Breakfast Bites - Banks kick off earnings

CPI on deck; Trade tension with Russia; China GDP growth at 5.2%

Rise and shine everyone

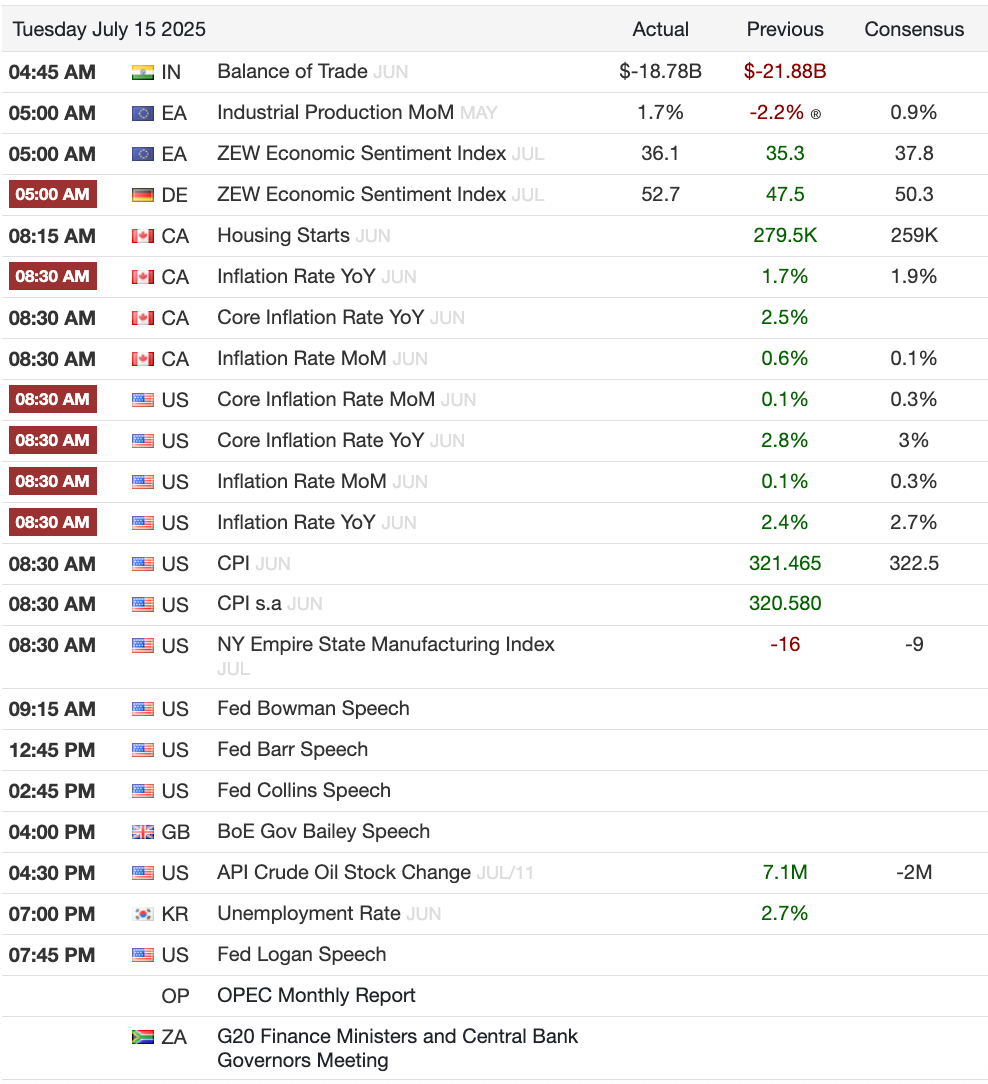

Today’s focus will be US CPI data released at 8:30 am ET, but we also get bank earnings today.

First, let’s look at the CPI data. Last month’s CPI data surprised to the downside, and as we predicted, was mostly driven by lower energy prices. We did see a spike in oil prices last month because of the conflict, but how much of that feeds into the CPI for the month of June remains to be seen. Food and Shelter didn’t move much, so I suspect some of the focus will be on that.

It’s also quite likely that we will see early signs of some of the tariff price increases. I say this because we’re seeing customs revenue data increase for the month of June, so some of that could be reflected in the CPI numbers, but if not, then the PPI.

The major banks kick off earnings season today. Wells Fargo CEO Charlie Scharf highlighted solid Q2 results, with higher earnings and revenue driven by stronger fee-based income and consistent credit performance. He called the lifting of the asset cap a major milestone, enabling the bank to expand more aggressively. Additionally, Wells Fargo repurchased over $6B in stock in H1 and plans to raise its Q3 dividend by 12.5%, pending board approval.

China’s June data came in mixed. Q2 GDP beat expectations and stayed comfortably above the government’s 5% target for the year, but the details tell a familiar story. Retail Sales were weaker than expected despite the government’s push through stimulus and trade-in programs. In contrast, Industrial Production posted a strong beat, reinforcing the idea that China continues to produce more than it consumes — essentially exporting its domestic oversupply. Official commentary after the release leaned heavily on the need to boost domestic consumption, but we’ve heard that before.

Meanwhile, the property market remains under pressure. June new home prices fell at the fastest pace in eight months. The broader China property index dropped 3.7%, and China Vanke was down 4%, as sentiment continues to deteriorate in the sector.

Some US-based analysts are now rethinking near-term PBOC easing, especially after the stronger M2 growth in June. That data may give the central bank reason to pause before pulling the trigger on another rate cut.

In broader Asia, equities had another quiet session with no major standout performers. Markets are largely in wait-and-see mode ahead of the US CPI release tonight, which could provide clearer direction.

As for Japan, rate hike expectations are swinging again. Market-based pricing for a 25bps hike in October has risen to 41.5% from 33% on Friday, while December odds jumped to 65.5%. Still, the yen failed to benefit and dropped by a full figure against the dollar, now trading near four-week lows.

Japanese bond yields continued their upward climb. The 10-year JGB rose to its highest level since October 2008 — a level that was last tested in May. Long-end yields also moved higher, with the 20-year reaching levels not seen since 1999.

Trade tensions remain front and center. Trump has now threatened 100% secondary tariffs on Russia if a Ukraine peace deal isn’t reached within 50 days, following earlier threats against the EU and Mexico. Meanwhile, markets got a boost from Nvidia’s decision to resume H20 chip exports to China.

Separately, FT reports Trump privately urged Zelenskiy to strike inside Russia — even Moscow — if given longer-range weapons, framing it as a way to force peace talks. While a list of systems was shared with NATO partners, it’s still unclear if the U.S. will follow through.

Chart of the Day

This is a slide from Fastenal’s earnings presentation yesterday. I really liked this slide because it goes to show that companies are preparing for how tariffs can affect them.

Fox Appearance

We discussed earnings, stock picks, and the markets.

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)