Breakfast Bites: Amazon results lift US tech index

ECB keeps rates on hold; Big Energy Reports today; Gold still has hope; My Bloomberg appearance

Rise and shine everyone

The major events of the week are behind us, and I’m looking forward to a quieter Friday, heading into the weekend.

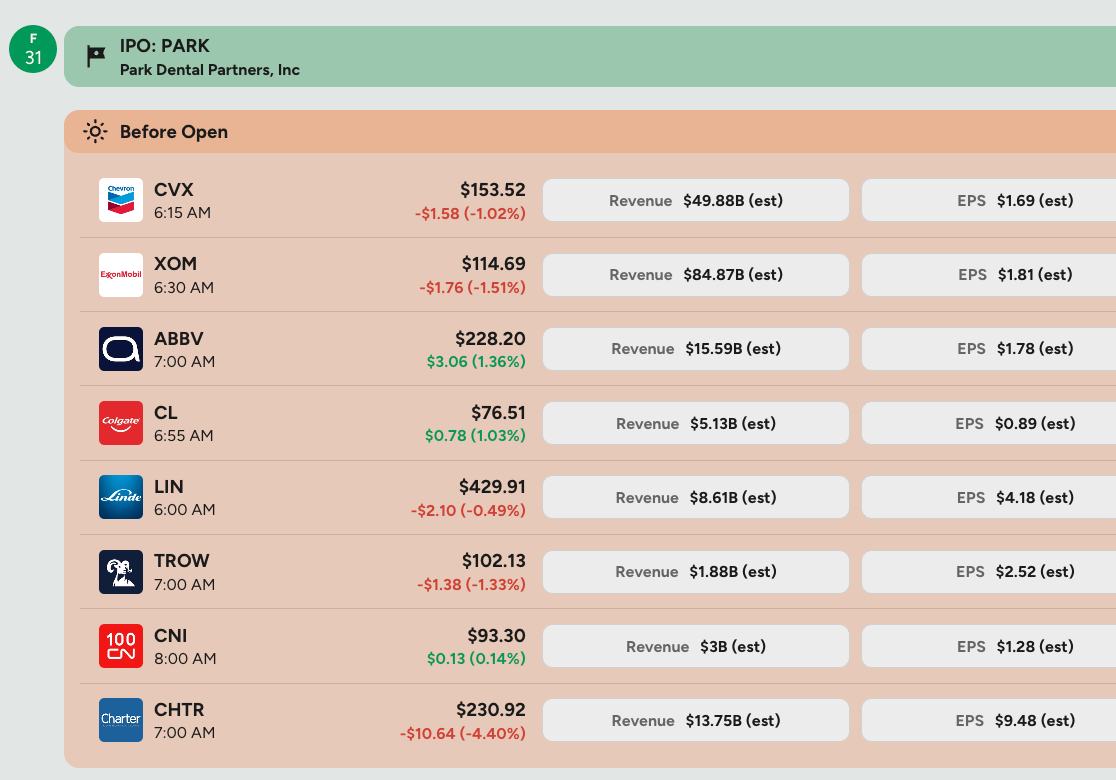

We still have the two energy majors reporting today before the open, alongside AbbVie and Linde. We also have the EA inflation numbers coming out.

Speak of the EA, the ECB kept rates unchanged and maintained its wait-and-see stance, signaling that policy is already in a “good place” and the economy is broadly developing as expected. The bar for another cut remains high, with the ECB emphasizing data dependence and fewer downside risks compared to earlier in the year. We will get updated forecasts in December, including 2028 inflation numbers and that’s when we may get some clarity on whether is easing has truly ended.

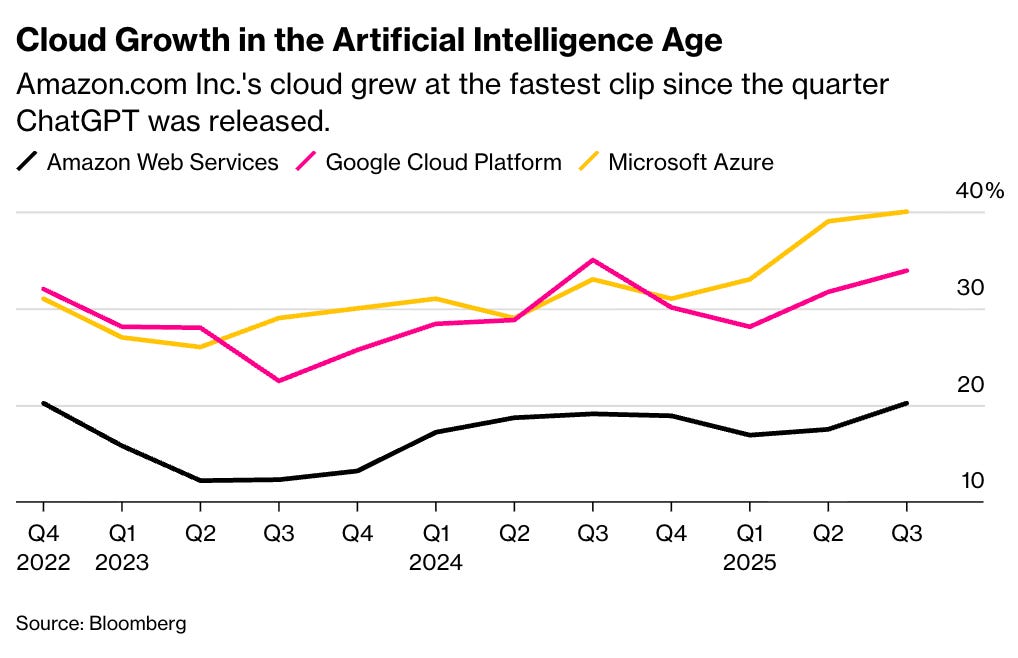

US Equity Futures are higher this morning, particularly the Nasdaq with most of big tech pulling it up. Amazon is up just over 12% after reporting strong AI-driven cloud growth during their earnings yesterday.

Amazon’s quarter was all about the re-acceleration in AWS. Cloud revenue grew 20% year on year, the fastest pace since 2022, with management pointing to AI workloads as the key driver behind the pickup. The company has been aggressively expanding data center capacity and leaning into its custom silicon strategy, which pushed capex meaningfully higher. The message from Andy Jassy was that AWS has momentum again, supported by early traction in Bedrock and the broader AI services stack.

For the holiday quarter, Amazon guided revenue to $206–213 billion and operating income to $21–26 billion. The tone was cautiously optimistic, even with the recent outage and headlines around job cuts. Retail and advertising continue to contribute, but the investment case today rests squarely on the cloud and AI infrastructure build-out. Amazon is spending to stay in front of the curve, and investors are beginning to reward the shift back to growth at AWS.

It’s a bit of a slow news day otherwise, and we can be grateful for that!

Chart of the Day - DB notes gold ETF outflows accelerating, but correction nearing exhaustion

We still like Gold, and it was one of my picks on Bloomberg yesterday. It looks like Deutsche Bank has some research to support my thesis.

Gold ETFs have seen a sharp pickup in outflows over the past few days, reaching more than half of the selling seen during the April–May drawdown in just four sessions.

The price reaction has been unusually sensitive relative to the amount of ETF selling, suggesting investors may now be expressing gold views through other instruments beyond traditional ETFs.

Based on prior drawdown patterns, the current correction could bottom around USD 3,700–3,800/oz if an additional 300–600 thousand ounces are sold.

Medium-term fundamentals remain supportive, with expectations for gold to eventually move back toward USD 4,000/oz once this correction stabilizes.

Central bank purchases will be in focus with upcoming Q3 data; a result near the estimated ~240 tonnes of buying would reinforce continued official-sector demand, while a weaker figure may raise concerns about reserve manager appetite.

Appearance on Bloomberg

I was on Bloomberg Horizons yesterday. My spot starts at the 15 min mark on the video below.

We covered:

The possibility of a Fed cut in December

The data void because of the shutdown

The Fed decision on bond and equity markets

US-China - there’s still a lot to work out

Our picks: Small Caps; China Tech Equities.

We also continue to like gold and remain bearish on the USD

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)