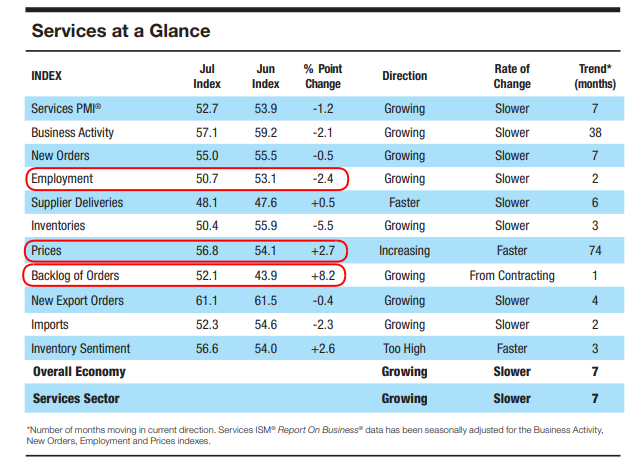

Today we received US ISM Services PMI data, which showed an appreciable slowdown in employment with rising prices and backlogs. Top-line growth also slowed month-over-month to 52.7 from 53.9.

The services industry remains in expansion, but that expansion is showing initial signs of slowing again. What’s happening with prices and backlogs rising as employment growth slows to almost neutral is a concern should it become a trend.

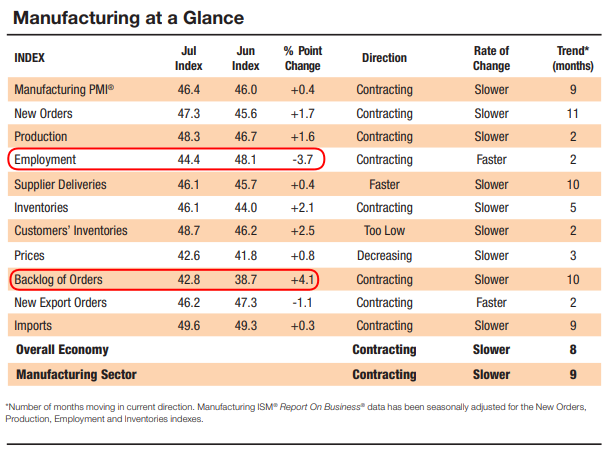

There are some similarities to manufacturing, which has been in contraction for almost a year. Backlog trends are improving as employment deteriorates. While the backlog of orders is still in contraction, that contraction has slowed while the pace of job reduction has increased.

Prices are still in a contraction, and that contraction slowed modestly in July.

We continue to believe that the services industry is a key area to watch for signs of slowing. The data today suggests that slowing process may be in its early stages, but we do need to see multiple sequential data points to confirm that assessment.

We would expect that if a more meaningful slowdown into contraction manifests, that prices would drop along with other business activities (like new orders, production, deliveries, etc). If such a contraction were to last multiple months and be met with jobless claim prints of 300K+ and unemployment rising meaningfully over 4% we would expect that it could lead to an economic slowdown and further earnings deterioration.

For now, however, the services industry is only slowing rather than contracting, and prices are rising at a time when employment growth is closer to neutral. We are concerned that multiple July data points suggest that we may see CPI for the month come in appreciably higher than June’s year-over-year data.

We’ll discuss that more later.