Breakfast Bites: +12% day

Markets soar on Trump's tariff pause; China gets hit with more; Gold and USD maintain trajectory; US Inflation report at 8:30 am ET

Rise and shine everyone.

What a day we had yesterday! Going from a gloomy market environment to a 12% jump in the Nasdaq. All broad market indices were up after President Trump posted about “buying” and later followed that up with an announcement to pause reciprocal tariffs for 90 days for countries that had reached out for negotiations.

Global markets also shared the enthusiasm this morning. The Nikkei jumped 8%, marking its best performance since August 6th, 2024. Australia’s ASX and South Korea’s Kospi also saw strong gains of around 5%.

Toyota rose 11%, while Japan’s major banks surged between 12% and 16%, recovering from recent sharp declines.

In Europe, Eurostoxx and DAX futures climbed 9%. South Korea’s SK Hynix gained 13%, and Taiwan’s TSMC hit its daily limit with a 10% increase. Foxconn was up 9.8%, helping lift Taiwan’s Taiex index to a record 9.2% gain. Interestingly enough, Chinese markets were also up this morning.

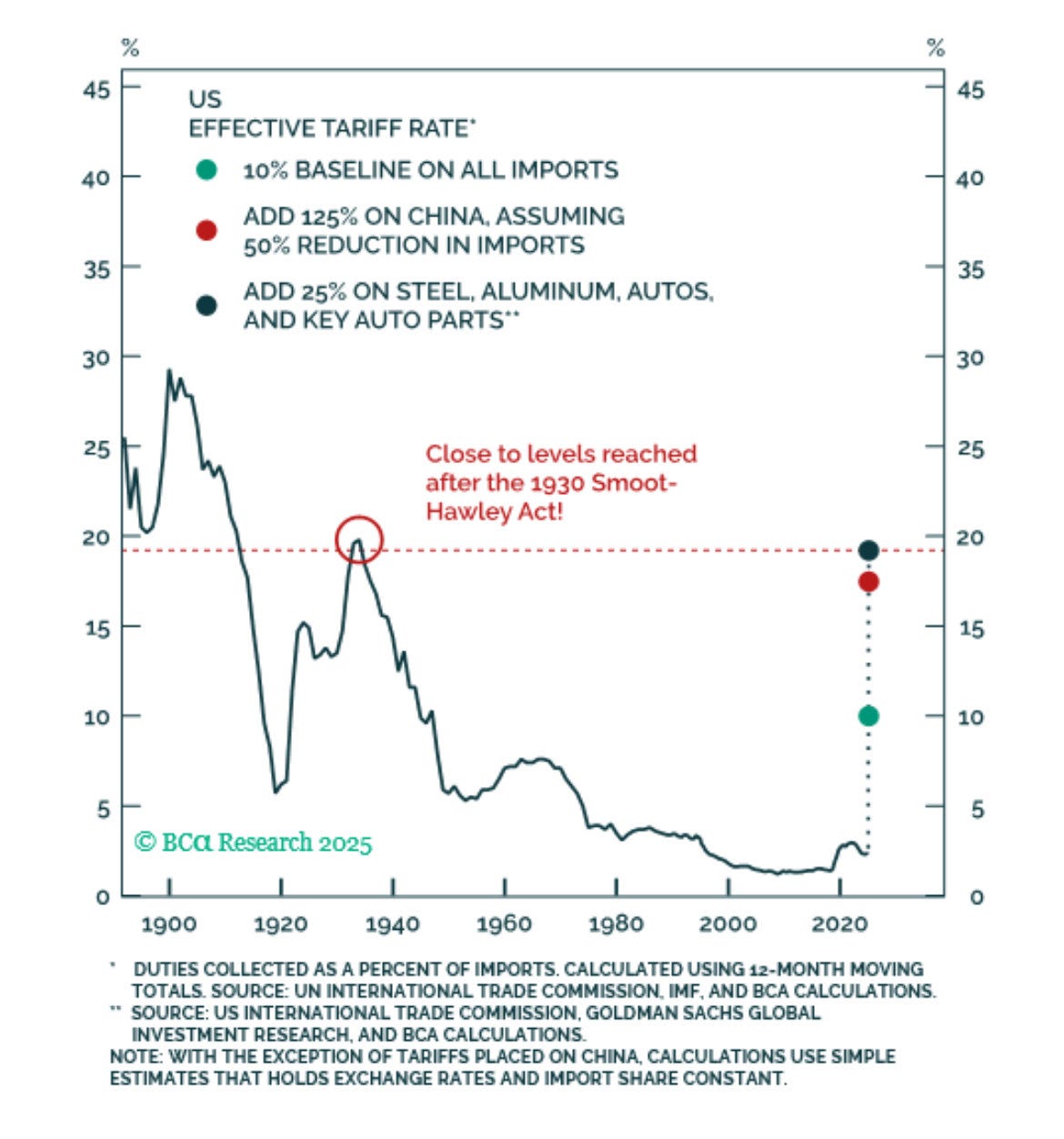

A couple of nuances to point out though. Tariffs on China were increased to 125%, and the pause came with a lower level of tariffs of 10% for the rest of the countries, while the negotiations are worked out over the next three months. Europe has just announced a pause on their retaliation, which is a positive move.

According to BCA, this still means a higher overall tariff level for the US, so the economy is still not out of the woods, so to speak. This escalating trade war with China could continue to bring on unprecedented levels of inflation and lower trade. Phasing out from China is a process and won’t happen overnight.

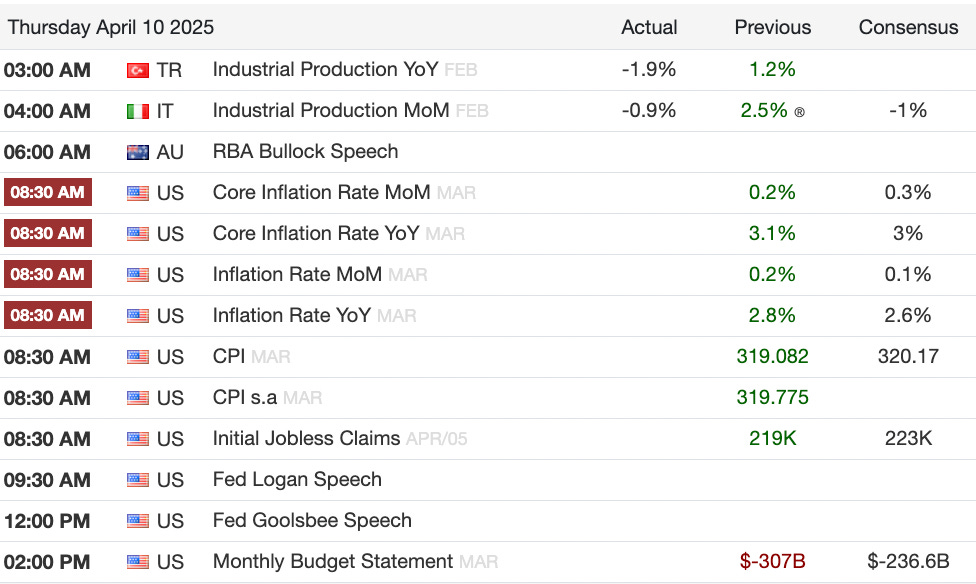

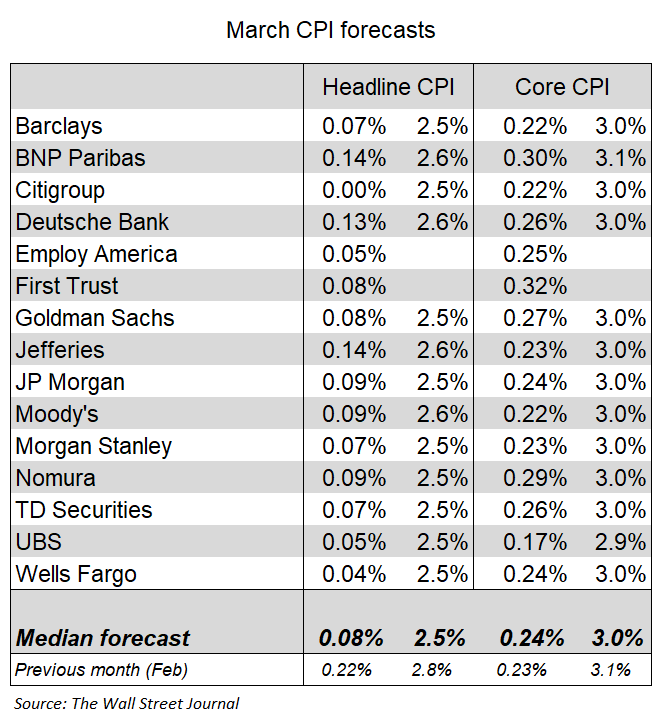

Our attention now turns back to the macro. The focus today will be US CPI, to be released at 8:30am ET. The estimates are in and they seem to be trending lower for Headline CPI.

There’s no doubt that inflation still remains a crucial factor for the Fed. Yesterday, we got the Fed minutes, which showed a cautious approach and focus on inflation in the coming months. This reading may come in lower from previous months, but tariffs just went live and the impact will certainly be felt in the next two quarters.

They also discussed reviewing the Fed’s policy framework, specifically the language around employment goals, suggesting it may be time to rethink how they address shortfalls in job levels.

While yesterday’s tariff pause was telegraphed as having nothing to do with the markets, we can’t help but wonder whether the surge in UST yields had anything to do with the decision. President Trump made a remark about it as well. Whatever the reason, it seems to have worked. Bond yields are pulling back again.

Gold, however, never paused its rally. It would seem that investors are still seeing fear in the markets and hiding out there. The USD is lower this morning, suggesting the faith in trade is yet to return, and US Equity Futures are selling off some of their gains.

Yesterday was a truly remarkable day, and we will probably remember it for years to come, but it also means that we’re still looking at highly volatile markets that are event-driven.

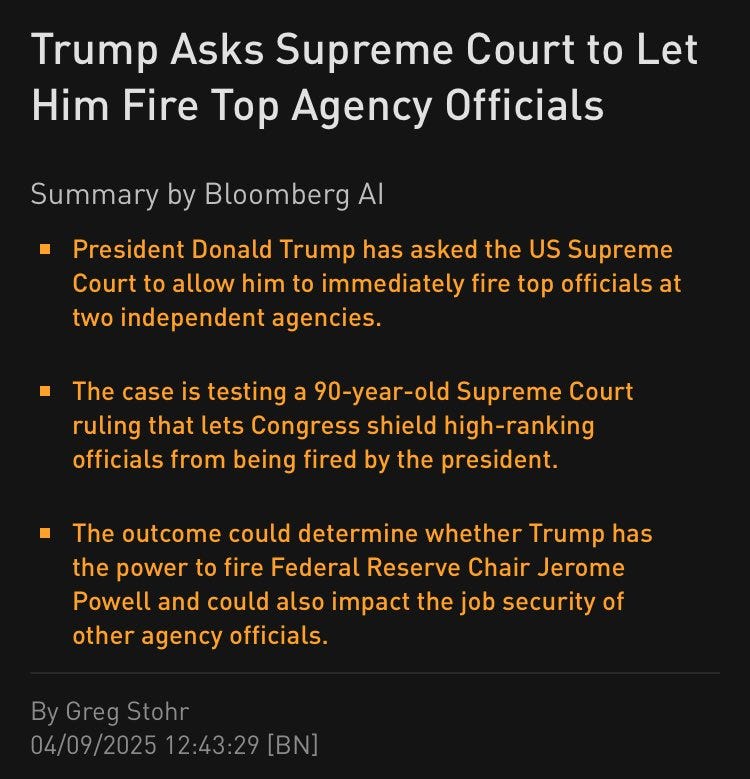

Here’s some interesting drama this morning that I just came across. President Trump is asking the Supreme Court to let him fire top agency officials. According to Bloomberg, this could determine whether he has the power to fire Fed Chair Powell.

Chart of the Day

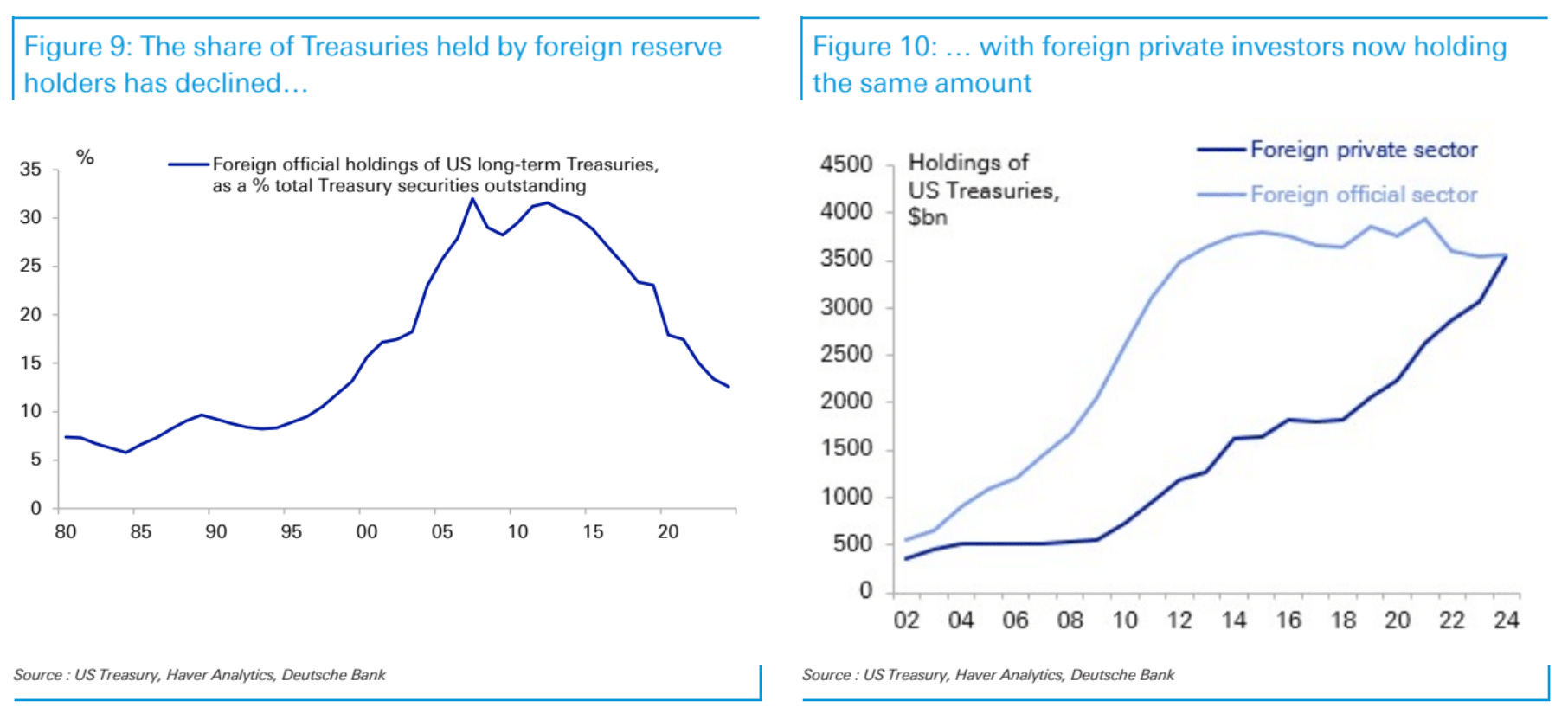

This is a great set of charts from DB. Yesterday, we talked about China, and overseas investors possibly dumping US treasuries, leading to some of the decline in price. These charts suggest that the dumping had actually started a while back but what’s also interesting is that while official sectors have been lowering their positions, foreign private sectors have been filling the void.

What We’re Watching

8:30 am ET - US CPI

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)