Every AI query you’ve ever typed used about a shot glass of water.

Multiply that by 2.5 billion daily prompts. Add the training runs that consume tens of millions of liters per model. Add the 211 billion gallons of water that US power plants burn through every year just to generate the electricity that runs the chips. Then put the whole thing on an 11x growth curve through 2028.

That is where AI infrastructure is heading. This explains why a 7-0 vote in Tucson, Arizona, last August killed a $2.5 billion Amazon-backed data center, why Google halted a $200 million project in Chile, and why 73% of data center operators surveyed by Schneider Electric in 2025 said water availability is now slowing down their projects.

For the better part of three years, the AI infrastructure conversation has revolved around two scarce resources, chips and electricity. But the third resource, water, is now starting to show up in earnings calls, permitting decisions, and sell-side research notes in a way it simply did not 2 years ago.

Morgan Stanley’s base case has AI data center water consumption rising more than 11x by 2028, from 95 billion liters to roughly 1,068 billion liters. Google’s water withdrawal jumped 28% in a single year. Microsoft’s usage surged 87% from 2020 to 2023. Bloomberg and World Resources Institute data show that two-thirds of data centers built since 2022 are sitting in water-stressed regions.

Water is becoming a binding operational constraint on where data centers can be built, how they have to be designed, and which suppliers will capture the next leg of the capex supercycle. And that, for investors, is exactly what makes it tradable.

In this piece, I’ll walk through:

Why AI is structurally so much more water-hungry than traditional cloud computing

The disclosed numbers from Google, Microsoft, Meta, and the gaping hole where Amazon’s data should be

Why water stress is a localized risk that is already killing projects

The regulatory ratchet that is tightening globally, even as US federal policy loosens

The liquid cooling total addressable market, which is expected to increase from a few billion dollars today to $15 to $30 billion by 2030

And five stocks that give you exposure, including the underappreciated water tech name that just made a $4.75 billion acquisition, the market hasn’t fully digested

Let’s start with the physics.

Why AI is so water-intensive

Data centers convert electricity into computation and waste heat. Cooling that heat consumes 20% to 40% of total facility energy, and water has historically been the dominant cooling medium because its heat absorption capacity is roughly 3,000x greater than air’s.

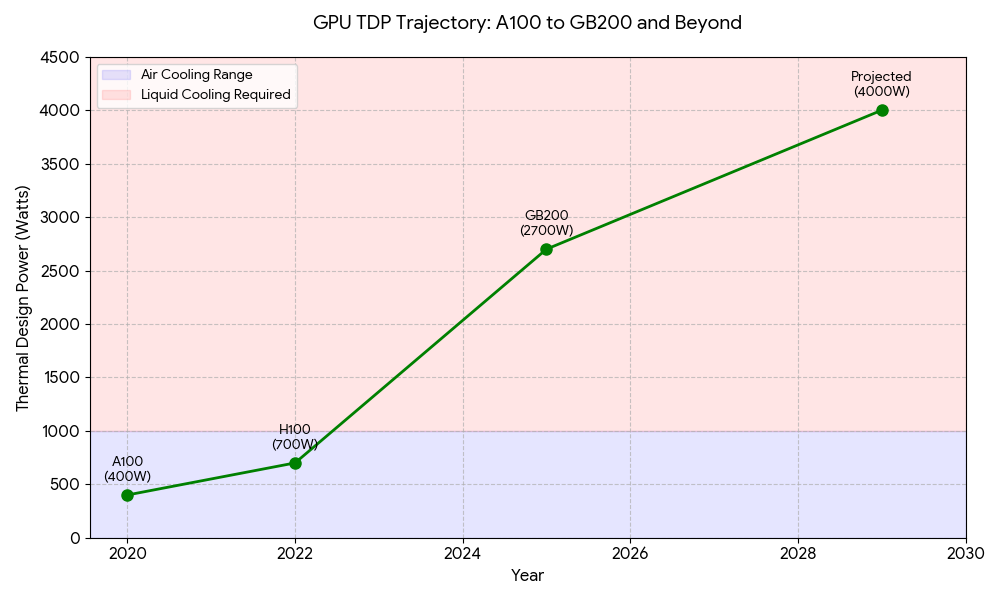

AI has pushed this to the max now. Traditional server racks operate at 5 to 15 kW. NVIDIA H100-based AI racks run at 40 to 50 kW. The current GB200 NVL72 system draws 120 to 140 kW per rack, a jump that makes conventional air cooling physically inadequate. Dell’Oro projects leading-edge GPU thermal design power will exceed 4,000W by 2029. Every watt becomes waste heat that needs to leave the building.

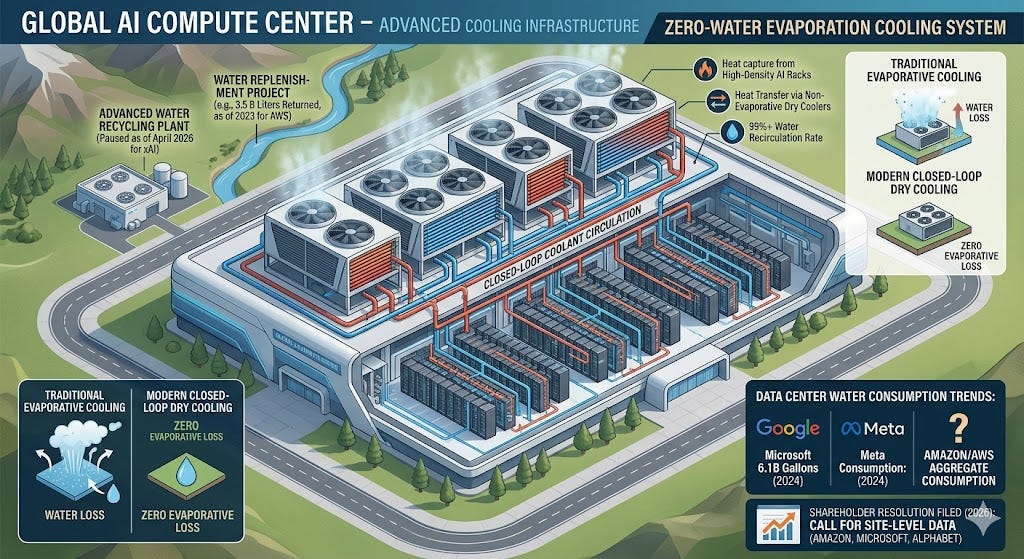

Three water-using cooling methods dominate the installed base. Evaporative cooling towers, the most common, lose roughly 80% of withdrawn water to evaporation. A 1 MW data center can pump around 855 gallons per minute through one. Chilled water systems and air-assisted evaporative units sit in between. The newer alternative, closed-loop direct liquid cooling, recirculates coolant in sealed pipes and consumes only 5% to 10% of the water of evaporative systems. NVIDIA claims its GB200 NVL72 delivers 300x better water efficiency than equivalent air-cooled H100 infrastructure.

Two metrics define the efficiency conversation. Power Usage Effectiveness (PUE) measures total facility power divided by IT power, with the industry stuck around 1.56 since 2020 and best-in-class hyperscalers at 1.09 to 1.15. Water Usage Effectiveness (WUE) measures liters consumed per kWh of IT energy, ranging from near zero for dry-cooled facilities to 9 L/kWh for inefficient evaporative ones. Crucially, the two metrics are in tension: using more water lowers PUE but raises WUE. That structural tradeoff is why site-by-site decisions, and the technologies that resolve it, matter so much.

The disclosure cycle is finally exposing absolute volumes

The disclosed numbers tell a consistent story of structural acceleration.

Google provides the most granular disclosure. In 2024, Google consumed approximately 6.1 billion gallons (22.7 billion liters) of water, with data centers accounting for roughly 95% of the total. Its largest single facility, Council Bluffs, Iowa, consumed 1 billion gallons in 2024 and peaked at 2.7 million gallons per day during the summer. Google’s water consumption roughly tripled from 2016 to 2024. The company provides site-level data for owned and leased facilities but excludes third-party operations.

Microsoft reported FY2023 total water withdrawal of 7.8 million cubic meters (about 2.06 billion gallons) with net consumption of 6.4 million cubic meters (about 1.69 billion gallons). The headline figure: FY2022 consumption surged 34% year over year, widely attributed to GPT training workloads at Iowa data centers. Microsoft’s WUE improved from 0.49 L/kWh in 2021 to 0.30 L/kWh in 2024, a 39% improvement. As of August 2024, all new Microsoft data center designs use “zero-water evaporation” cooling. The company does not provide site-level breakdowns.

Meta disclosed 2024 consumption of 5,637 megaliters (1.489 billion gallons), a 51% increase from 3,726 megaliters in 2020. Meta reports for owned sites only and excludes leased facilities, a significant gap given its rapid expansion.

Amazon and AWS, the world’s largest cloud provider, do not report total aggregate water consumption. This is the most consequential disclosure gap in the sector. AWS reports only intensity metrics (usage per unit of power) and partial replenishment figures (3.5 billion liters returned in 2023). Twelve-plus shareholders filed resolutions ahead of the 2026 annual meetings demanding site-specific water and power data from Amazon, Microsoft, and Alphabet.

xAI’s Colossus 1 facility in Memphis currently draws 1.3 million gallons per day from the Memphis Sand Aquifer, with peak demand projected at 5 million gallons per day. An $80 million planned water recycling plant was indefinitely paused as of April 2026. Oracle and CoreWeave provide no meaningful water consumption disclosure, though both claim new facilities use closed-loop, non-evaporative cooling.

The trend table makes the trajectory clear:

Company 2020 2023 2024 2020 to latest Google ~14.2M m³ 24M m³ ~22.7M m³ +60 to 69% Microsoft ~4.2M m³ ~7.8M m³ Not yet reported +87% Meta 3,726 ML ~3,100 ML 5,637 ML +51% Amazon Not disclosed Not disclosed Not disclosed N/A

Combined Big Tech water consumption (Google, Microsoft, Meta, and Apple) grew 61% from roughly 25 million cubic meters in 2020 to roughly 41 million cubic meters in 2023 (Surfshark Research, April 2025). Total US data center direct water consumption reached 17 billion gallons in 2023, with an additional 211 billion gallons consumed indirectly through electricity generation.

The growth rates are no longer something investors can dismiss as ESG noise. They reflect real operational constraints showing up in real cost lines.

Water stress is highly localized, and regulations are ambiguous

Morgan Stanley finds that more than half of the world’s top 30 data center markets by operational IT load already face medium basin physical risk. The same is true of the secondary markets where new builds are concentrated.

A Schneider Electric, AlphaStruxure, and Data Center Frontier survey in 2025 captured the operator perspective: 73% of respondents said water availability is now slowing the development of data centers.

The regulatory direction outside the US is unambiguously restrictive. The EU Energy Efficiency Directive (2023/1791), since October 2023, requires all data centers above 500 kW IT power to report PUE, WUE, and other metrics annually. The European Commission may propose minimum performance standards by the end of 2026. Singapore’s DC-CFA2 round, launched in December 2025, requires Green Mark Platinum certification, a PUE of 1.25 at full IT load, and 50% green power. The Netherlands has banned new hyperscale data centers outside two designated areas. Ireland lifted its moratorium in December 2025 only after attaching strict renewable power conditions. China incorporates WUE into its national green data center rating system.

Within the US, state and local governments are picking up the slack. Loudoun County, Virginia, eliminated by-right data center development in March 2025. Reno, Nevada, is considering a moratorium. Minnesota has passed a House bill requiring closed-loop cooling for new data centers. California’s SB 58 proposes tax credits for water-efficient cooling. More than 300 data center bills were introduced across US Congress and state legislatures during the 2025 session.

The net effect for investors is straightforward: water-efficient cooling is moving from an optional sustainability story to a permitting prerequisite. And that is where the investment case gets interesting.

Up Next….

The liquid cooling total addressable market, with five competing forecasts triangulated to a defensible $15 to $30 billion estimate by 2030

How the cooling thesis fits into the AI infrastructure capex supercycle, including the operational leverage math

My five stock picks across the value chain: the consensus growth name, the value alternative, the diversified industrial, the cross-over water tech play, and the lower-volatility second-derivative pick

What could derail the thesis?