.7%, above estimates.

The initial bounce in the pound reversed quickly, as weak growth, fiscal worries, and a murky trade outlook remain dominant. Market pricing for a BOE rate cut has been pushed back slightly.

J.B. Hunt’s earnings reflected the difficult macro backdrop. The company cited policy uncertainty and regulatory friction while managing early peak-season surcharges and a tighter truckload market. It leaned on premium services and pre-funded capacity to weather the volatility.

We still have more banks and large caps reporting today, before and after the close. Plus, we have the PPI out at 8:30 am ET.

Bloomberg Appearance This Morning

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)